How Should Investors Assess Bombardier After 96% Rally and Strong Jet Demand in 2025?

If you’ve been watching Bombardier’s stock lately, you’re probably not alone in wondering what to do next. There’s been no shortage of movement here: after a modest dip of 0.4% in the last week, shares have still climbed 7.6% over the past month. The real jaw-dropper? A nearly double return year to date, up 96%, and an astonishing five-year rally of 2,269.4%. This kind of performance has turned more than a few heads, sparking debates over whether Bombardier remains a great buy or has run too far, too fast.

Much of this momentum is tied to changing perceptions about risk and opportunity in the business jet market, along with global demand and the company’s steadfast focus on its core business. The market seems to be re-rating Bombardier’s potential, and those willing to bet early have certainly been rewarded. That said, none of this guarantees an easy or obvious path from here, and that’s where a clear-eyed look at value becomes essential.

When it comes to traditional valuation metrics, Bombardier stands out. On a scale where 1 means a company is undervalued in just one area and 6 means it’s undervalued across the board, Bombardier scores a 5. That’s an impressive result, suggesting it’s undervalued on nearly every major measure analysts track.

Let’s break down what those valuation checks actually mean for investors. And just as important, there’s a smarter way to use valuation that goes beyond the obvious. I’ll get to that further down.

Approach 1: Bombardier Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s dollars. This approach gives investors a sense of what the business is worth based on expected financial performance.

For Bombardier, the current Free Cash Flow (FCF) is $79 million. Analysts expect robust growth ahead, with projections showing annual FCF climbing steadily and reaching $1,159 million by the end of 2029. While direct analyst forecasts extend about five years into the future, numbers beyond that rely on further extrapolation but still present a continuation of the growth trend.

