AMD (AMD) Jumps 12.1% After $1 Billion DOE Supercomputing Win Powered by AI Technologies

- The U.S. Department of Energy and Advanced Micro Devices recently announced a $1 billion initiative to build the Lux AI and Discovery supercomputers at Oak Ridge National Laboratory, powered by AMD’s advanced GPUs, CPUs, and networking technologies, to support national AI and scientific infrastructure.

- This collaboration highlights a significant shift toward secure, sovereign AI capabilities and cements AMD's critical role in delivering next-generation high-performance computing platforms for U.S. researchers and innovators.

- We’ll explore how this landmark government partnership strengthens AMD’s investment narrative, especially through its leadership in AI-driven supercomputing.

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Advanced Micro Devices Investment Narrative Recap

To be a shareholder in AMD, you need to believe that the company can convert strong momentum in data center and AI hardware into durable growth, winning share from entrenched rivals while capitalizing on surging demand from large-scale projects like the Lux and Discovery supercomputers. The recent $1 billion Department of Energy collaboration meaningfully boosts AMD’s investment narrative in sovereign AI infrastructure, but does not immediately change the short-term catalyst: broad customer adoption of Instinct GPUs in public and private clouds. Execution risk on deployment scale remains the single largest threat, particularly if competitive or regulatory pressures intensify.

The most relevant recent announcement is AMD’s deal with Oracle to deploy 50,000 Instinct MI450 GPUs in a new AI supercluster. This partnership aligns closely with the DoE news, underlining AMD’s push into foundational AI infrastructure across both government and enterprise. Successful ramp-up and real-world adoption of these GPU platforms is critical, as customer wins beyond the headline deals will determine how much AMD can outpace expectations in the AI hardware cycle.

By contrast, investors should be aware that with increased sovereign and hyperscale demand, risks from export restrictions could still...

Read the full narrative on Advanced Micro Devices (it's free!)

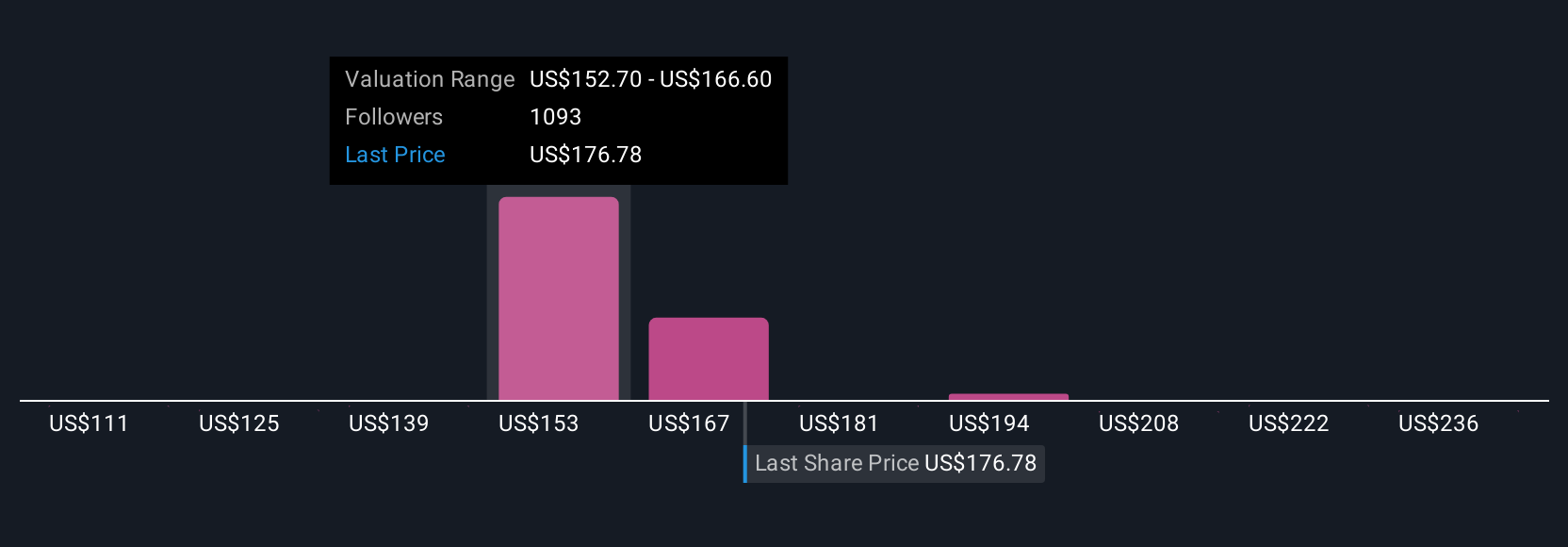

Advanced Micro Devices is projected to reach $46.2 billion in revenue and $9.0 billion in earnings by 2028. This outlook relies on an annual revenue growth rate of 18.5% and a $6.8 billion increase in earnings from the current $2.2 billion.

Uncover how Advanced Micro Devices' forecasts yield a $239.11 fair value, a 7% downside to its current price.

Exploring Other Perspectives

While the consensus expects brisk earnings growth, the most pessimistic analysts forecast AMD’s annual revenue reaching just US$44.8 billion by 2028 and earnings of US$7.2 billion, cautioning that export restrictions and supply challenges could curb AI gains. As someone weighing both sides, you’ll find that analyst expectations, and potential outcomes, are far apart, making it important to compare several viewpoints as new information emerges.

Explore 108 other fair value estimates on Advanced Micro Devices - why the stock might be worth 47% less than the current price!

Build Your Own Advanced Micro Devices Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Advanced Micro Devices research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Advanced Micro Devices research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Advanced Micro Devices' overall financial health at a glance.

No Opportunity In Advanced Micro Devices?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com