Is Chipotle a Smart Investment Following This Year’s 33% Share Price Drop?

Wondering whether Chipotle Mexican Grill stock deserves a spot in your portfolio right now? You are definitely not alone. Investors have been following Chipotle’s journey closely, especially given its mix of fast-casual growth and a share price that has seen both ups and downs over the past year. If you are trying to make sense of these moves and what they mean for value, you are in the right place.

Let's talk about price action: In the past week, Chipotle shares have slipped by 5.0%. Stretch that window and you will see the stock remains basically flat over the last 30 days, up just 0.4%. Looking further back, the stock has dropped nearly 33.4% in the last year and is down 32.8% year-to-date. However, over the last five years, it is still up an impressive 66.4%. That long-term outperformance is a big reason why Chipotle keeps drawing attention, even as some short-term investors get nervous following management changes and evolving consumer trends discussed in recent headlines.

Against this backdrop, our latest valuation snapshot gives Chipotle a value score of 2. Out of six key valuation checks, the company is currently considered undervalued in two. So while it is not in bargain territory, there are a couple of signals suggesting upside if you look deeper. And that is exactly what we are about to do: examine the different approaches to assessing Chipotle's value, before wrapping up with what could be the most insightful way to think about its valuation today.

Chipotle Mexican Grill scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Chipotle Mexican Grill Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a method for estimating the value of a company by projecting its future cash flows and discounting them back to today’s value. In Chipotle Mexican Grill’s case, this involves looking at its Free Cash Flow (FCF), which is currently $1.45 billion, and projecting how it might grow over the next decade.

Analyst estimates, together with model extrapolations, see Chipotle’s FCF rising steadily each year. By 2029, projections put FCF at $2.48 billion. The next five years rely on analyst forecasts; from 2030 onward, growth is extrapolated based on recent financial patterns and industry expectations. This provides a longer-term perspective.

Using these projections in the DCF model, Chipotle’s estimated intrinsic value is $32.02 billion. Comparing this to the current market valuation, the DCF model indicates the stock is 25.7% above its fair value. In other words, the stock appears overvalued at present.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Chipotle Mexican Grill may be overvalued by 25.7%. Find undervalued stocks or create your own screener to find better value opportunities.