- 2026 projected FCF: $933 million

- 2027 projected FCF: $1,082 million

- 2028 projected FCF: $1,185 million

- 2029 projected FCF: $1,159 million

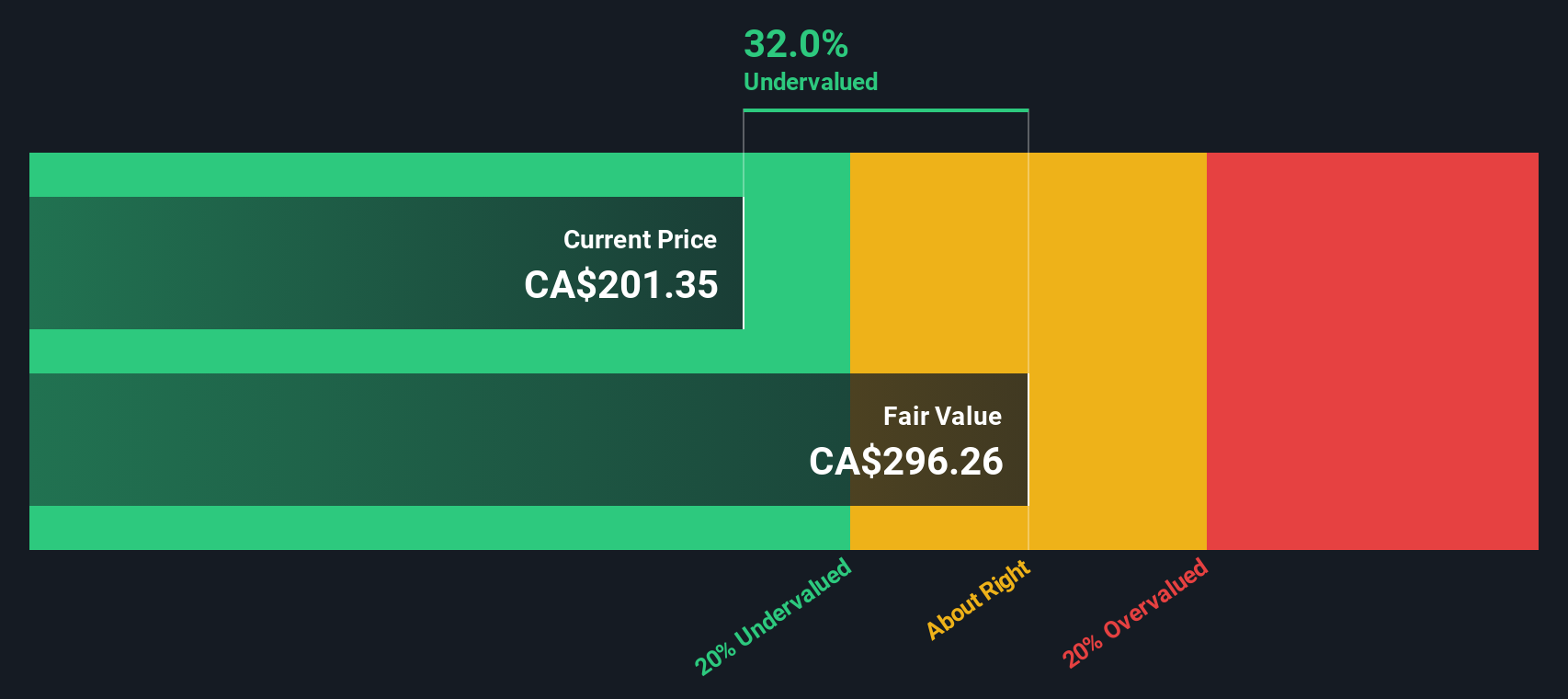

Based on these calculations, the DCF model estimates Bombardier’s fair intrinsic value at $278.39. Given the current market price, this implies the stock is trading at a 31.9% discount to its estimated value, suggesting there is significant upside for investors under these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bombardier is undervalued by 31.9%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Bombardier Price vs Earnings

For profitable companies like Bombardier, the Price-to-Earnings (PE) ratio is a widely used and intuitive measure of valuation. It tells investors how much they are paying for each dollar of earnings, making it especially relevant when the company is generating steady profits. The “right” PE ratio is not fixed; it changes with expectations for future growth and the level of risk. Fast-growing or lower-risk companies typically trade at higher PEs, while those with uncertain prospects tend to be valued lower.

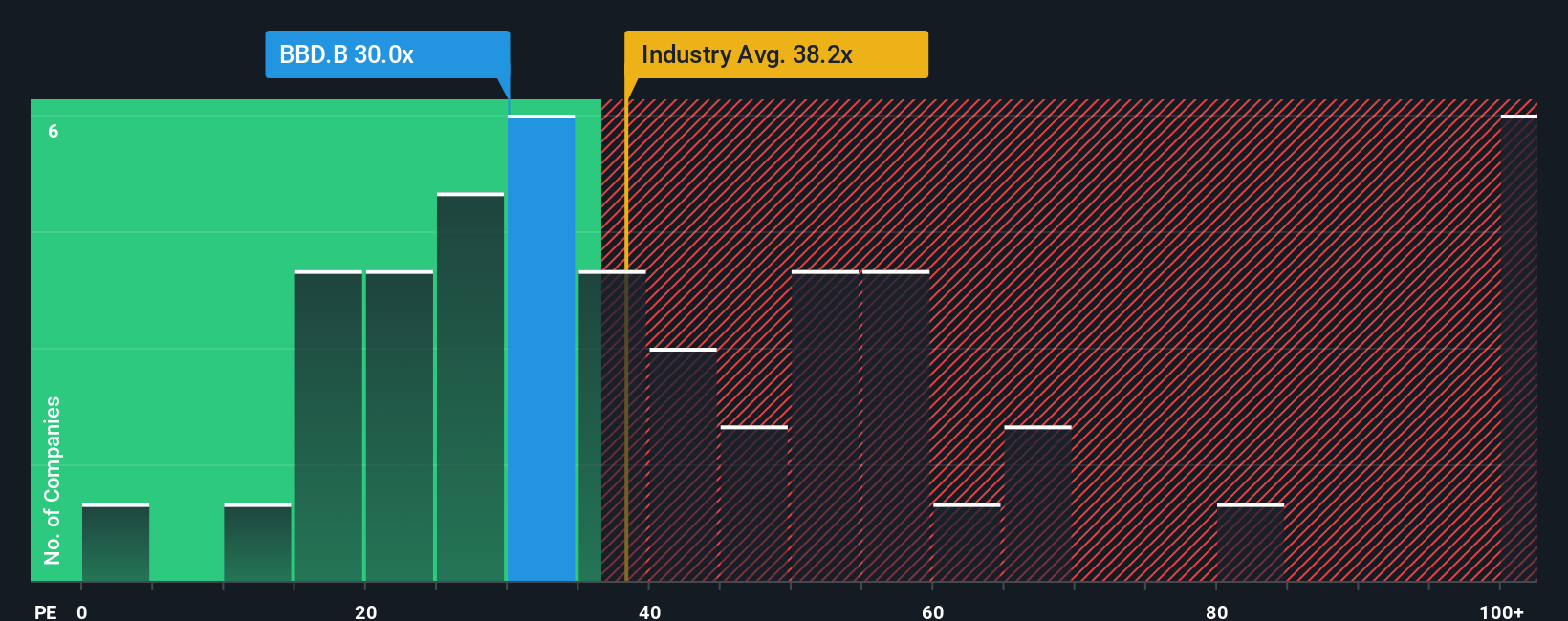

Bombardier’s current PE ratio sits at 29.9x. For context, the aerospace and defense industry average is 46.0x, while peers are around 33.1x. These benchmarks provide useful context, suggesting Bombardier trades below both its industry and immediate competitors. However, benchmarks alone can be misleading, as they do not fully account for a company’s unique profile.

