Alphatec Holdings (ATEC): Evaluating Valuation After a 13% Weekly Share Price Surge

See our latest analysis for Alphatec Holdings.

Alphatec Holdings has really stepped up in 2024, with the recent 13% weekly share price jump building on strong momentum. Its share price is now up 64% year-to-date. Investors who held on for the past twelve months have seen a 163% total shareholder return, signaling that sentiment around future growth and operational execution is running high.

If you’re curious about other healthcare names with potential, it’s worth exploring the opportunities in our See the full list for free..

But after such a strong run, is Alphatec Holdings’ rise fueled by fundamentals that still offer value, or has the market already factored in all the upcoming growth? Is there still a buying opportunity here?

Most Popular Narrative: 23.3% Undervalued

With Alphatec Holdings’ narrative fair value assessed at $19.41, and shares last closing at $14.89, there is a noticeable gap that has caught investors’ attention. Here is what is driving the narrative behind this bullish fair value.

Ongoing innovation in integrated procedural solutions and the forthcoming launch of Valence (robotics/navigation) positions the company to capitalize on the accelerating adoption of advanced healthcare technologies. This development is likely to boost both future revenue and long-term margin expansion.

Curious how this bold price target is built? The narrative’s foundation includes rapid revenue growth, rising margins, and a future profit multiple that could surprise even optimists. See which ambitious forecasts are tilting the scales toward such a strong fair value.

Result: Fair Value of $19.41 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing operating losses and fierce competition could challenge Alphatec's growth prospects. These developing risks may prompt investors to stay attentive.

Find out about the key risks to this Alphatec Holdings narrative.

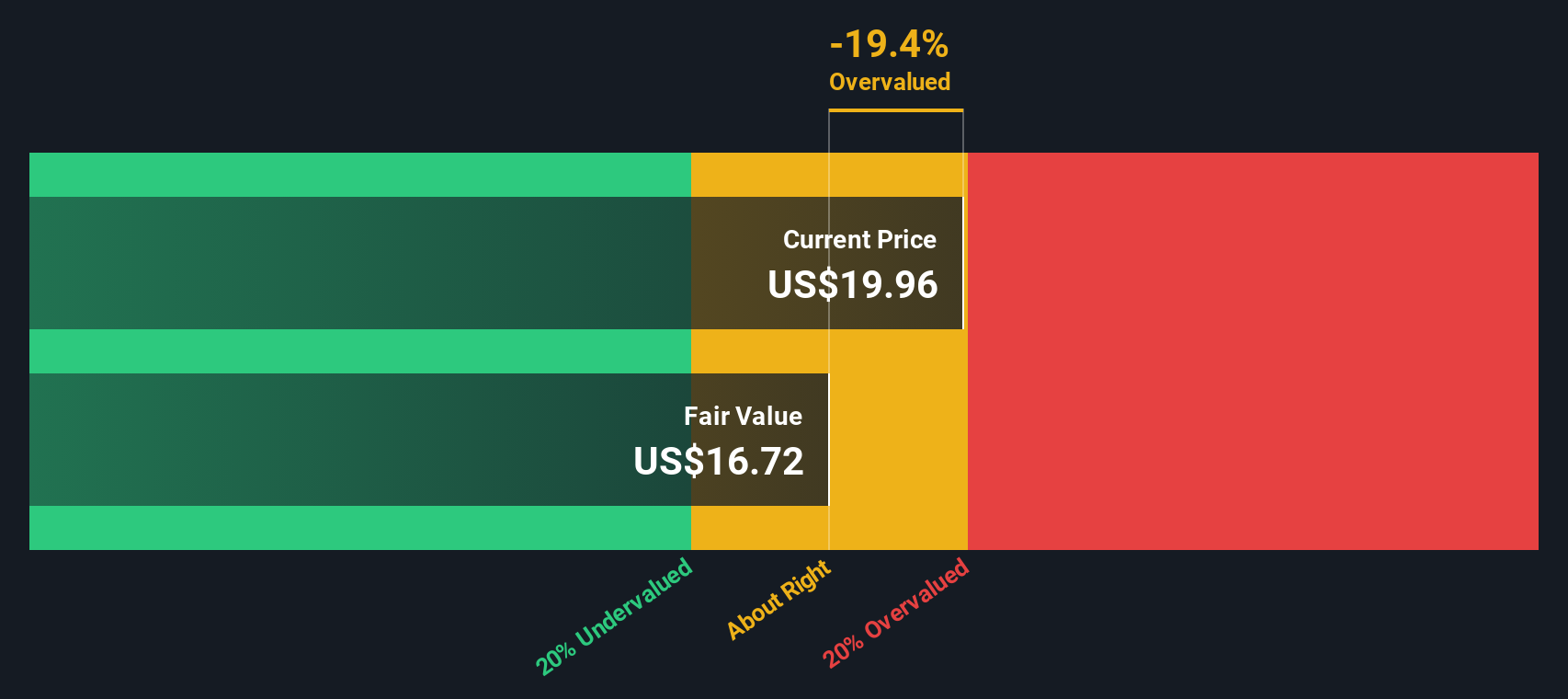

Another View: SWS DCF Model Challenges the Bullish Picture

While narrative and analyst consensus see Alphatec Holdings as undervalued, our DCF model tells a different story. According to the SWS DCF model, Alphatec is trading well above its calculated fair value of $4.41. This suggests the stock may in fact be overvalued at current prices. Does this mean the market is pricing in too much optimism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alphatec Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Alphatec Holdings Narrative

If you see things differently or want to chart your own path, you can dig into the numbers and build your own perspective in just a few minutes. Do it your way

A great starting point for your Alphatec Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don't let opportunity pass by. Seize your edge with fresh investment themes using the Simply Wall Street Screener. There could be overlooked potential hiding in plain sight.

- Unlock income opportunities and start building your future with these 18 dividend stocks with yields > 3%, offering yields above 3% for steady potential returns.

- Tap into tomorrow’s technology leaders and accelerate your strategy with these 24 AI penny stocks, featuring emerging companies in artificial intelligence breakthroughs.

- Harness quantum innovation. Take a bold step with these 26 quantum computing stocks for exposure to pioneers at the forefront of computing’s next big leap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com