Mercury Systems (MRCY): Evaluating Valuation After Securing Major Multi-Year Defense Contract

Mercury Systems (MRCY) announced it secured a multi-year development contract to create a multi-mission, multi-domain subsystem for a leading U.S. defense prime contractor. This deal draws fresh attention to Mercury’s role in advanced defense technology.

See our latest analysis for Mercury Systems.

Mercury Systems’ latest defense contract comes on the heels of an impressive upswing, with a 78.5% year-to-date share price return and a staggering 123.5% total shareholder return over the past year. This signals renewed momentum as the company lands high-profile opportunities.

If defense sector moves like Mercury’s have your attention, you may want to explore leaders shaping the future in aerospace and defense. See the full list for free.

With the stock trading near its analyst price targets and recent gains already on the books, investors must decide if Mercury Systems is still undervalued or if the market has already priced in this future growth.

Most Popular Narrative: 2.5% Undervalued

Compared to its last close at $75.54, the most-followed narrative points to a fair value of $77.50, based on detailed industry and financial projections. This assessment reflects a nuanced view that weighs Mercury Systems' growth strategies and sector momentum against existing operational risks.

Expanding penetration into programs that require secure, high-performance embedded processing and open-architecture modular solutions positions Mercury to benefit from the defense sector's shift toward greater digitization and AI/ML adoption. This supports higher-margin, higher-value contracts and improved long-term gross and net margins.

What financial forecasts make analysts so bullish? There is a bold profit turnaround and margin leap built into this calculation. Curious which assumptions drive Mercury’s high valuation and why the market disagrees? Discover the full narrative for the revealing answer.

Result: Fair Value of $77.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still risks, such as reliance on legacy low-margin contracts, and the possibility that recent revenue gains may not be easily repeated.

Find out about the key risks to this Mercury Systems narrative.

Another View: A DCF Perspective

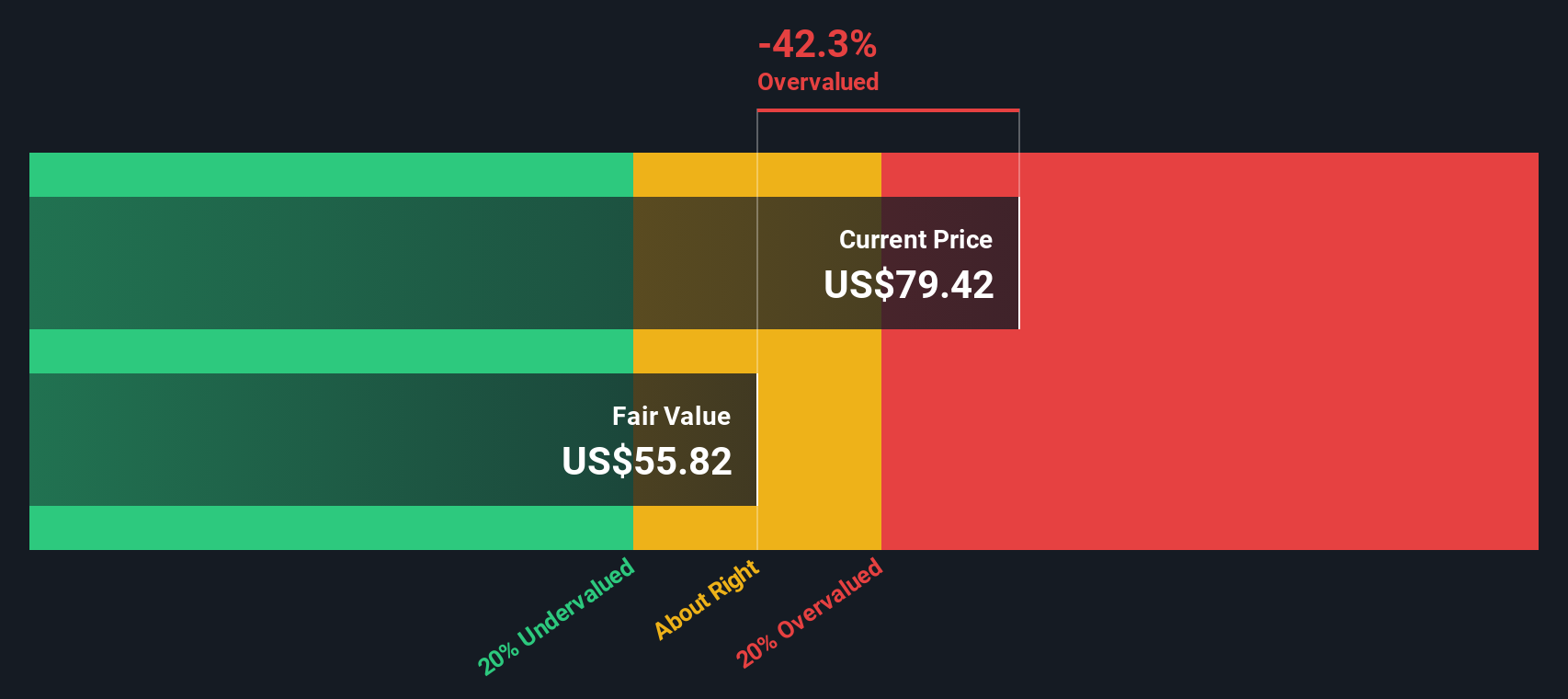

While the popular price-to-sales approach points to an undervalued stock, our SWS DCF model raises a red flag. Based on projected cash flows, Mercury Systems appears overvalued at current prices compared to its estimated fair value. Could this signal that a reality check is due for the stock?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Mercury Systems Narrative

If you see things differently or want to dig into the details yourself, you can craft a personalized Mercury Systems story quickly and easily. Do it your way

A great starting point for your Mercury Systems research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never stop at one opportunity. Don’t let the market pass you by when there are powerful trends, lucrative sectors, and undervalued gems to uncover.

- Unlock high potential by checking out these 3573 penny stocks with strong financials, offering explosive growth opportunities you won’t want to miss.

- Spot the future of healthcare by scanning these 33 healthcare AI stocks, where innovative companies blend medicine and technology for tomorrow’s breakthroughs.

- Capture gains others overlook by targeting these 875 undervalued stocks based on cash flows, filled with stocks that are priced below their true worth based on real cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com