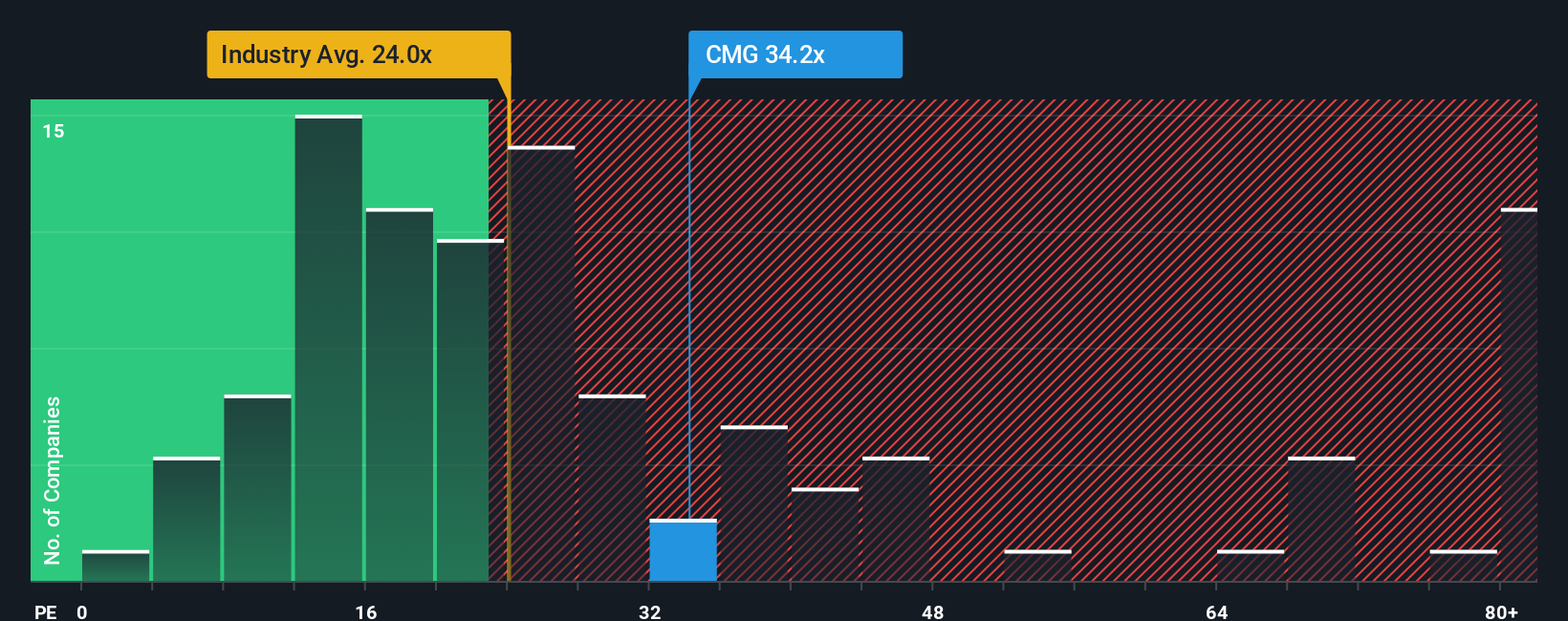

Approach 2: Chipotle Mexican Grill Price vs Earnings

For profitable companies like Chipotle Mexican Grill, the Price-to-Earnings (PE) ratio is one of the most widely used tools for valuation. It measures how much investors are willing to pay for each dollar of earnings and is especially meaningful when a company has a consistent track record of profitability, as Chipotle does.

What makes the “right” PE ratio a bit tricky is that it should reflect not only a company’s current earnings but also growth expectations and risk. Higher anticipated growth or lower risks typically justify a higher PE, while companies with uncertain prospects or more risk tend to trade at a lower multiple.

Chipotle’s current PE ratio sits at 35x. When compared to the hospitality industry’s average of 24x and the average among similar peers at 58x, Chipotle stands somewhere in the middle. This means investors are paying more than the broader industry for each dollar of Chipotle’s earnings, but less than some competitors. However, Simply Wall St’s “Fair Ratio,” which takes into account not just growth and risk but also profit margins, industry context, and market cap, suggests Chipotle’s fair PE ratio is 30x.

The “Fair Ratio” is more precise than industry or peer comparisons because it incorporates all the unique fundamental factors that shape what a company’s valuation should be. By tailoring the benchmark to Chipotle’s specific outlook and attributes, it delivers a more realistic sense of value than a simple average ever could.

Given that Chipotle trades at 35x, above its fair value PE of 30x, the stock appears overvalued on this basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Chipotle Mexican Grill Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, a powerful approach that helps you make smarter investment decisions by combining the story you believe about a company with the numbers behind it.

Narratives let you define your perspective on a stock like Chipotle by connecting your assumptions about future revenue, earnings, and margins to a fair value estimate. This creates a story that is tied directly to a financial forecast.

Available and easy to use on Simply Wall St's Community page, Narratives give you and millions of investors a simple tool to express, share, and compare your view, whether you think Chipotle is poised to thrive with international expansion or may face challenges from tougher competition and shifting consumer habits.

By comparing your Narrative’s Fair Value to the current price, you can see if your outlook suggests buying or selling, and because Narratives update dynamically with fresh news and earnings, your analysis stays relevant in real time.

For example, some Chipotle Narratives build a bullish outlook around new markets and margin growth, leading to a high fair value estimate of $65.0. Others, considering more cautious assumptions and increased risks, set a lower fair value of $46.0. This provides a practical way to see which story and valuation aligns with your own views.

Do you think there's more to the story for Chipotle Mexican Grill? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com