Are Sandisk Shares Still Attractive After a 314.7% Rally Driven by Flash Memory Advances?

Thinking about Sandisk stock? You’re definitely not alone. With the share price closing at $149.29 recently, investors everywhere are asking themselves if the rally has legs or if it’s run too far, too fast. After all, Sandisk’s stock is up an eye-popping 17.3% in just the past week, and a jaw-dropping 314.7% year-to-date. Even over the last 30 days, shares have surged 46.1%. That kind of momentum grabs attention and raises big questions about what’s driving it and where the stock actually stands.

So, why the spike? The main catalyst appears to be new developments in flash memory technology, which have opened up massive opportunities for Sandisk in both consumer and enterprise markets. Investors have responded with enthusiasm, betting that these advances could supercharge future earnings growth. There’s also excitement around recent partnerships with cloud service providers, suggesting Sandisk may have found a lucrative new lane for expansion. Of course, not every news headline has been a blockbuster, but the sense that something big could be unfolding is clearly reflected in the price action.

With all that excitement, though, the big question on the table is valuation. Is Sandisk now priced for perfection, or is there still overlooked value in the stock? According to our valuation framework, Sandisk earns a value score of 2, meaning it checks undervalued boxes in two out of six key areas. But what do those checks actually represent, and is there a smarter way to gauge value? That’s exactly where we’re headed next.

Sandisk scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

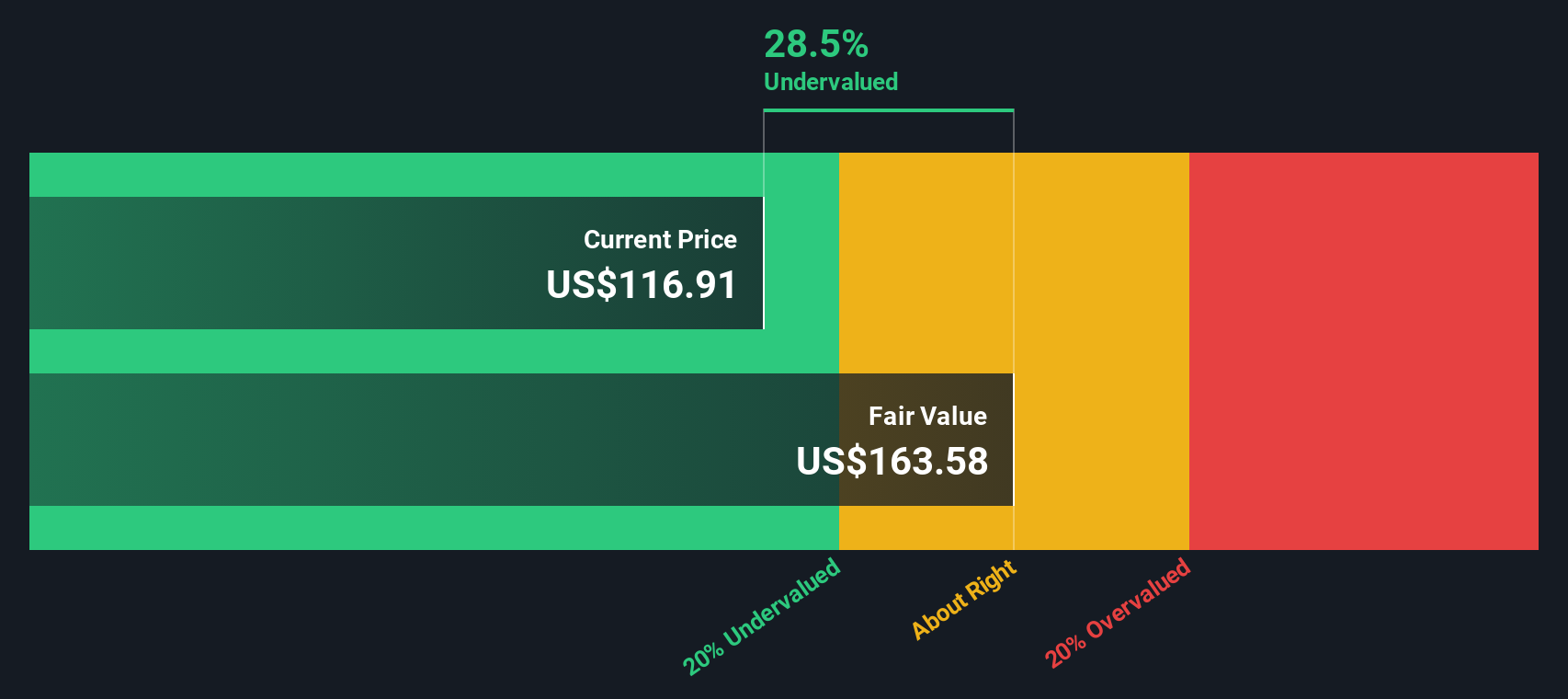

Approach 1: Sandisk Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to their value today. For Sandisk, this method looks at how much cash the business is expected to generate in the years to come and weighs those projections against the current share price.

