Could Payment Tech Partnerships Reshape American Airlines (AAL) Response to Industry Revenue Challenges?

- Earlier this month, American Airlines Group participated in DPW 2025 in Amsterdam, with Chief Procurement Officer Dan Bartel presenting, and separate industry commentary has captured attention regarding recent revenue trends and financial pressures facing major carriers.

- UATP's partnership announcement with Burbank aims to help airline merchants, including potential industry peers of American Airlines, reduce online payment fraud and lower associated costs through new payment technology.

- We'll now examine how ongoing revenue passenger mile weakness and debt concerns could affect American Airlines Group’s future investment outlook.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

American Airlines Group Investment Narrative Recap

To be confident as a shareholder in American Airlines Group, you must believe that recovery in air travel demand and enhancements to customer experience can offset the headwinds from a large debt burden, rising labor costs, and intensifying competition. While recent executive participation at DPW 2025 and advancements in airline payment security provide industry insight, the news does not materially change the most important short-term catalyst, stabilization and recovery in revenue passenger miles. However, the biggest risk in the near term remains the company’s high net-debt-to-EBITDA ratio, which could pressure the balance sheet during any downturn.

Among recent developments, the expanded codeshare partnership with Porter Airlines is particularly relevant. It increases cross-border connectivity between the US and Canada, supporting American's broader efforts to grow revenue through network expansion, a key catalyst as domestic demand remains uneven and international opportunities become increasingly important for future growth.

By contrast, investors should be aware that the scale of American’s debt load means...

Read the full narrative on American Airlines Group (it's free!)

American Airlines Group is projected to reach $61.8 billion in revenue and $1.8 billion in earnings by 2028. This outlook relies on annual revenue growth of 4.5% and an earnings increase of $1.2 billion from the current $567.0 million.

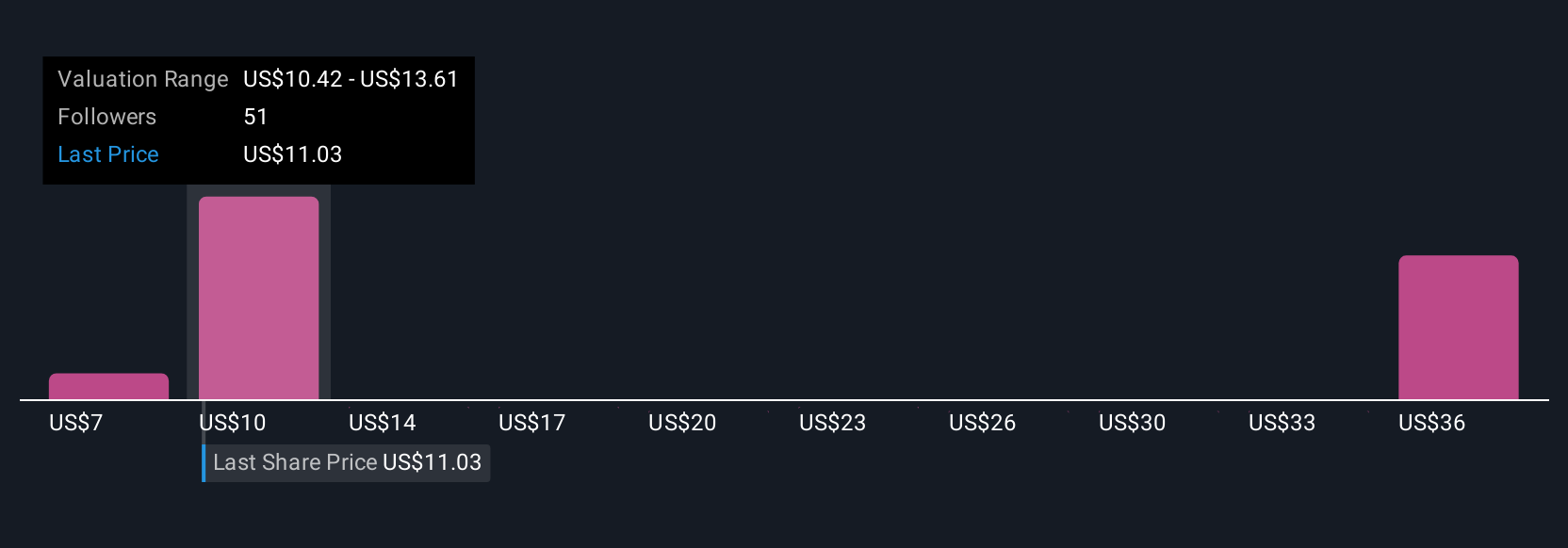

Uncover how American Airlines Group's forecasts yield a $14.23 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Ten private investors in the Simply Wall St Community have estimated fair value for American Airlines between US$7.81 and US$18.74 per share. With exposure to persistent domestic market risks, you may want to consider how varying views on structural challenges could shape the company’s outlook.

Explore 10 other fair value estimates on American Airlines Group - why the stock might be worth as much as 58% more than the current price!

Build Your Own American Airlines Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your American Airlines Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free American Airlines Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate American Airlines Group's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com