A Fresh Look at Coca-Cola Consolidated (COKE) Valuation After Recent Share Price Momentum

See our latest analysis for Coca-Cola Consolidated.

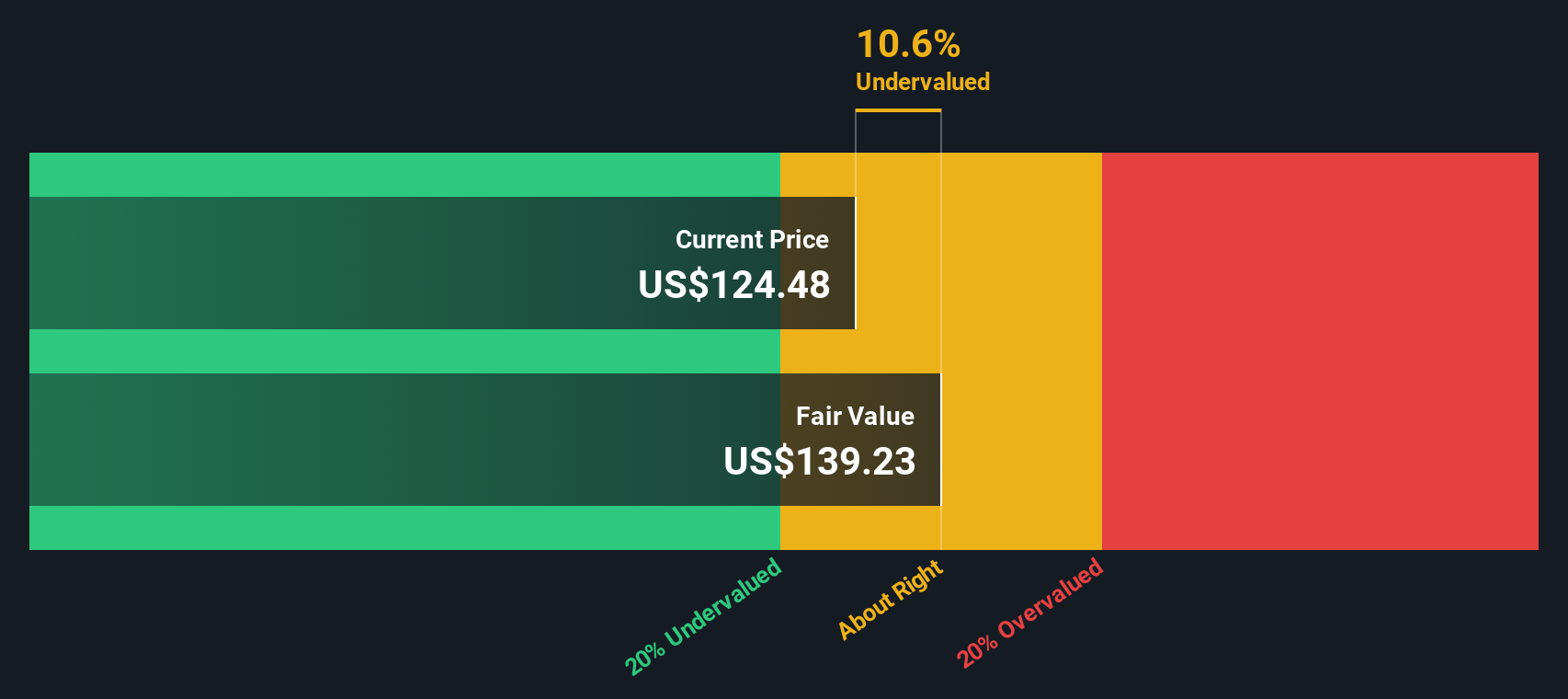

Coca-Cola Consolidated’s shares have shown renewed momentum lately, notching a 10.6% 1-month share price return even as the year-to-date move sits near flat. Looking at the bigger picture, the stock’s 3.0% total shareholder return over the past year trails its exceptional multiyear run, highlighted by a nearly 483% five-year total return. This is clear evidence of long-term value creation despite recent moderation.

If you’re interested in finding the next standout performer, now’s a perfect time to broaden your search and discover fast growing stocks with high insider ownership

With shares rebounding but long-term gains already substantial, investors now face a key question: is Coca-Cola Consolidated trading below its intrinsic worth, or is the market fully pricing in its future growth prospects?

Price-to-Earnings of 18.9x: Is it justified?

At a last close of $127.66, Coca-Cola Consolidated trades on a price-to-earnings (P/E) ratio of 18.9x, placing it above its sector’s typical valuation range and sparking debate about its premium.

The P/E ratio measures how much investors are paying for each dollar of company earnings, and is widely used to benchmark valuation for beverage companies. A higher P/E can indicate strong future growth expectations or simply a stock that is expensive relative to recent performance.

While Coca-Cola Consolidated’s P/E is well above the Global Beverage industry average of 17.4x, it is at a substantial discount to its peer group’s average of 56.7x, suggesting mixed market signals. The company’s rapid historical earnings growth and robust profitability may justify a higher valuation, but investors should consider how much of future potential is already priced in.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 18.9x (OVERVALUED compared to industry, UNDERVALUED compared to peers)

However, a lack of recent revenue or net income growth could cast doubt on Coca-Cola Consolidated’s ability to sustain its current valuation over time.

Find out about the key risks to this Coca-Cola Consolidated narrative.

Another View: SWS DCF Model Suggests Undervaluation

Looking beyond typical industry valuation measures, our SWS DCF model estimates Coca-Cola Consolidated’s fair value at $139.23 per share, which is roughly 8% higher than its current price of $127.66. This approach highlights a potential opportunity that price-to-earnings ratios might overlook. Could the market be missing something?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Coca-Cola Consolidated for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Coca-Cola Consolidated Narrative

Keep in mind, if you want a different perspective or enjoy diving into the numbers yourself, you can develop your own view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Coca-Cola Consolidated.

Looking for More Investment Ideas?

Don’t sit on the sidelines while the next big winners emerge. Explore stocks with strong fundamentals, rapid adoption, or potential to shake up entire industries today:

- Tap into robust cash flows and undervalued price points by checking out these 876 undervalued stocks based on cash flows, which are flying under most investors’ radar.

- Take advantage of major trends in healthcare by finding opportunities among these 33 healthcare AI stocks, pioneering medical innovation with artificial intelligence breakthroughs.

- Unlock potential growth by targeting income with these 17 dividend stocks with yields > 3%, offering attractive yields and reliable payouts to strengthen your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com