Is It Time to Consider Pan American Silver After Its 65% Rally in 2025?

Thinking about what to do with Pan American Silver stock? You are not alone. After a wild ride over the past year, a lot of investors are looking for clues about whether this surge has staying power. The stock has returned a stellar 65.2% since the start of the year and is up more than 146% in three years. That is a hefty long-term gain. Yet, in the past week, the stock pulled back by 5.6%, reminding everyone that volatility is part of the package.

Much of Pan American Silver’s recent momentum comes in the wake of industry news surrounding supply concerns and changing risk perceptions in precious metals. With silver prices remaining robust and continued chatter about potential new mine developments, excitement is building in the sector. Analysts are watching macroeconomic trends and geopolitical developments closely, as these could shift both sentiment and valuation for silver miners like Pan American.

With a current value score of 3 out of 6, Pan American is undervalued on half of the key metrics we track. This is an encouraging sign, but hardly a slam dunk. Whether this is an ideal buying opportunity or a time to lock in some profits depends a lot on how you view valuation, so let us walk through the major approaches to determining whether this silver miner is truly a bargain. Stick around to the end for a perspective even the valuation models sometimes miss.

Why Pan American Silver is lagging behind its peers

Approach 1: Pan American Silver Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and discounting them back to today, helping investors gauge whether a stock is undervalued or overvalued based on those future profits.

For Pan American Silver, the current Free Cash Flow stands at $561 million. Analyst projections suggest this will climb to about $1.3 billion in 2026, before gradually moderating to $724 million by 2035, based on Simply Wall St's extended extrapolations. These forecasts reflect the cyclical nature of the metals and mining sector, with growth expected in the next several years, then tapering off as market conditions stabilize.

Using this two-stage Free Cash Flow to Equity model, the resulting estimated intrinsic value for Pan American Silver is $51.55 per share. Compared to the current share price, this implies the stock is around 1.3% undervalued.

This slight discount places Pan American Silver almost exactly in line with its long-term fundamentals. There is no dramatic bargain, but neither is it overpriced on cash flow grounds.

Result: ABOUT RIGHT

Simply Wall St performs a valuation analysis on every stock in the world every day (check out Pan American Silver's valuation analysis). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes.

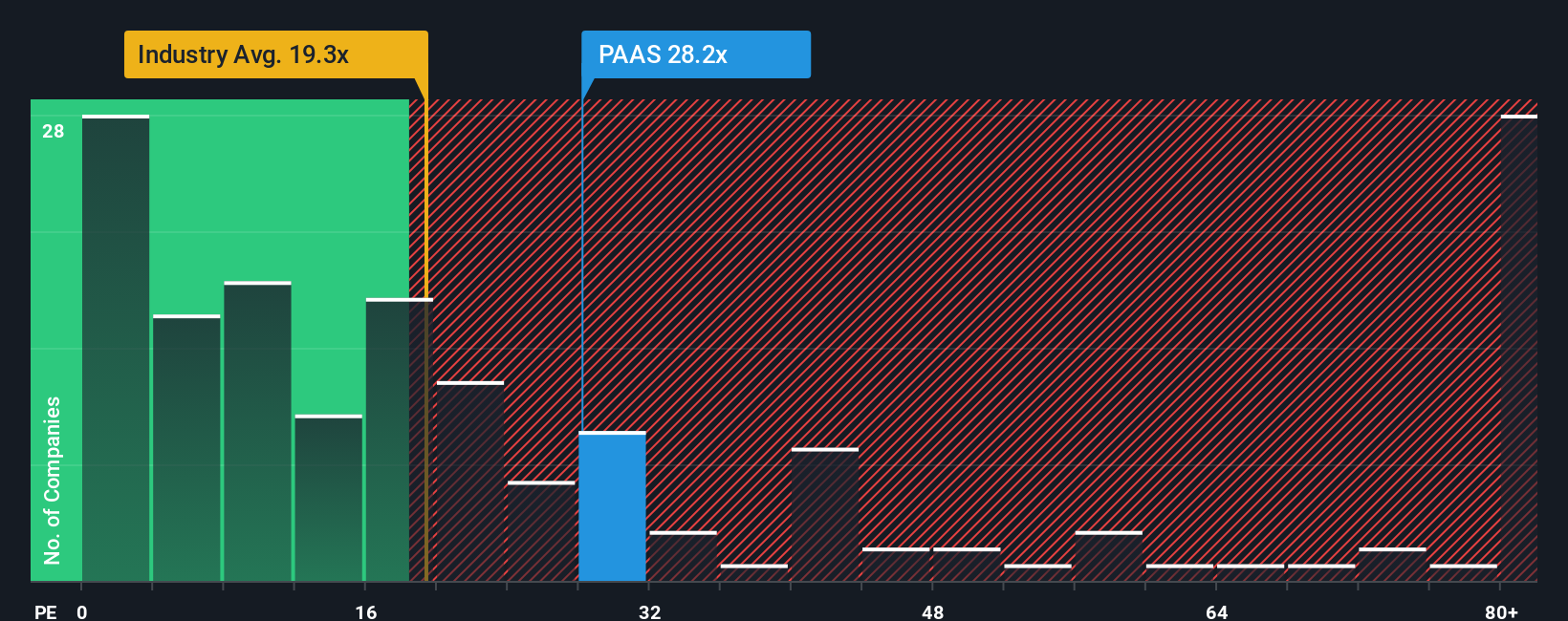

Approach 2: Pan American Silver Price vs Earnings

The Price-to-Earnings (PE) ratio is often the go-to valuation tool for profitable companies like Pan American Silver because it directly compares the price investors are willing to pay for each dollar of company earnings. It is especially useful when those earnings are sustainable and not significantly distorted by unusual items or short-term factors.

Deciding what is a "fair" PE ratio for any stock, however, is not a one-size-fits-all process. Higher growth prospects or lower perceived risk usually mean investors will accept a higher PE, while slower growth or greater risk tends to drag it lower. This highlights the importance of context when interpreting valuation multiples.

Currently, Pan American Silver trades at a PE ratio of 29.37x. For perspective, this is above the broader Metals and Mining industry average of 21.23x, but just below the peer average of 32.37x. Simply Wall St’s proprietary Fair Ratio places Pan American’s fair PE at 35.57x. Unlike simple peer comparisons, the Fair Ratio methodology considers the company’s underlying growth prospects, profit margins, risks, and its position within the industry and wider market, providing a more tailored estimate of where its valuation should reasonably sit.

With Pan American’s current PE sitting below the Fair Ratio, the valuation appears to be about right. This suggests that the stock is neither excessively cheap nor overpriced on earnings grounds.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pan American Silver Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply your story about a company, shaped by your assumptions about its future revenue, earnings, and margins. This connects the company’s journey to a financial forecast and, ultimately, a fair value estimate.

This approach goes beyond static numbers, making investing more personal and insightful. With Narratives, available right now on the Simply Wall St Community page, you can easily build and share your own view of Pan American Silver’s future, compare it to others, and see where you differ on what the stock is truly worth.

Narratives help you stay ahead by showing at a glance whether your fair value estimate is above or below the current price, so you can decide when to buy or sell. In addition, Narratives are automatically refreshed whenever new earnings or news hit the market, keeping your story and your valuation up to date.

For example, one investor’s Pan American Silver Narrative projects rapid demand growth and puts fair value above $70, while another sees operational risks and values the stock near $40. This demonstrates just how powerful Narratives can be in shaping your investing decisions.

Do you think there's more to the story for Pan American Silver? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com