Joy City Property (SEHK:207): Assessing Valuation Following New USD 150 Million Refinancing Deal

Joy City Property (SEHK:207) has entered into a new USD 150 million term loan facility with a consortium of lenders. The company aims to refinance existing debt and strengthen its capital structure. The deal closely links future loan terms to the ongoing control of COFCO Corporation.

See our latest analysis for Joy City Property.

Joy City Property’s latest loan agreement comes after a remarkable run for the shares. After a muted start to the year, momentum has surged, reflected in a 54% share price return over the past three months and a stunning year-to-date rise of 176.7%. The company’s total shareholder return over the past year stands at 142.6%, highlighting both strong medium-term gains and renewed investor confidence.

If this kind of turnaround momentum has you rethinking your own approach, why not take the opportunity to discover fast growing stocks with high insider ownership

But with shares already up more than 170% this year and the latest loan announcement attracting attention, the key question is whether Joy City Property remains undervalued or if the market has already factored in future growth expectations.

Price-to-Sales Ratio of 0.4x: Is it justified?

Joy City Property's shares trade at a price-to-sales ratio of just 0.4x, which signals the market is pricing the stock well below its industry peers.

The price-to-sales multiple compares a company’s market value to its revenues. This offers a sense of how highly or cheaply investors are valuing each dollar of sales. In real estate, where earnings can fluctuate due to large projects or one-time items, this ratio is often used as a consistent measure for relative value.

A price-to-sales ratio this low can indicate that the market is underestimating the company’s revenue-generating potential or has broader concerns about its profitability outlook. For Joy City Property, the stock stands out as good value compared to the Hong Kong Real Estate sector average of 0.7x and a peer average of 5.1x.

With a price-to-sales ratio not only lower than the sector but also much lower than the peer group, there is a considerable gap that may close if sentiment shifts or fundamentals improve.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Sales of 0.4x (UNDERVALUED)

However, persistent losses and the absence of clear annual revenue or income growth trends could challenge the case for Joy City Property's continued strong valuation.

Find out about the key risks to this Joy City Property narrative.

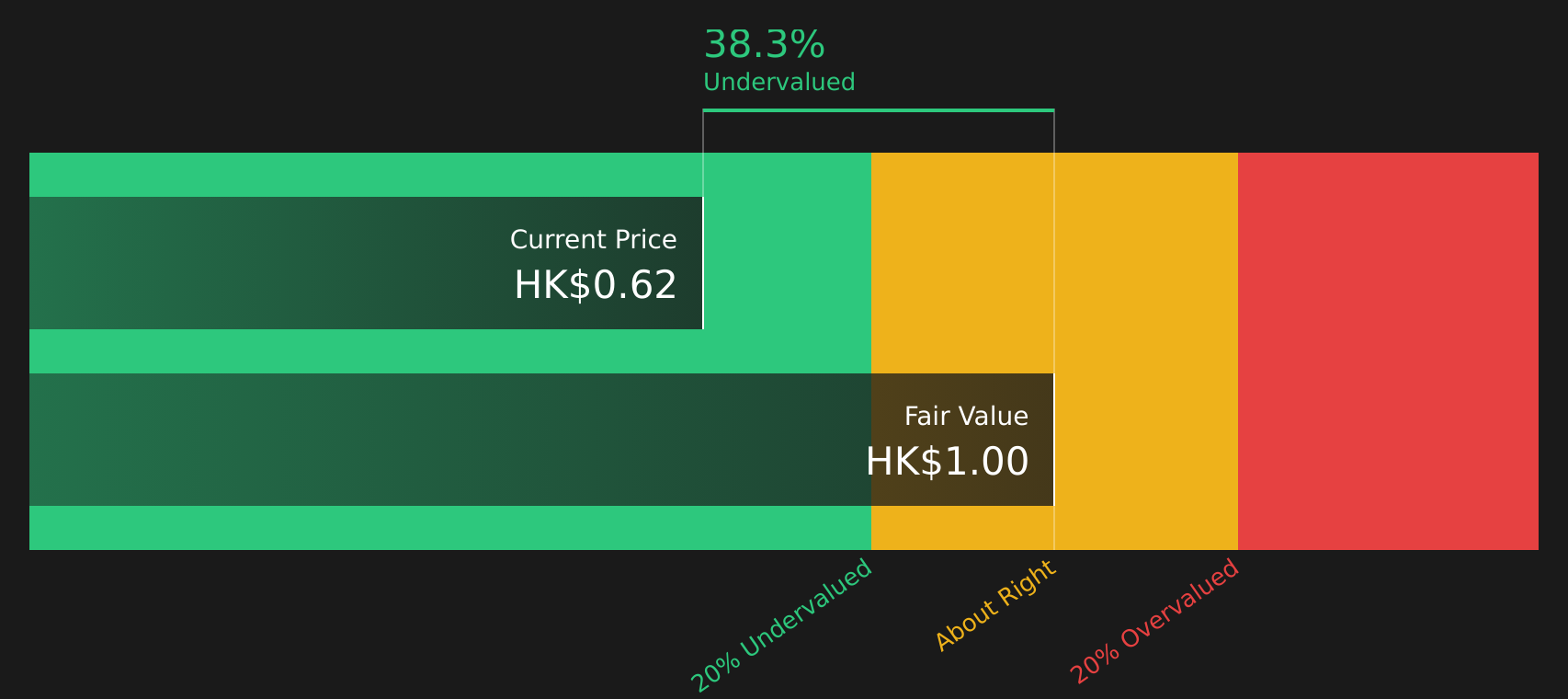

Another View: Discounted Cash Flow Model

Looking at Joy City Property using our DCF model gives a similar message. The shares are trading 42.8% below our fair value estimate (HK$1 compared to the current HK$0.57). Does this confirm a rare value opportunity, or could unseen business risks be holding back investor conviction?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Joy City Property for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Joy City Property Narrative

If you see things differently or would rather form your own opinions from the facts, you can build your own perspective using our tools in just a few minutes, so why not Do it your way

A great starting point for your Joy City Property research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock more promising stocks by targeting specific trends and opportunities. Handpicked screeners below help you uncover investments you might regret missing out on.

- Amplify your portfolio’s growth by jumping into these 873 undervalued stocks based on cash flows, which score high on future cash flow value.

- Tap into the healthcare technology boom and check out these 33 healthcare AI stocks, reshaping the future of medicine and diagnostics.

- Boost your income potential with these 17 dividend stocks with yields > 3%, offering strong yields above 3% and reliable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com