Unusual Machines (UMAC): Evaluating Valuation Following Major Defense Win, Expansion, and Rotor Lab Acquisition

Unusual Machines (UMAC) is in the spotlight after clinching its largest contract yet to provide drone components for the U.S. Army’s Rapid Reconfigurable Systems Line. The company is also expanding with a new motor factory in Florida and the Rotor Lab acquisition.

See our latest analysis for Unusual Machines.

This string of defense wins, growing Pentagon demand, and ramped-up U.S. motor manufacturing has supercharged Unusual Machines’ investor momentum. The share price has soared with a 49% gain over the past three months, underscoring how recent contract wins and strategic acquisitions have fundamentally shifted perceptions about the company’s growth prospects. Despite a pullback earlier in the year, the total shareholder return over the past 12 months is an eye-popping 847%. This is clear evidence that excitement is building around UMAC’s future.

If you’re interested in discovering other innovative tech and robotics players riding the current manufacturing and defense boom, see the full list for free with See the full list for free.

With shares up sharply on deal news and bullish analyst targets pointing even higher, investors are now facing the key question: is UMAC still undervalued, or has the market already priced in its next stage of explosive growth?

Most Popular Narrative: 24.9% Undervalued

With Unusual Machines last closing at $14.01 and the most popular narrative attaching a fair value of $18.67, the market may not reflect the full earnings potential these analysts forecast. The stage is set for a bold view on growth.

The buildout of new domestic manufacturing capacity for motors and headsets, alongside the ability to scale production to tens of thousands of units monthly with further ramp potential, will enable Unusual Machines to quickly fulfill large, near-term orders and provide reliable, onshore supply to B2B and government customers. This approach supports both revenue acceleration and gross margin expansion as supply chains become more efficient.

What is the hidden engine behind this high-flying valuation? The fair value projection relies on rapid top-line growth, future profit margins, and an ambitious earnings multiple. See for yourself what is fueling this bullish narrative.

Result: Fair Value of $18.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, significant risks remain, including potential delays in government contracts and execution challenges as Unusual Machines rapidly scales operations to meet high demand.

Find out about the key risks to this Unusual Machines narrative.

Another View: Valuing UMAC Against Its Book Value

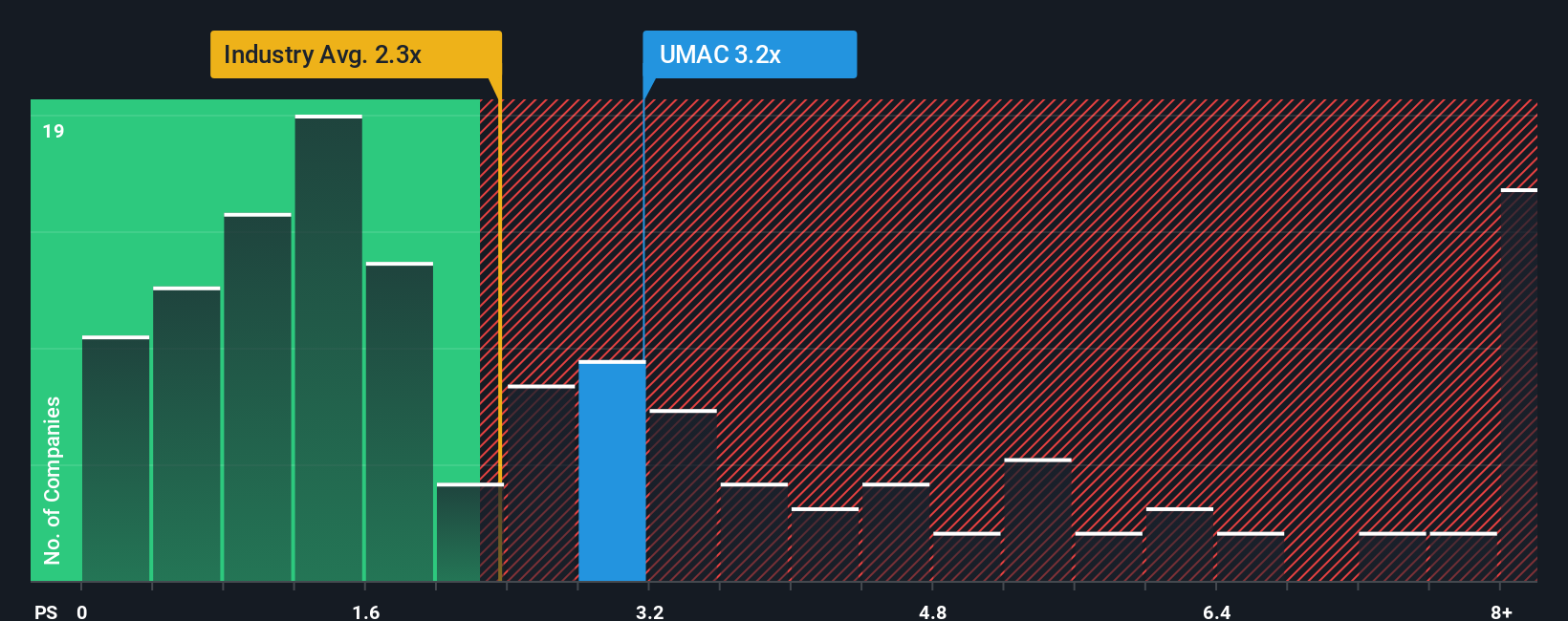

Switching to a different lens, UMAC's price-to-book ratio stands at 9x, which is much higher than both the peer average of 3.2x and the broader US Electronic industry average at 2.7x. This steeper ratio hints that shares may be priced for perfection, highlighting valuation risk if growth targets are missed. Could the market attention be running ahead of fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Unusual Machines Narrative

If you want to dig deeper or reach your own conclusion, you can craft a unique view with your own analysis in just a few minutes, so why not Do it your way

A great starting point for your Unusual Machines research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don't limit yourself to one breakthrough story; the right investments may be just a click away. Uncover winning opportunities and put your money where momentum is building.

- Snap up potential bargains by checking out these 866 undervalued stocks based on cash flows for companies showing strong fundamentals but still trading below their real worth.

- Ride the wave of innovation and take advantage of growth opportunities from these 26 AI penny stocks making headlines in artificial intelligence and automation.

- Earn while you invest by seeing which top-performing companies are offering standout returns through these 21 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com