This is where Simply Wall St’s “Fair Ratio” comes in. This proprietary measure goes beyond mere peer or industry averages. The Fair Ratio (35.0x for Bombardier) weighs factors such as profit margins, expected earnings growth, company size, and risk factors alongside broader industry drivers. Because it is tailored to Bombardier’s specifics, it provides a more accurate and holistic view of what a reasonable valuation should be at this point in time.

With Bombardier trading at 29.9x compared to a Fair Ratio of 35.0x, the stock appears modestly undervalued on earnings. This gap signals that investors are not overpaying for the company’s projected growth and profitability, leaving potential room for upside if fundamentals remain on track.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bombardier Narrative

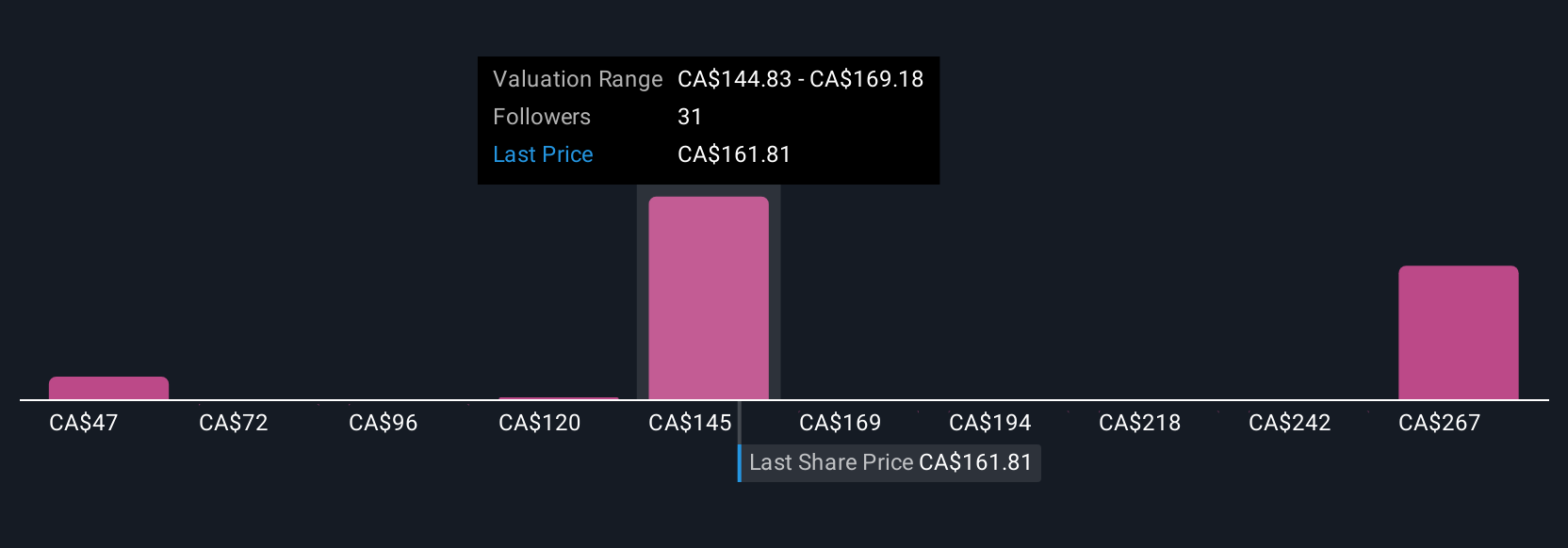

Earlier, we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. In investing, a Narrative is the story or viewpoint that connects your perspective on a company, such as why you see its revenue or margins growing for specific reasons, to your forecast of its future performance and ultimately to your estimate of fair value. With Simply Wall St’s Narratives, available right on the Community page and used by millions worldwide, you can easily see how others interpret Bombardier’s numbers and compare different stories. Narratives make buy or sell decisions more transparent by clearly showing how each story ties the company’s journey to a financial forecast, then to a fair value which is instantly compared against the market price.

They are updated dynamically as news or earnings emerge, giving you an always-current, evidence-backed angle. For example, if you see one Narrative projecting Bombardier’s fair value at CA$200.75, describing durable growth from premium jets and services, but another Narrative places fair value as low as CA$120.05 due to risks from regulatory hurdles or delayed cash inflows, you can choose the story and investment approach that best matches your beliefs, all in one place.

Do you think there's more to the story for Bombardier? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com