Currently, Sandisk has a Free Cash Flow (FCF) of -$131.8 million. Analysts forecast strong growth ahead, projecting FCF to reach $1.03 billion by 2028. The model further extrapolates that by 2035, annual FCF could climb as high as $1.80 billion. These projections use a combination of analyst estimates for the coming years, with longer-term figures forecast by Simply Wall St using reasonable growth assumptions.

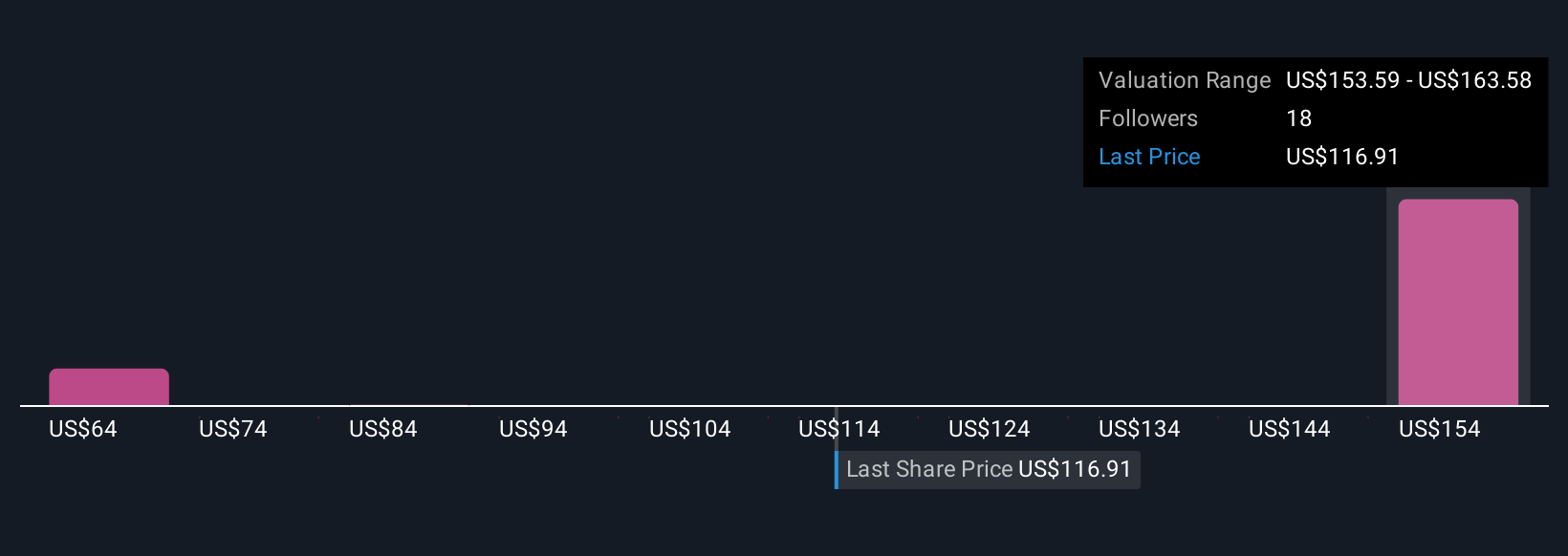

Using these cash flows, the DCF model produces a fair value estimate of $165.79 per share. This is about 10% higher than the latest closing price of $149.29, indicating that, according to this approach, the stock is currently undervalued.

Result: UNDERVALUED

Simply Wall St performs a valuation analysis on every stock in the world every day (check out Sandisk's valuation analysis). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes.

