Markel Group (MKL): Assessing Valuation After a Year of Steady Shareholder Returns

See our latest analysis for Markel Group.

Momentum has cooled a bit after a strong start to the year, with Markel Group’s share price settling at $1,896.18. While short-term price returns have dipped over the last month, the bigger picture remains impressive. A 20% total shareholder return in the past year highlights solid long-term performance and consistent value creation.

If Markel’s steady climb has you wondering what else is out there, consider expanding your search and discover fast growing stocks with high insider ownership

With the stock posting solid gains yet trading just below analysts’ price targets, the key question is whether Markel Group is undervalued at current levels or if the market already reflects its growth prospects.

Most Popular Narrative: 5.6% Undervalued

With Markel Group’s fair value sitting above the last closing price, the most popular analyst narrative suggests the stock could have untapped upside. The rationale comes from deep dives into the company’s transformation plans and evolving business mix.

The restructuring and re-segmentation of Markel's insurance operations, including decentralizing decision-making and aligning accountability with clear P&L ownership, is expected to drive expense efficiency and strengthen underwriting performance. This is likely to improve overall net margins and earnings as operational improvements take hold.

Want to know the secret behind this bullish valuation? It hinges on management’s radical new approach and a future earning power that could surprise even long-time investors. Find out what bold projections and industry comparisons shape this price target. See how the narrative pieces it all together.

Result: Fair Value of $2,009 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent legacy risks or ineffective execution of restructuring plans could undermine Markel’s margin improvements and challenge the current bullish outlook.

Find out about the key risks to this Markel Group narrative.

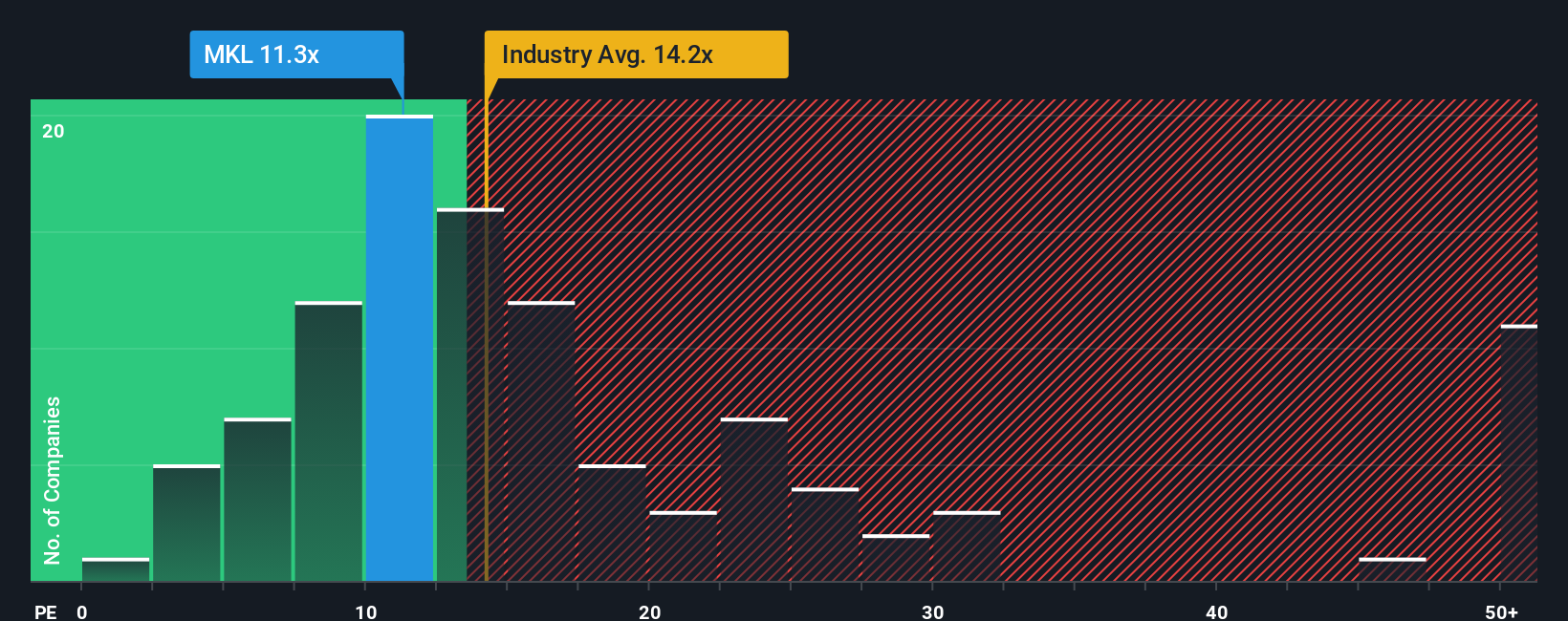

Another View: Market Multiples Paint a Good Value Picture

Taking a look at earnings multiples, Markel Group trades at 11.2x earnings, noticeably lower than both peers (17.7x) and the broader US Insurance industry average (13.9x). Even compared to the fair ratio of 11.5x, shares still offer relative value. Does this gap reveal opportunity, or are expectations for future growth simply lower?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Markel Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Markel Group Narrative

If you have a different perspective or want to dive into the numbers yourself, it’s simple to craft your own narrative in just a few minutes. Do it your way.

A great starting point for your Markel Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an open mind to new opportunities. Level up your watchlist today and don't let standout growth stocks slip through your fingers.

- Capture potential long-term gains by tapping into these 876 undervalued stocks based on cash flows with strong cash flow and attractive entry points.

- Ride the next wave of healthcare evolution by accessing these 33 healthcare AI stocks that are setting the pace for AI-driven medical breakthroughs and innovation.

- Target superior income streams and bolster your returns through these 17 dividend stocks with yields > 3% which reward investors with yields greater than 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com