Fair Isaac (FICO): Assessing Valuation Following Surge in AI Patents and Innovation Momentum

Fair Isaac (FICO) was recently granted 10 new patents. This highlights the company's momentum in Responsible AI, bias detection, and fraud prevention. This expansion reinforces FICO’s capabilities and ongoing innovation across critical technology areas.

See our latest analysis for Fair Isaac.

FICO’s share price has rebounded sharply in recent weeks, jumping nearly 10% over the past month as the market seems to be taking renewed notice of its steady pipeline of innovation, including its newly announced patents. While the year-to-date share price return is still down 16%, long-term holders are well ahead, with the past three years delivering a remarkable 248% total shareholder return. This kind of momentum, paired with high-profile events such as its upcoming annual meeting, suggests investors are weighing both near-term challenges and FICO’s durable strengths.

If news of these AI patents sparked your interest, it might be the right time to see what other software leaders and innovators are on the move—See the full list for free.

With shares bouncing back and analysts predicting more upside ahead, are investors looking at a promising entry point for Fair Isaac, or has the market already factored in its next wave of growth?

Most Popular Narrative: 17% Undervalued

With Fair Isaac trading at $1,667 at last close, the most popular narrative estimates its fair value at $2,017, pointing to meaningful upside versus where the stock currently sits. These differing price targets set the stage for a deep dive into bold expectations for future growth and profitability.

The ongoing transition to SaaS and cloud-based delivery, evidenced by double-digit growth in FICO Platform ARR and emphasis on conversion to next-generation AI-driven decisioning solutions, is increasing recurring revenues, supporting margin expansion and greater earnings predictability. Sustained investment in explainable AI and machine learning, as showcased by new FICO-focused foundation models and decisioning innovations, is enhancing competitive differentiation and supporting premium product offerings, increasing average selling prices and net margins.

Curious how bold growth bets and technology upgrades shape this valuation? The narrative hinges on optimistic gains in both recurring revenues and profit margins. Find out which assumptions might surprise even veteran investors. Click through for the full breakdown driving this fair value.

Result: Fair Value of $2,017 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, regulatory shifts or new competitors such as VantageScore could threaten FICO's dominance and disrupt these upbeat expectations.

Find out about the key risks to this Fair Isaac narrative.

Another View: What Do Market Multiples Say?

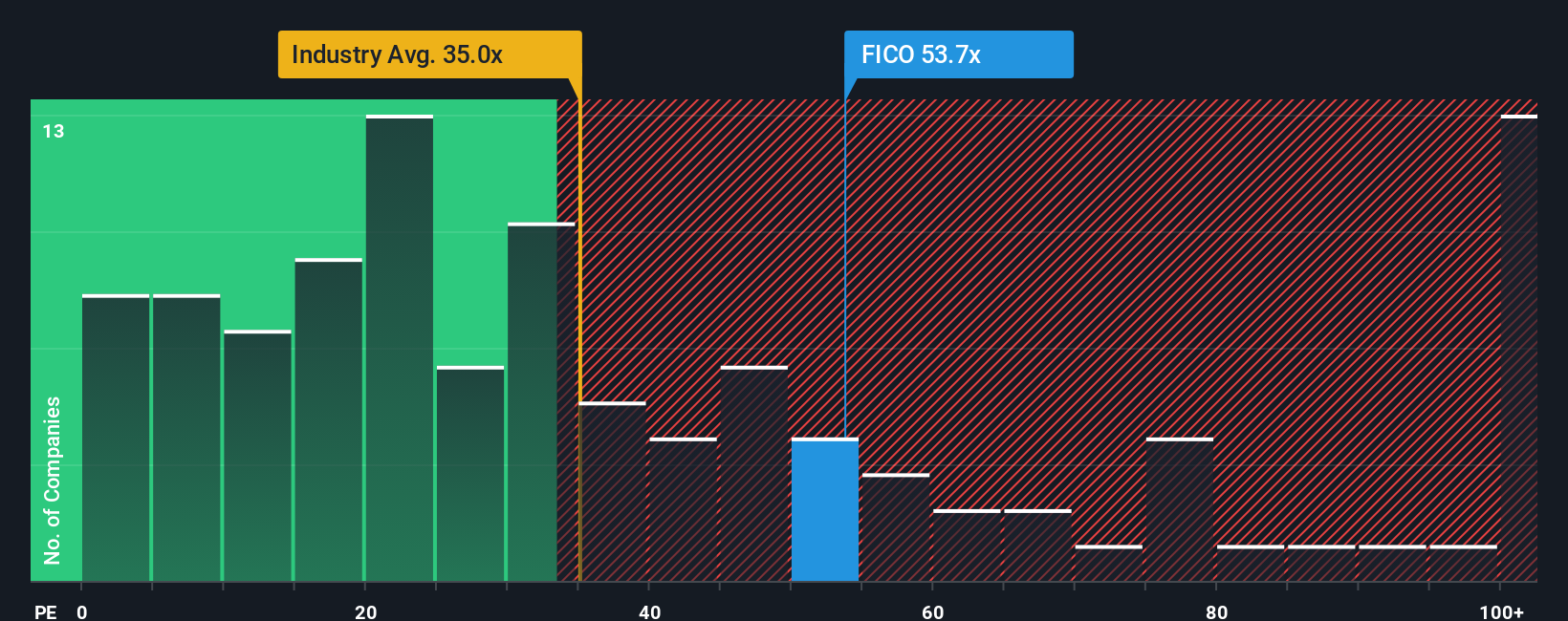

While analyst forecasts point to significant upside, traditional valuation ratios paint a more cautious picture. FICO’s price-to-earnings ratio stands at 63.3 times, nearly double the US Software industry average of 33.3 and well above its estimated fair ratio of 42.5. Compared to peers, the stock appears more fairly priced. However, by broader sector standards, investors are paying a premium. Does this higher multiple reflect enduring quality, or could it signal elevated expectations that leave less room for error?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fair Isaac Narrative

If you want to challenge these findings or dive deeper into the numbers yourself, the tools are at your fingertips for a quick, customized analysis. Do it your way

A great starting point for your Fair Isaac research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

You’re missing out if you stick to just one stock. Make your next move count by checking out these tailored investment opportunities that could give your portfolio an exciting edge.

- Boost your portfolio with passive income by starting with these 17 dividend stocks with yields > 3%, featuring companies with yields above 3% and strong payout histories.

- Tap into the future of medicine by following these 33 healthcare AI stocks, packed with trailblazing firms at the intersection of artificial intelligence and healthcare innovation.

- Seize early-mover opportunities by exploring these 3560 penny stocks with strong financials with robust financials and big potential before the broader market takes notice.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com