FTAI Aviation (FTAI) One-Off $262M Loss Weighs on Profit, Testing Bullish Growth Narratives

FTAI Aviation (FTAI) posted a 23.2% annual earnings growth forecast, eclipsing the US market’s 15.6% growth rate. Revenue is expected to expand at 13.3% per year, ahead of the market’s 10.1%. The company recently tipped into profitability and has managed to expand its net profit margin, but its latest financials were weighed down by a one-off $262 million loss. Over the past five years, annual earnings growth averaged a robust 53.7%, setting a strong backdrop for the future outlook.

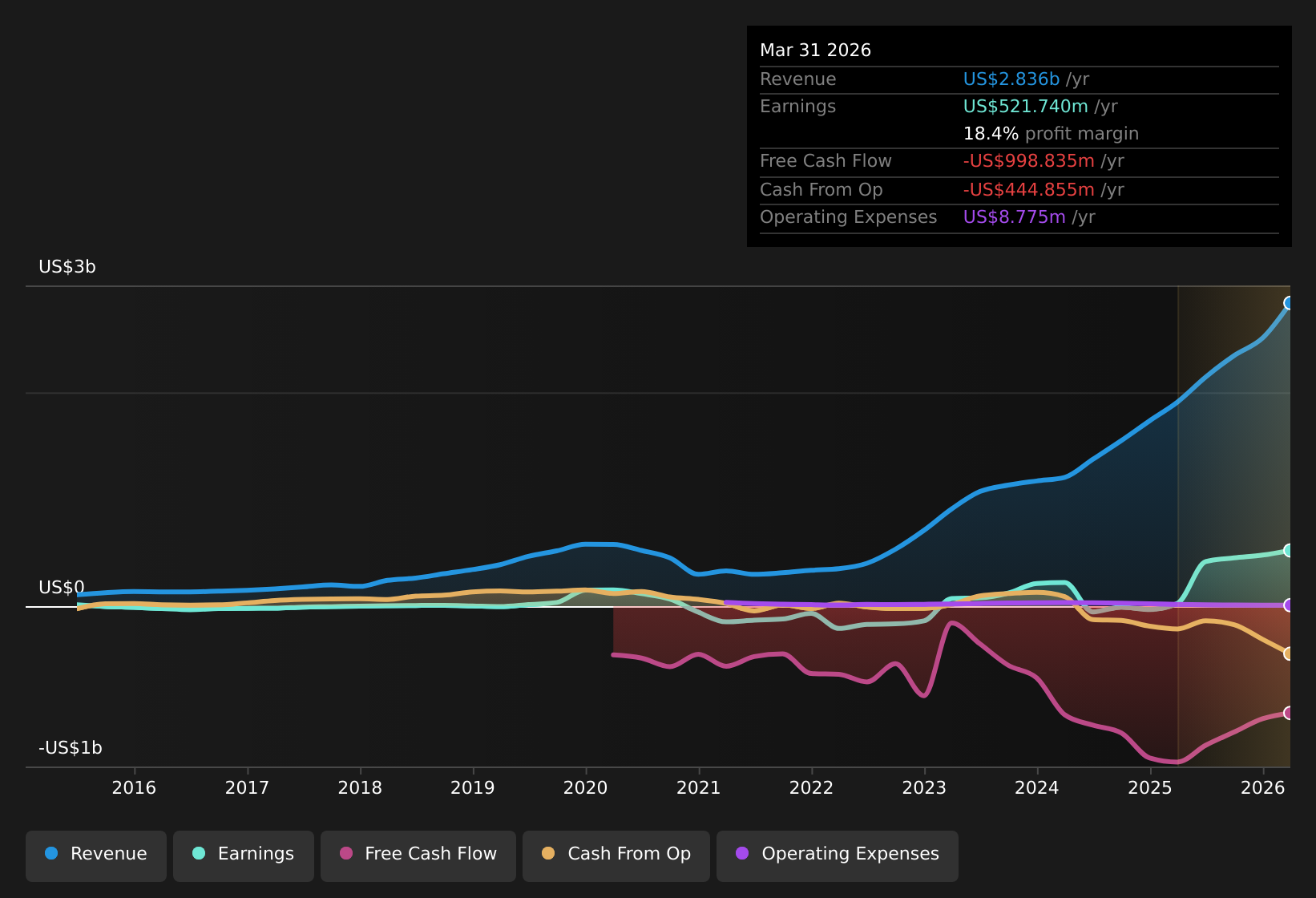

See our full analysis for FTAI Aviation.Now, let's see how these results compare to the market’s dominant narratives and whether the latest numbers reinforce or challenge prevailing expectations.

See what the community is saying about FTAI Aviation

Profit Margin Forecast Jumps to 28.8%

- Analysts expect FTAI's profit margin to climb from 19.4% today to 28.8% in the next three years, signaling a substantial increase in profitability if the company delivers on its projections.

- According to the analysts' consensus view, operational leverage and strategic partnerships are expected to support this margin expansion, but success hinges on several key assumptions:

- The anticipated ramp in vertical integration and cost efficiencies from recent acquisitions must translate into higher gross and EBITDA margins, as outlined in the consensus narrative.

- Margin growth also relies on market dynamics remaining favorable, such as ongoing demand for engine maintenance and uninterrupted operation of the Strategic Capital Initiative partnership.

What’s interesting is that the latest forecasts for margin expansion directly test whether operational leverage can turn scale into sustained profits, a key pillar of the consensus outlook. 📊 Read the full FTAI Aviation Consensus Narrative.

PE Ratio Stands at 40.7x, Well Above Peers

- FTAI trades at a 40.7x Price-To-Earnings ratio, significantly above the industry average of 22.6x, and more than double its direct peer average of 19.7x.

- The analysts' consensus view highlights this premium valuation, grounding it in high growth expectations:

- To justify such a PE ratio, analysts project that earnings will reach $1.1 billion by September 2028, implying major EPS growth from current levels.

- However, the consensus also notes that in three years' time, the company would need to trade at 23.9x on those projected earnings, still above industry norms, so any shortfall in profit or growth would put the current valuation under scrutiny.

Analyst Price Target vs. Current Share Price

- Current share price is $179.39, while the latest analyst price target is 217.20, which is 21% higher than today's price and reflects elevated expectations about FTAI's growth path.

- The analysts' consensus view frames this upside as conditional, with some projecting targets as high as $300.0 and others as low as $150.0, highlighting uncertainty:

- Achieving the midpoint target depends on revenue growing to $3.7 billion and margins lifting as forecast, but there is disagreement among analysts on the likelihood of hitting these numbers.

- With the DCF fair value at 118.64, any shortfall in earnings or margin expansion could widen the valuation gap and spark a reassessment of future growth assumptions.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for FTAI Aviation on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Looking at the data from a fresh angle? Craft your viewpoint and build your own unique narrative in just a few minutes with Do it your way.

A great starting point for your FTAI Aviation research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Despite robust earnings growth, FTAI Aviation’s high valuation leaves little room for error and could expose investors to downside if targets are missed.

If you’re wary of paying steep prices for growth, spot opportunities among these 868 undervalued stocks based on cash flows that could offer more upside with less valuation risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com