Asian Dividend Stocks To Consider In October 2025

As of late October 2025, Asian markets have shown resilience amid a global backdrop of fluctuating economic indicators and geopolitical tensions. With Japan's proactive fiscal policies and China's focus on technological self-reliance, investors are increasingly looking toward dividend stocks in Asia as a potential source of steady income amidst these dynamic market conditions. A good dividend stock typically combines stable earnings with a strong balance sheet, offering investors the dual benefits of regular income and potential capital appreciation.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 5.27% | ★★★★★★ |

| Torigoe (TSE:2009) | 4.00% | ★★★★★★ |

| NCD (TSE:4783) | 4.27% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.03% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 4.04% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.40% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.46% | ★★★★★★ |

| Changjiang Publishing & MediaLtd (SHSE:600757) | 4.64% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.59% | ★★★★★★ |

| Binggrae (KOSE:A005180) | 4.60% | ★★★★★★ |

Click here to see the full list of 1023 stocks from our Top Asian Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

Samudera Shipping Line (SGX:S56)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Samudera Shipping Line Ltd specializes in transporting containerized and non-containerized cargo across Southeast Asia, the Indian Sub-continent, the Far East, and the Middle East, with a market capitalization of SGD527.28 million.

Operations: Samudera Shipping Line Ltd's revenue is primarily derived from its Container Shipping segment at $549.06 million, followed by the Bulk and Tanker segment at $28.03 million, and the Logistics segment contributing $17.59 million.

Dividend Yield: 9%

Samudera Shipping Line's dividend payments have been volatile over the past decade, though recent increases suggest potential improvement. With a low payout ratio of 11.2%, dividends are well-covered by earnings and cash flows, providing some assurance of sustainability. The company's dividend yield is in the top 25% of Singaporean market payers, but its history of unreliability may concern cautious investors. Recent business expansions indicate strategic growth efforts without impacting current financial stability significantly.

- Click here to discover the nuances of Samudera Shipping Line with our detailed analytical dividend report.

- In light of our recent valuation report, it seems possible that Samudera Shipping Line is trading behind its estimated value.

