Weaker New Orders and China Slowdown Might Change The Case For Investing In ASM International (ENXTAM:ASM)

- In October 2025, ASM International reported strong third-quarter earnings with sales of €800 million and net income of €384.2 million, but new orders fell below market expectations due to a significant drop in Chinese demand and ongoing export restrictions.

- Despite solid performance in advanced logic and foundry segments and reaffirmed long-term growth targets, ASM International issued cautious guidance for 2025, highlighting lingering uncertainty in semiconductor demand and regional market risks.

- We'll examine how weaker-than-expected bookings, especially from China, may reshape ASM International's investment narrative and growth assumptions.

Find companies with promising cash flow potential yet trading below their fair value.

ASM International Investment Narrative Recap

For an investor to remain confident in ASM International, they need to believe that advanced node-driven demand, especially from AI and high-performance computing, will continue to offset cyclicality and geographic risks. The latest earnings results highlight robust ongoing performance, but the marked shortfall in China-related bookings underscores that the biggest short-term catalyst, AI demand in leading-edge nodes, remains at risk if weakness spreads further, particularly given the scale of recent order declines. For now, these impacts appear to be material enough to warrant close tracking rather than being dismissed as temporary noise.

The most relevant recent announcement is the company’s updated Q4 2025 revenue guidance of €630 million to €660 million, reflecting management’s view that order softness, mainly from China, could persist into the next quarter. This cautious outlook reinforces that while the underlying growth story is intact, visibility on the timing of a demand rebound is limited, keeping the spotlight on quarterly order trends and regional exposure. Despite double-digit revenue and robust profitability, investors should also be alert to some unresolved uncertainties, especially as order intake from China slows and ASM’s customer concentration risk remains in focus...

Read the full narrative on ASM International (it's free!)

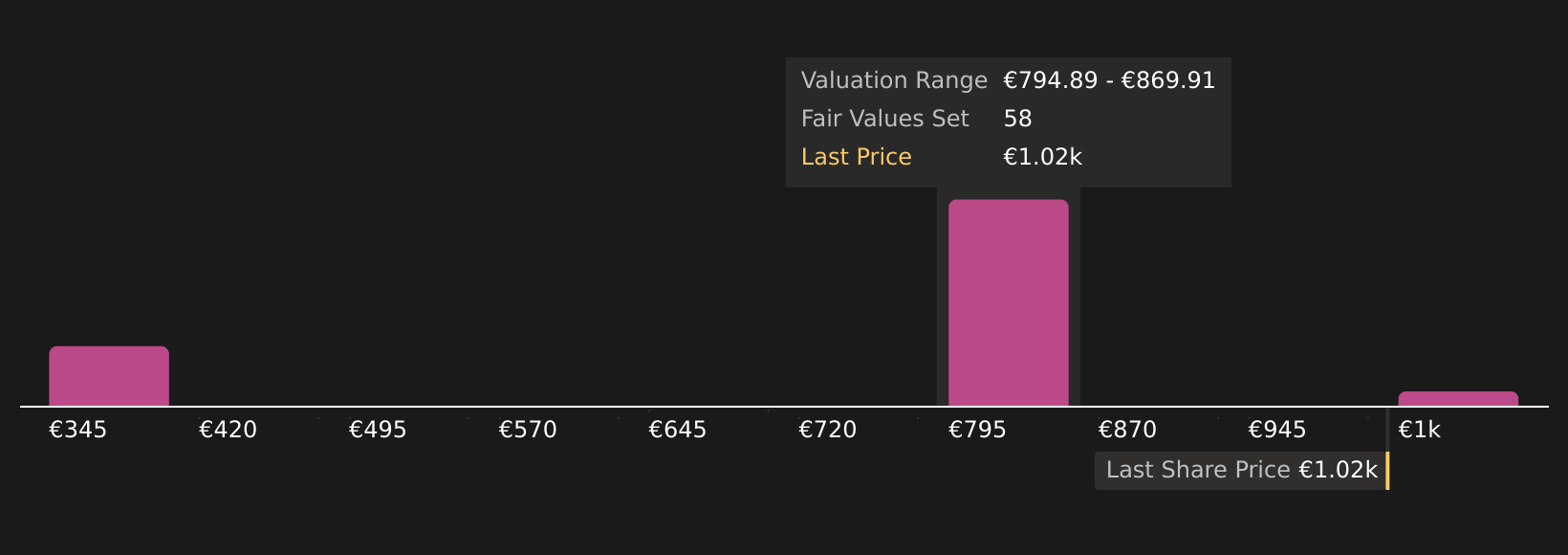

ASM International's outlook anticipates €4.6 billion in revenue and €1.1 billion in earnings by 2028. This assumes annual revenue growth of 12.0% and an earnings increase of about €573 million from the current €527.1 million.

Uncover how ASM International's forecasts yield a €597.40 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Across eight Simply Wall St Community fair value views, estimated targets for ASM International range from €262.44 to €690 per share. With current challenges in China affecting order intake, consider how much these diverse outlooks account for regional risk and whether your own expectations for growth and resilience align.

Explore 8 other fair value estimates on ASM International - why the stock might be worth less than half the current price!

Build Your Own ASM International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ASM International research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free ASM International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ASM International's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com