Is Fiserv a Bargain After Tumultuous 39% Share Price Drop in 2025?

Trying to figure out what to do with Fiserv stock? You are not alone. This payments and fintech powerhouse has had a rollercoaster ride recently, leaving both bulls and bears re-examining their convictions. Just this past week, the share price climbed 3.4%, bouncing back after a recent dip, but that hardly tells the whole story. Over the past month, Fiserv is down 4.0%, and if you zoom out to the year-to-date, the stock has fallen a jaw-dropping 39.2%. For anyone holding on since last year, the 38.1% decline stings, though those who committed three or five years ago still see solid gains: up 23.1% and 33.9% respectively.

What is driving these big swings? In the last several months, industry chatter has centered around shifting consumer payment trends, new regulatory considerations for digital transactions, and ongoing integration following major acquisitions. While these headlines have contributed to changes in how the market values Fiserv, they have also added uncertainty, inviting both skepticism and cautious optimism from investors.

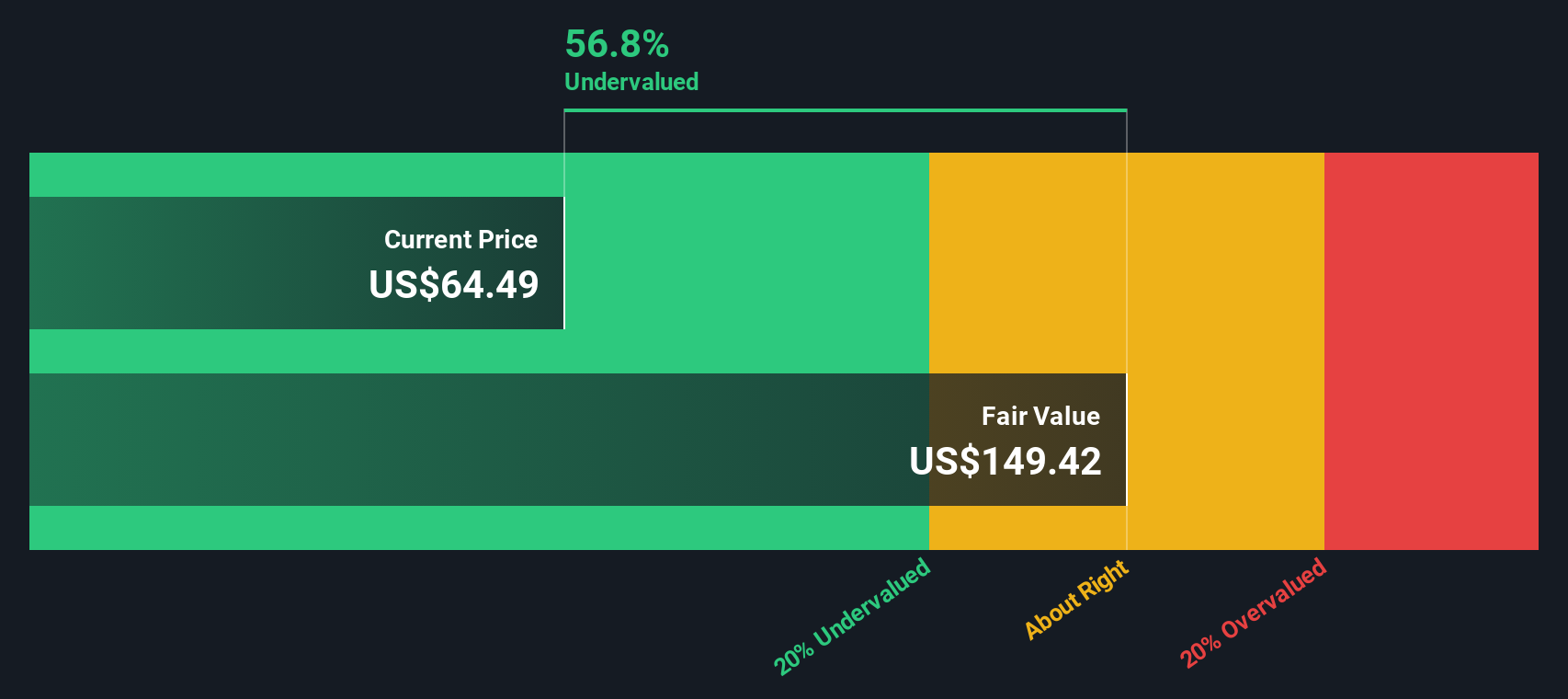

With these moves in mind, you might wonder whether Fiserv looks undervalued at the current price of $125.25. According to key valuation metrics, the company currently scores a 3 out of 6: undervalued in three checks, fairly valued or slightly expensive in the rest. But what do these valuation checks really tell us, and can they predict Fiserv's future performance? Let’s dig into several core methods for determining value, and stick around until the end for a perspective that might just be smarter than any checklist.