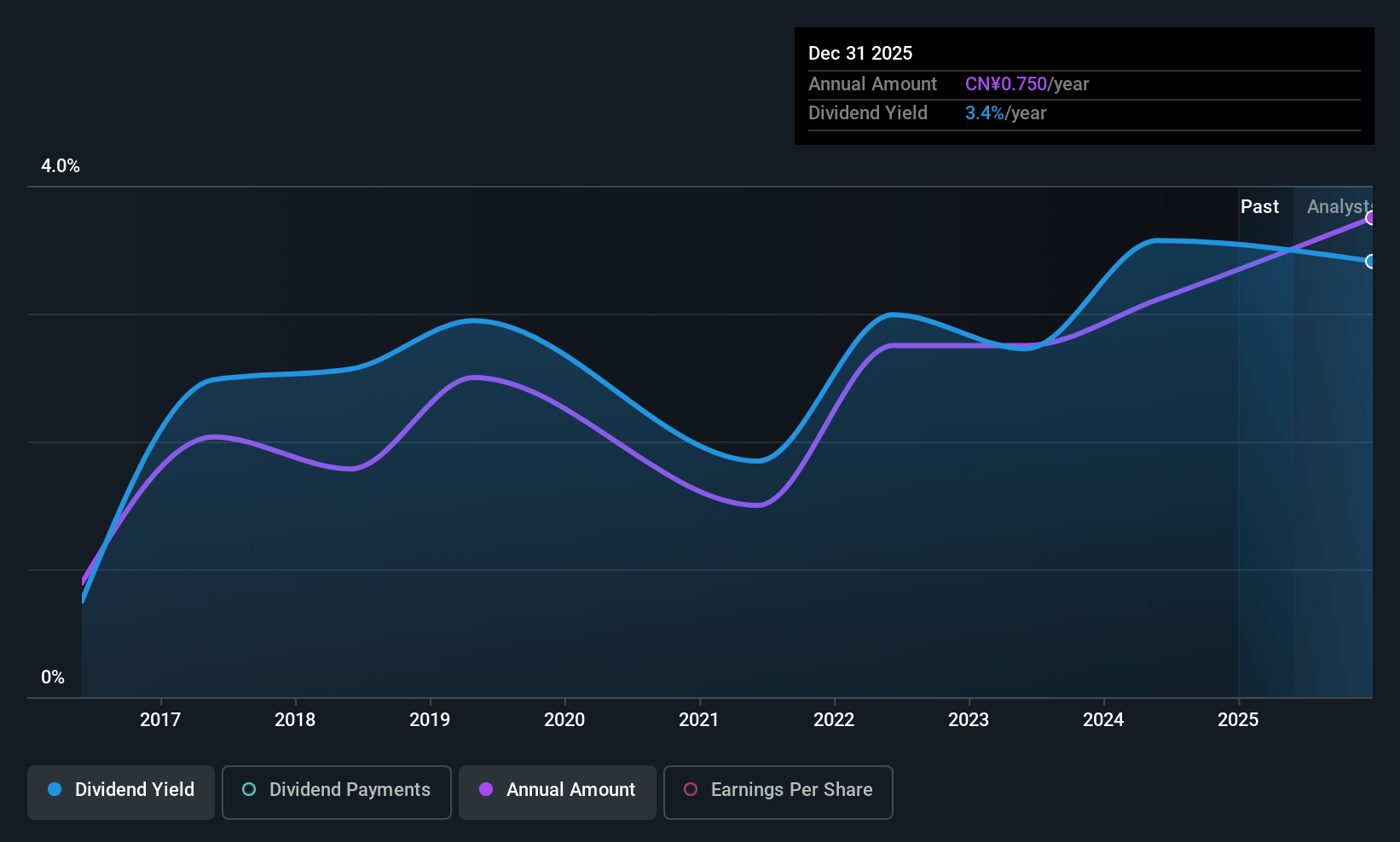

Noblelift Intelligent EquipmentLtd (SHSE:603611)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Noblelift Intelligent Equipment Co., Ltd. operates in the intelligent manufacturing equipment and smart logistics system sectors both in China and internationally, with a market cap of CN¥6.65 billion.

Operations: Noblelift Intelligent Equipment Co., Ltd. generates revenue through its operations in intelligent manufacturing equipment and smart logistics systems across domestic and international markets.

Dividend Yield: 3.5%

Noblelift Intelligent Equipment Ltd.'s dividend payments are well-covered by both earnings and cash flows, with a payout ratio of 49.6% and a cash payout ratio of 34.3%. Despite being in the top 25% of dividend payers in China, its dividends have been volatile over the past decade. The company trades significantly below its estimated fair value, suggesting potential for capital appreciation alongside dividends. Recent earnings show stable net income growth despite a decline in sales and revenue.

- Navigate through the intricacies of Noblelift Intelligent EquipmentLtd with our comprehensive dividend report here.

- Our valuation report here indicates Noblelift Intelligent EquipmentLtd may be undervalued.