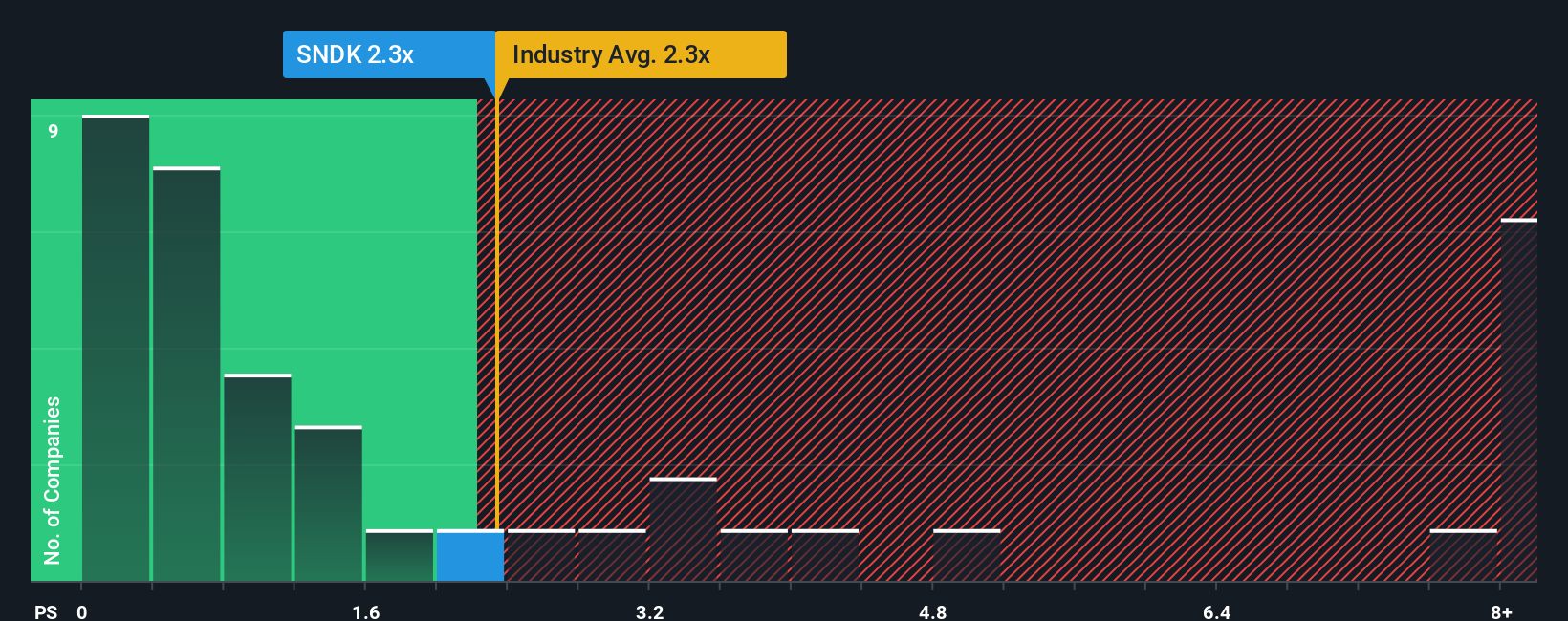

Approach 2: Sandisk Price vs Sales

The Price-to-Sales (P/S) ratio is often the preferred multiple for valuing companies like Sandisk, especially when profits are volatile or negative, but sales growth remains robust. This ratio allows investors to compare a company’s total valuation to its revenues, filtering out some of the noise of fluctuating earnings and focusing on the scale of the business relative to its market value.

Growth expectations and risk are two major factors that shape what a “normal” or “fair” P/S ratio should be. High-growth companies typically trade at higher P/S multiples, since investors are willing to pay a premium for future expansion. Conversely, higher perceived risk tends to cap the multiple investors will accept. Industry norms and peer benchmarks also play a role in setting expectations for what is reasonable.

Right now, Sandisk’s P/S ratio stands at 2.97x. That is above the tech industry average of 2.65x, but below the peer average of 3.48x. To gain a more nuanced view, we turn to Simply Wall St's proprietary “Fair Ratio,” which weighs factors like the company’s future growth prospects, risks, profitability, and market cap to derive a tailored benchmark. In Sandisk’s case, the Fair Ratio is 2.81x. This approach goes deeper than simple peer or industry comparisons by considering what truly sets the company apart or adds to its risk profile.

Comparing Sandisk’s actual P/S ratio (2.97x) to its Fair Ratio (2.81x), the difference is just 0.16. That places the stock slightly above its fair value based on this metric, but not by much.

Result: ABOUT RIGHT

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Sandisk Narrative

Earlier we mentioned there is an even better way to understand valuation. Let's introduce you to Narratives. A Narrative is simply your story of what you think a company can achieve, using your own view of where its revenue, profit margins, and fair value could go. Narratives help you connect the dots between a company’s business story, financial forecasts, and what you believe its shares are worth today.

Rather than relying only on traditional models, Narratives let you factor in your perspective and assumptions, making valuation much more personal and dynamic. These tools are easy to use and available directly on Simply Wall St’s Community page, where millions of investors refine their ideas in real time. Narratives empower you to decide whether to buy or sell by clearly comparing your Fair Value estimate against the current share price. They update automatically when new news or earnings are released.

For example, one investor’s Narrative might see Sandisk becoming a global leader, supporting a much higher fair value. Another might build in more conservative assumptions and arrive at a lower one. Narratives make it easy to see and compare these viewpoints, helping you make more informed decisions quickly.

Do you think there's more to the story for Sandisk? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com