Why Fiserv is lagging behind its peers

Approach 1: Fiserv Excess Returns Analysis

The Excess Returns valuation model focuses on how much value a company can create beyond the cost of the capital it uses. In Fiserv’s case, analysts estimate a stable Book Value of $46.35 per share and expect it to rise to $55.18 per share in the coming years, based on three independent analyst forecasts. Meanwhile, a stable Earnings Per Share (EPS) of $12.10 is projected, grounded in weighted future Return on Equity (ROE) estimates from five analysts.

Fiserv’s average Return on Equity is notably high at 21.92%, which far exceeds its per-share cost of equity at $4.59. This results in an excess return of $7.51 per share, representing the amount Fiserv generates over what is needed to compensate shareholders for their risk. Essentially, Fiserv is using investor capital efficiently and is expected to continue delivering strong value as it grows.

Based on this analysis, the model estimates Fiserv’s intrinsic value at $198.78 per share. Compared to the current price of $125.25, the stock appears 37.0% undervalued by this approach, suggesting meaningful upside potential if the company’s performance remains on track.

Result: UNDERVALUED

Our Excess Returns analysis suggests Fiserv is undervalued by 37.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

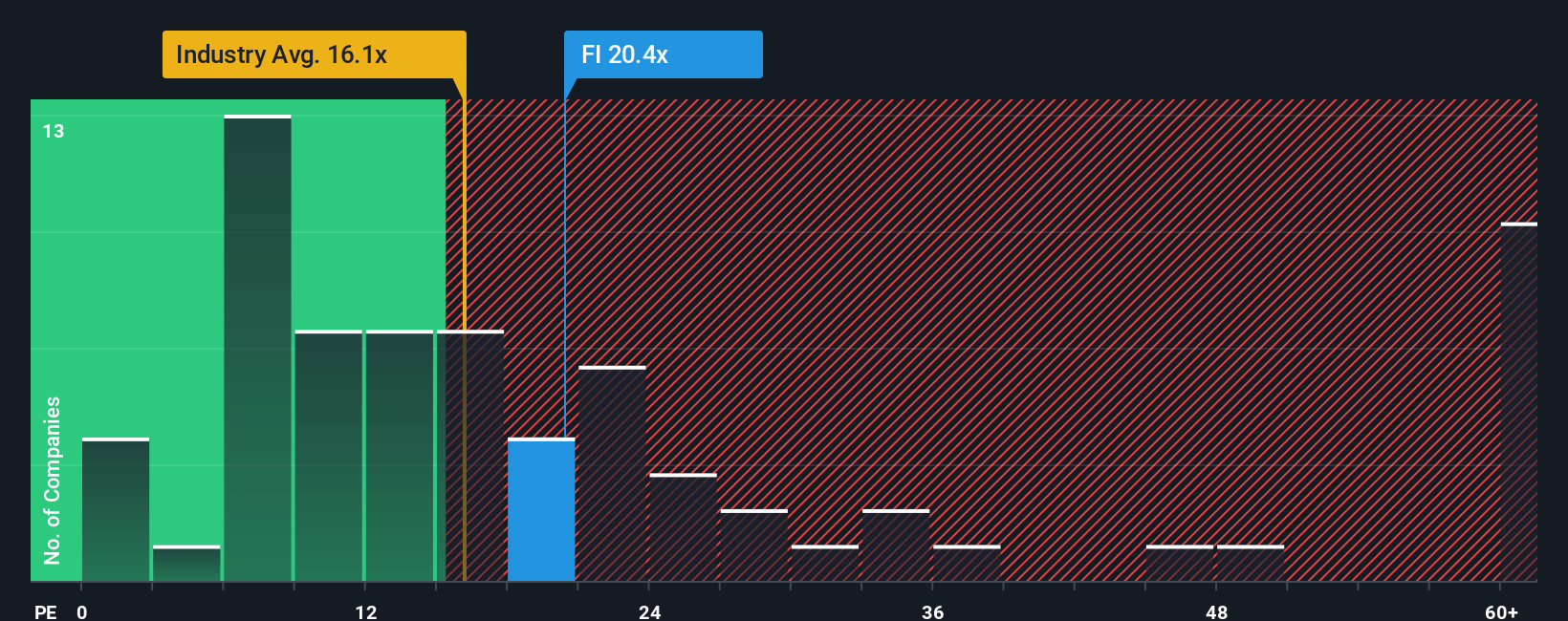

Approach 2: Fiserv Price vs Earnings

The price-to-earnings (PE) ratio is widely used for valuing profitable companies like Fiserv because it helps investors assess how much they are paying for each dollar of earnings. Since Fiserv is firmly in the black, the PE ratio provides a practical snapshot of both the company's profitability and market expectations for its future growth.