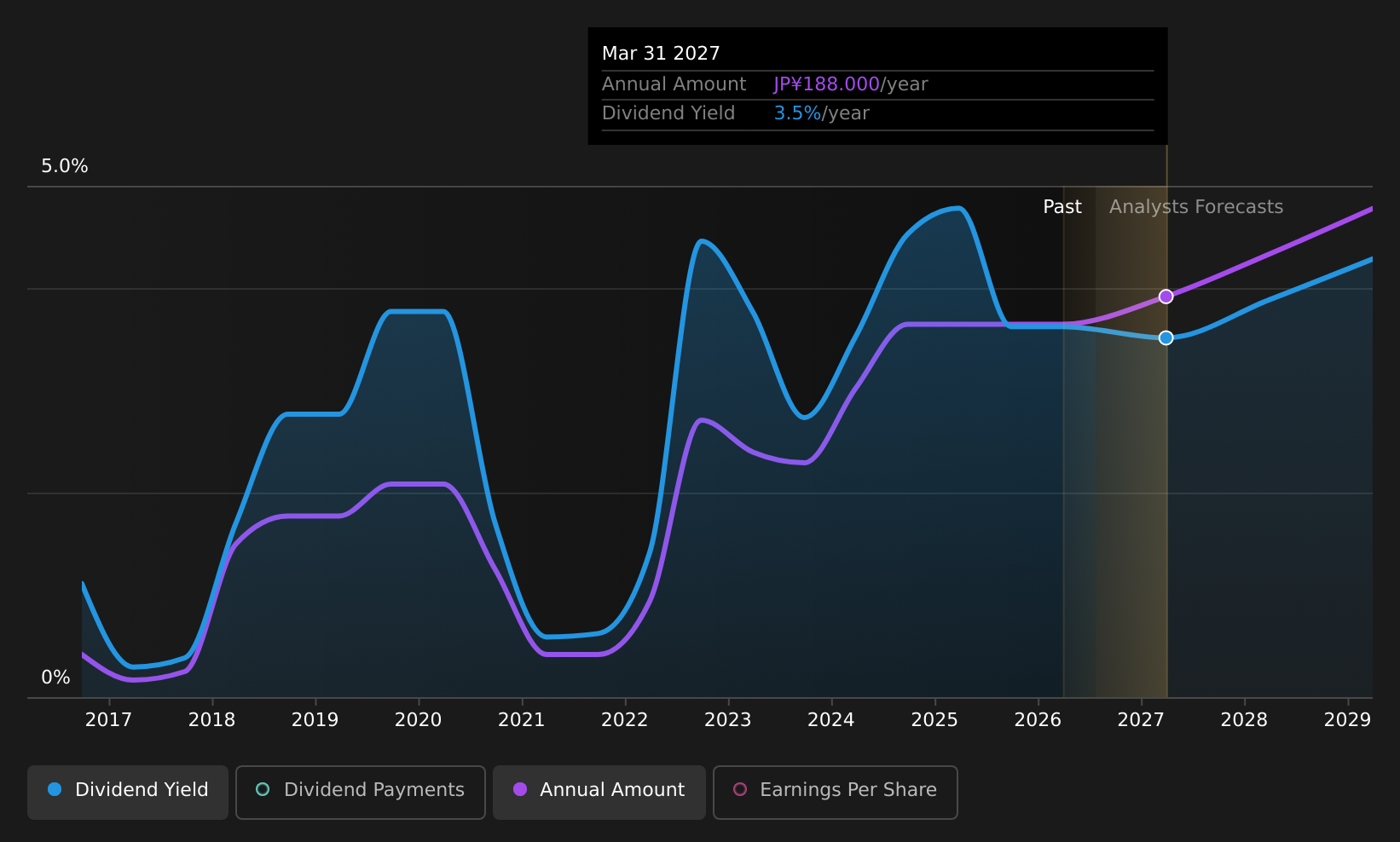

Hitachi Construction Machinery (TSE:6305)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Hitachi Construction Machinery Co., Ltd., along with its subsidiaries, manufactures and sells construction machinery globally, with a market cap of ¥1.10 trillion.

Operations: Hitachi Construction Machinery Co., Ltd. generates revenue primarily from its Construction Machinery Business, which accounts for ¥1.22 billion, and its Specialized Parts & Service Business, contributing ¥137.92 million.

Dividend Yield: 3.4%

Hitachi Construction Machinery's dividend yield of 3.38% is slightly below the top 25% in Japan, with dividends well-covered by earnings and cash flows, indicated by a payout ratio of 55.2% and a cash payout ratio of 33%. Despite past volatility in dividend payments, they have grown over the last decade. The stock trades at a significant discount to its estimated fair value, offering potential for capital appreciation alongside dividends. However, the company carries high debt levels.

- Delve into the full analysis dividend report here for a deeper understanding of Hitachi Construction Machinery.

- Our comprehensive valuation report raises the possibility that Hitachi Construction Machinery is priced lower than what may be justified by its financials.

Key Takeaways

- Dive into all 1023 of the Top Asian Dividend Stocks we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com