Astellas Pharma (TSE:4503) Valuation: FDA Advancements Spark New Optimism for PADCEV Plus KEYTRUDA Therapy

Astellas Pharma (TSE:4503) and Pfizer just received U.S. FDA acceptance for their supplemental application to use PADCEV with KEYTRUDA as both a neoadjuvant and adjuvant therapy in muscle-invasive bladder cancer patients who are not eligible for cisplatin.

See our latest analysis for Astellas Pharma.

This FDA milestone for Astellas Pharma arrives following multiple noteworthy updates, including strong clinical trial results for cancer and macular degeneration therapies, and a recent conference spotlight. Notably, while the share price has climbed 9.3% over the past 90 days and 6.6% year-to-date, the one-year total shareholder return remains slightly negative, suggesting that momentum may be building after a challenging stretch.

If Astellas’ recent breakthroughs have you watching the healthcare sector, now is the perfect time to discover fresh opportunities with the See the full list for free.

Given these strong clinical and regulatory advances, is Astellas Pharma’s current valuation overlooking what lies ahead? Alternatively, has the recent uptick already factored in much of the prospective growth for investors?

Most Popular Narrative: 7.1% Undervalued

The most widely followed narrative sees Astellas Pharma’s fair value around ¥1,750, slightly above the last close of ¥1,628. This modest margin could signal reacceleration potential, though conviction depends on bold catalyst assumptions. Here is a key argument from the narrative driving this outlook:

Cost optimization and accelerated R&D productivity are enhancing profitability, with partnerships and emerging market uptake offering further upside to future earnings. Pricing pressures, patent expirations, concentration risk, execution challenges, and rising competition all threaten profitability, growth stability, and long-term market leadership.

Want to know what powers this narrative's bullish tilt? The secret is in the profit margin jump and a future-years earnings estimate that could make other Japanese pharma giants envious. Which underlying trends and scenarios tip the scales so far from the current price? Don’t miss how these audacious projections combine for the fair value call above.

Result: Fair Value of ¥1,753 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, drug pricing pressure and looming patent expirations could quickly temper optimism. These risks could potentially shift Astellas Pharma’s outlook if they materialize.

Find out about the key risks to this Astellas Pharma narrative.

Another View: Market Multiples Tell a Different Story

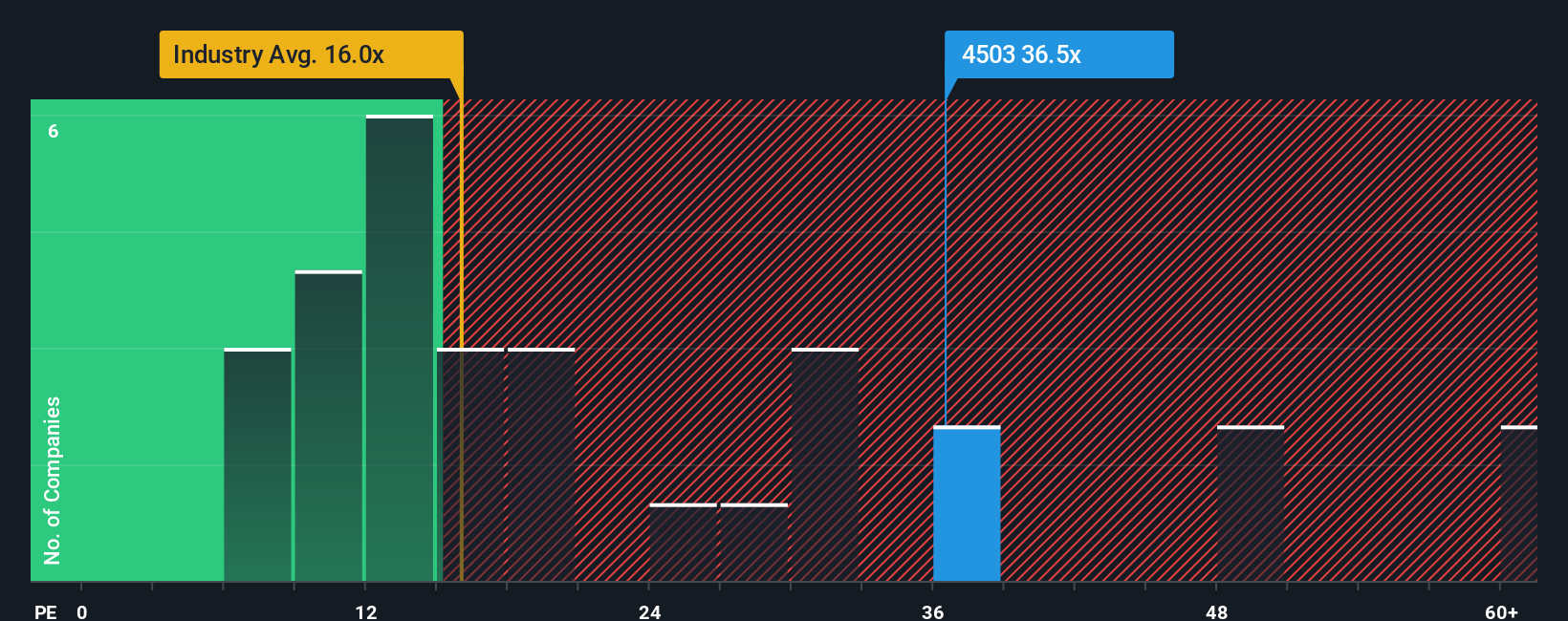

Looking from a different angle, market valuation multiples suggest Astellas Pharma might not be the bargain the first method implies. With its price-to-earnings ratio at 35.7x, the company appears far more expensive than both the industry average of 15.3x and its fair ratio of 24.3x. This premium hints at higher valuation risk if growth slows or expectations ease. Could investors be pricing in too much optimism?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Astellas Pharma Narrative

If you prefer to follow your own insights or question these perspectives, you can quickly analyze the data and craft your own view in under three minutes with the Do it your way

A great starting point for your Astellas Pharma research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Do not let fresh opportunities slip through your fingers. Now is an ideal moment to expand your search and uncover stocks set to shape tomorrow’s markets. Use these targeted screeners to find your next standout pick:

- Boost your passive income when you scan for consistent yields using these 17 dividend stocks with yields > 3%.

- Tap into innovators at the forefront of machine learning, automation, and tech breakthroughs through these 24 AI penny stocks.

- Capitalize on mispriced gems by finding companies underrated by the market with these 879 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com