Record Earnings and Client Asset Growth Could Be a Game Changer for Morgan Stanley (MS)

- Morgan Stanley recently reported third quarter 2025 earnings that surpassed Wall Street expectations, with net income rising to US$4.61 billion compared to US$3.19 billion a year earlier, driven by strong performance in capital markets and wealth management.

- Management highlighted renewed client activity, record client assets, and increased investment banking engagement, signaling broad-based growth across its core businesses.

- We'll examine how this robust earnings report and record client asset growth may influence Morgan Stanley's investment narrative moving forward.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Morgan Stanley Investment Narrative Recap

For Morgan Stanley shareholders, the core thesis hinges on consistent client asset growth and sustained demand for advisory and wealth management services, despite industry headwinds like digital disruption and passive investing trends. The recent earnings beat and ongoing capital markets strength reinforce short-term momentum, but do not materially alter the primary near-term catalyst: client activity and associated fee growth. Regulatory shifts and evolving global capital rules remain the most significant risks, though the latest developments do not represent a material change in this regard.

Among the recent company developments, Morgan Stanley’s ongoing fixed-income offerings, including multi-billion US dollar corporate bond issuances with both fixed and variable coupons, stand out for their potential to reinforce the firm's capital position. These transactions provide additional flexibility to pursue growth initiatives and help manage evolving regulatory and liquidity requirements, directly tying into both opportunity and risk factors facing the business.

By contrast, investors should be aware of how increased regulatory scrutiny or sudden shifts in capital requirements could...

Read the full narrative on Morgan Stanley (it's free!)

Morgan Stanley's narrative projects $76.0 billion revenue and $17.2 billion earnings by 2028. This requires 5.0% yearly revenue growth and a $3.1 billion earnings increase from $14.1 billion today.

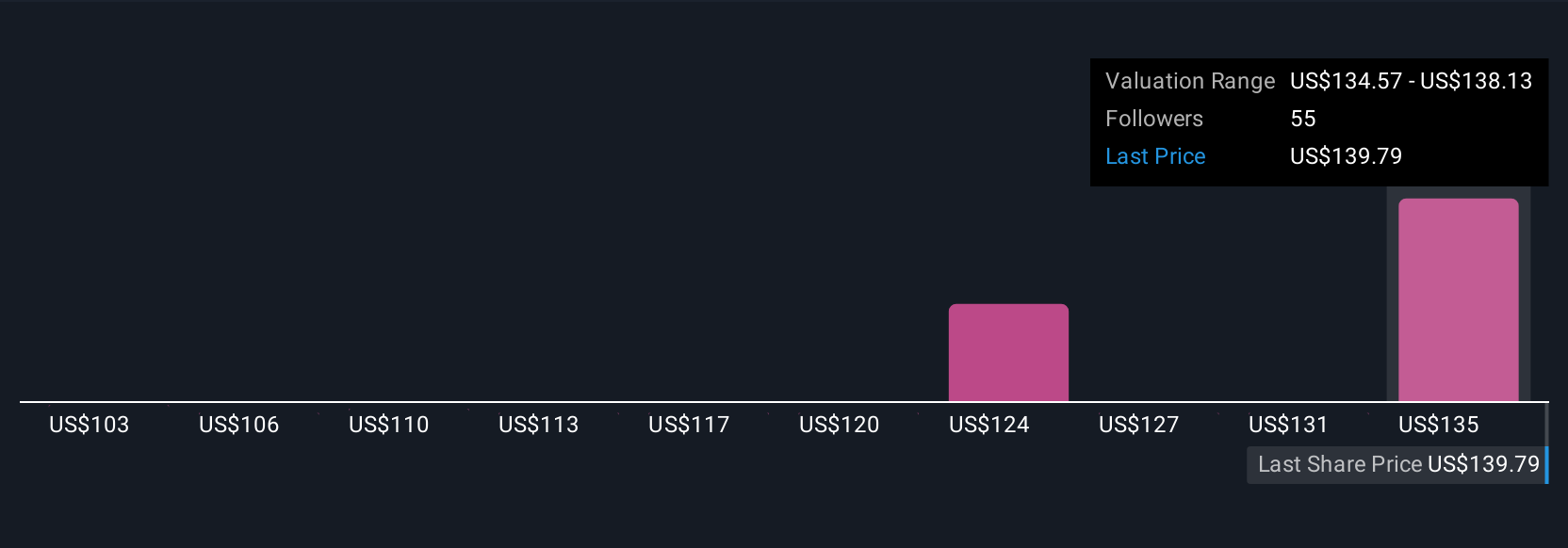

Uncover how Morgan Stanley's forecasts yield a $167.35 fair value, in line with its current price.

Exploring Other Perspectives

Fair value estimates for Morgan Stanley from the Simply Wall St Community span US$102.53 to US$167.35 across 6 opinions. Some see enhanced capital strength from recent bond offerings as supportive, but regulatory risks remain an open question for future performance, review all viewpoints to inform your own stance.

Explore 6 other fair value estimates on Morgan Stanley - why the stock might be worth 37% less than the current price!

Build Your Own Morgan Stanley Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Morgan Stanley research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Morgan Stanley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Morgan Stanley's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 37 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com