A Look at Sumitomo Metal Mining (TSE:5713) Valuation Following Winu Copper-Gold Project Stake Acquisition

Sumitomo Metal Mining (TSE:5713) has announced plans to boost capital in its subsidiary SMM PERTH PTY LTD. This move paves the way for a 30% stake in the Winu copper-gold project held by a Rio Tinto affiliate.

See our latest analysis for Sumitomo Metal Mining.

Momentum around Sumitomo Metal Mining has picked up impressively, with a 50.9% 90-day share price return suggesting renewed optimism following its latest resource expansion push. Over the past year, the company delivered a solid 25.7% total shareholder return, indicating that both short-term excitement and longer-term value creation are in play.

If news like this has you curious for more opportunity, now is the perfect time to discover fast growing stocks with high insider ownership

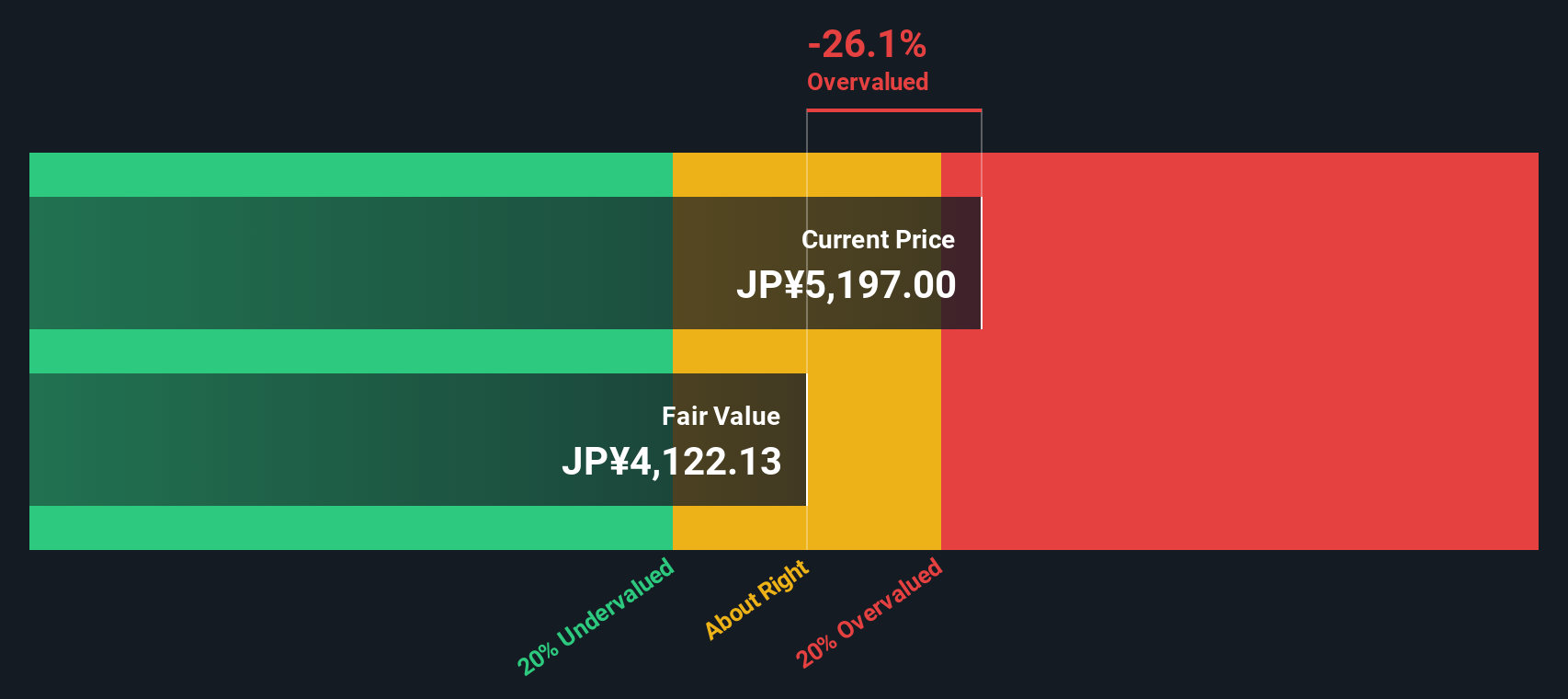

With the share price surging and major expansion moves underway, the question remains: is Sumitomo Metal Mining still undervalued, or is the market already factoring in all that future growth, leaving little room for upside?

Price-to-Earnings of 64.4x: Is it justified?

Sumitomo Metal Mining trades on a price-to-earnings ratio of 64.4x, which is sharply higher than both its industry peers and its own estimated fair value. With a last close of ¥5,197, the valuation is far above levels typically seen in the sector.

The price-to-earnings (P/E) ratio shows how much investors are paying for each yen of the company’s earnings. For Sumitomo Metal Mining, this high multiple likely signals robust future profits are expected or recent earnings have temporarily dipped. In the mining sector, investors usually look for a balance between earnings growth and stability, so outlier P/E ratios tend to stand out.

Compared to the JP Metals and Mining industry average P/E of 13.3x, Sumitomo’s ratio is much higher. The estimated fair P/E multiple is 24.9x, which highlights just how elevated the current valuation is. If market expectations recalibrate, the multiple could compress toward the fair level.

Explore the SWS fair ratio for Sumitomo Metal Mining

Result: Price-to-Earnings of 64.4x (OVERVALUED)

However, slowing revenue growth or an unexpected market correction could quickly challenge the current optimism and put pressure on Sumitomo Metal Mining’s valuation.

Find out about the key risks to this Sumitomo Metal Mining narrative.

Another View: DCF Tells a Different Story

Looking through the lens of our SWS DCF model, Sumitomo Metal Mining appears overvalued. The current share price of ¥5,197 sits well above our estimate of fair value at ¥4,461.19. This challenges the expectation of future upside seen in the high price-to-earnings ratio. Could this signal investors are paying too much for future growth?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sumitomo Metal Mining for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sumitomo Metal Mining Narrative

If you want to see the numbers from a different angle or trust your own research instincts, you can shape your own narrative in just minutes, and Do it your way.

A great starting point for your Sumitomo Metal Mining research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Ready for More Smart Investing Ideas?

Great investors do not wait for tomorrow’s headlines. Take your strategy further and unlock hidden opportunities with these tailored lists designed for forward-thinkers.

- Fuel your portfolio with untapped opportunities by tapping into these 876 undervalued stocks based on cash flows to spot companies flying under the radar and primed for potential upside.

- Amplify your returns with steady cash flow by seeking out these 19 dividend stocks with yields > 3% offering attractive yields surpassing 3% and supported by robust financials.

- Position yourself at the forefront of financial innovation by tracking these 80 cryptocurrency and blockchain stocks that harness blockchain advancements and next-generation payment technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com