Growth prospects and perceived risks play a key role in determining what a “normal” or “fair” PE ratio should be. Higher expected earnings growth or lower risk generally justify a higher PE. On the other hand, slower growth or greater risk lead the market to assign lower multiples.

At present, Fiserv trades at a PE ratio of 20.1x. This is notably higher than the average PE for the Diversified Financial industry at 16.2x, and the peer average of 15.7x. This suggests the market is already pricing in better prospects for Fiserv compared to its competitors.

Simply Wall St’s proprietary “Fair Ratio” goes further than simple peer and industry comparisons by factoring in Fiserv’s expected earnings growth, industry dynamics, profit margins, market cap, and the company’s specific risk profile. According to this metric, Fiserv’s Fair Ratio is 21.1x. This means the company’s current valuation is closely aligned with what would be considered justified given its fundamentals and outlook.

Given Fiserv’s actual PE of 20.1x versus its Fair Ratio of 21.1x, the stock looks fairly valued using this approach.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Fiserv Narrative

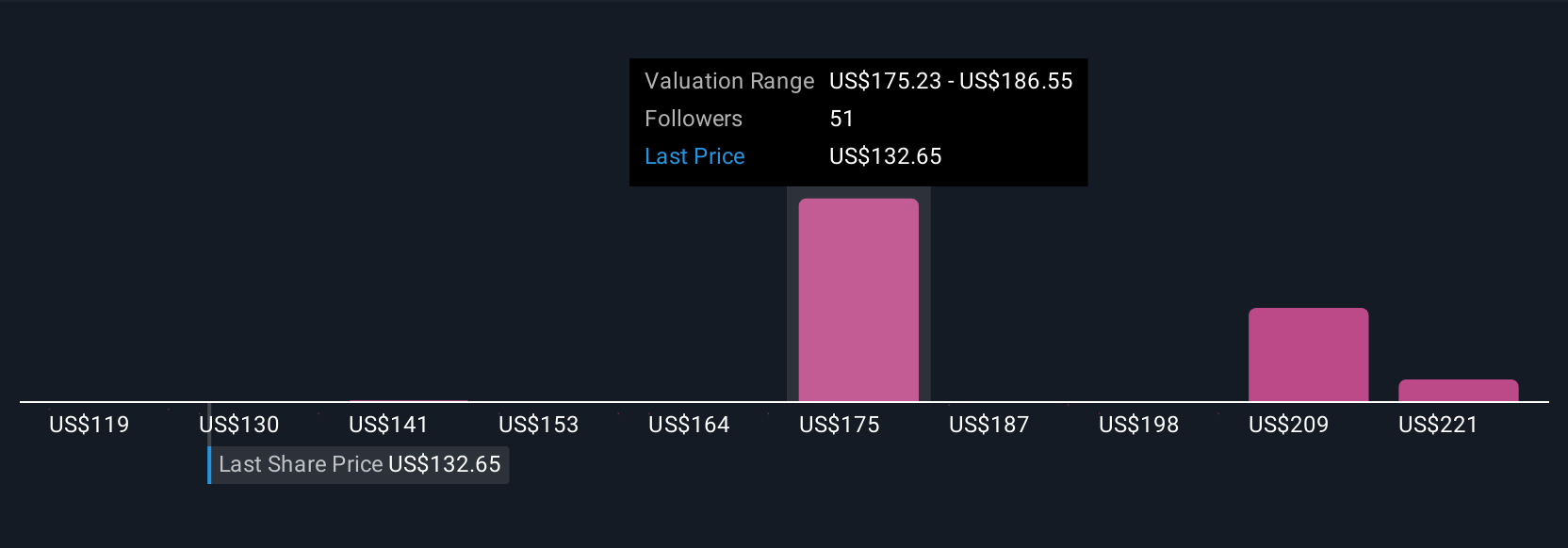

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Simply put, a Narrative combines your perspective on Fiserv’s business and future with the numbers, such as what you believe about their revenue, margin, or industry outlook, and connects that story directly to a financial forecast and Fair Value.

Narratives make investing more personal, letting you express why you think Fiserv will outperform or underperform. The Simply Wall St Community page lets millions of investors create and share Narratives in just a few clicks, so you can see a range of outlooks and transparently test your own assumptions.

Once your Narrative is saved, it instantly calculates your Fair Value and continually updates as new news or results come in, helping you track the gap between what you think the shares are worth versus the market price, and decide if it’s the right time to act.

For example, the most bullish Narrative for Fiserv today assumes aggressive global expansion and rapid margin gains, setting a Fair Value near $250 per share. In contrast, the most cautious expects earnings to stagnate and places Fair Value as low as $125, showing just how powerful it is to articulate and compare your view with others before making your next investment move.

Do you think there's more to the story for Fiserv? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com