Shell (LSE:SHEL): Assessing Valuation After Recent Share Price Gains

See our latest analysis for Shell.

Shell's share price has steadily climbed in recent months, with a 3.3% one-month share price return and 6.5% year-to-date gain reflecting renewed investor interest. Looking at the bigger picture, total shareholder returns stand at a strong 10.6% for the past year and a massive 237% over five years. This suggests momentum is still very much in play despite a few recent bumps.

If Shell's long-term journey caught your attention, why not discover fast growing stocks with high insider ownership for more fast-moving stocks with promising growth and strong insider backing?

With both steady share price gains and future analyst targets implying upside, is Shell currently undervalued and primed for further growth, or is the market already factoring in all its potential, leaving limited room for new buyers?

Most Popular Narrative: 13% Undervalued

Shell’s fair value estimate from the most widely followed narrative lands at £30.92 per share, which is notably higher than the recent close of £26.91. This suggests expectations of future upside. This section lays out what is driving the optimism in that valuation and the assumptions supporting it.

Shell's aggressive high-grading of its portfolio (divestment of non-core assets in Chemicals, Retail, and Renewables, and targeted upstream investments in deepwater and LNG) is redirecting capital to higher-return assets and geographies, underpinning higher operating leverage and future ROIC, and paving the way for more robust and resilient free cash flow.

What’s the secret formula behind this bullish price target? The hidden engine is a blend of calculated portfolio shifts, ambitious margin projections, and head-turning future earnings numbers. Want to see how these bold growth expectations and valuation multiples come together? The full story behind Shell’s perceived value is just a click away.

Result: Fair Value of £30.92 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent underperformance in chemicals or a slower than expected energy transition could quickly challenge Shell’s optimistic outlook and analyst forecasts.

Find out about the key risks to this Shell narrative.

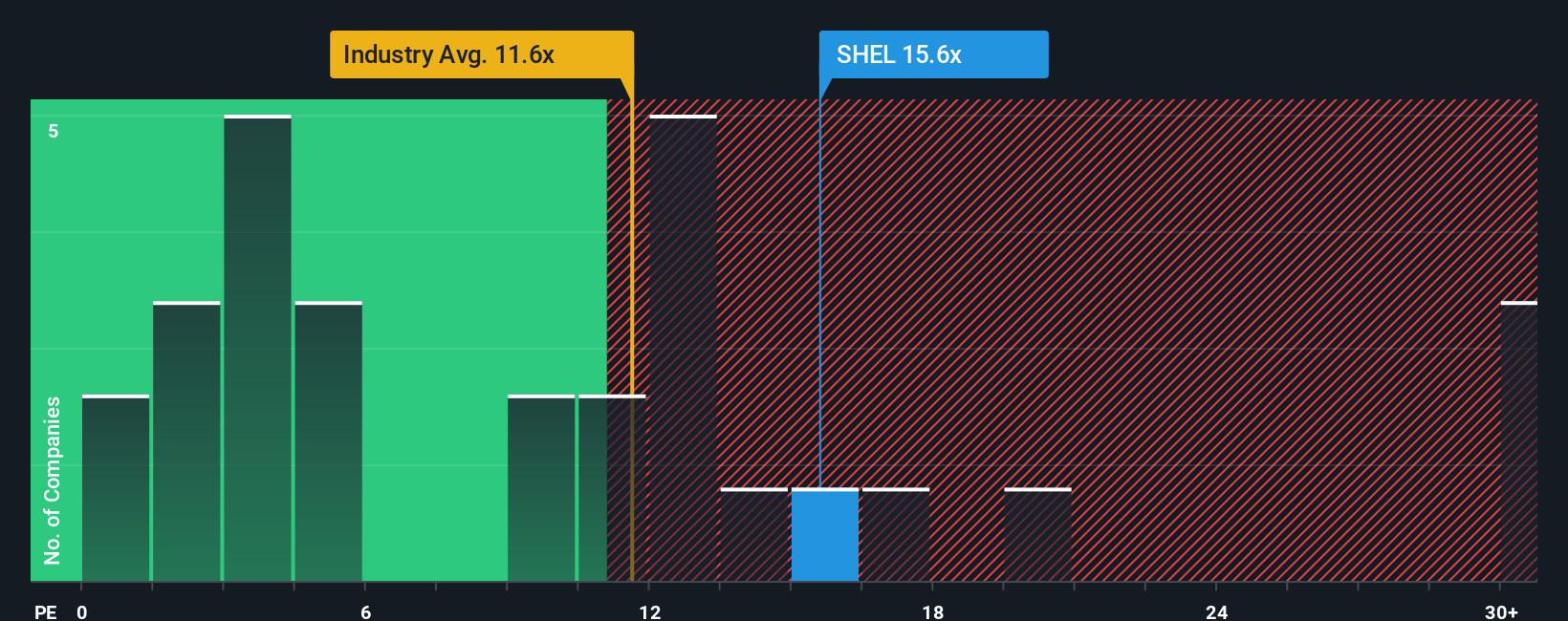

Another View: What Do Earnings Ratios Say?

Looking at Shell’s price-to-earnings ratio of 15.4x, the stock appears more expensive than both the sector average (13.5x) and a typical peer group (15.1x). While this may indicate investor optimism, the fair ratio suggests the market could justify valuations as high as 21.1x given Shell’s fundamentals. Does this premium represent real momentum, or does it hint at valuation risk that could weigh on shares if expectations are not met?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Shell Narrative

If you have a different perspective or want to dig into the numbers on your own terms, building your version of Shell’s story takes just a few minutes. Do it your way.

A great starting point for your Shell research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Stay ahead of the curve and open up fresh opportunities by targeting stocks suited to your strategy. Don’t let standout performers slip away. Take action now:

- Snap up passive income potential by reviewing these 18 dividend stocks with yields > 3%, earning attractive yields above 3%, and strengthen your portfolio’s cash flow.

- Spot emerging trends and leap into innovation with these 24 AI penny stocks, powering breakthroughs in artificial intelligence across multiple industries.

- Secure value-driven opportunities with these 878 undervalued stocks based on cash flows, trading below their cash flow potential for possible long-term upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com