Can Duolingo’s Recent Surge Continue After Strong User Growth in 2025?

Thinking about what to do with your Duolingo shares? Or maybe you are eyeing the stock for the first time and wondering if the recent run-up is just the warmup. Let us dig in together. Over the last month, Duolingo’s stock price has jumped 18.4%, adding to an incredible three-year gain of over 300%. Even in a year where most tech companies have been swept up in volatility, Duolingo has managed a 1.4% year-to-date gain, signaling some underlying resilience that is turning heads among investors.

This momentum comes amid ongoing buzz around the company’s strategic expansion into new language offerings and gamified learning. These are key developments often highlighted by bullish analysts. For many, the surging price raises the classic question: is Duolingo still a buy, or is this another stock flying a little too close to the sun?

To help answer that, we will break down the company’s valuation using six time-tested methods, the same ones the market has relied on for years to spot undervalued gems. By our count, Duolingo scores a 2 out of 6, meaning it is considered undervalued in two key areas. But numbers are only half the story. Before long, I will show you a smarter way to make sense of these valuations and how to think about them beyond the scores alone.

Duolingo scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Duolingo Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future free cash flows and discounting them back to today’s dollars. This approach provides a forward-looking assessment based on how much cash the business is expected to generate, rather than current earnings or book value.

For Duolingo, the latest figures show Free Cash Flow (FCF) at $315 million. Analyst estimates project considerable growth, with FCF climbing to $644 million by the end of 2027. Looking further ahead, projections estimate Duolingo could reach over $1.1 billion in FCF by 2034. It is worth noting that only the first five years are based on direct analyst forecasts, while longer-term numbers are derived from trend extrapolations.

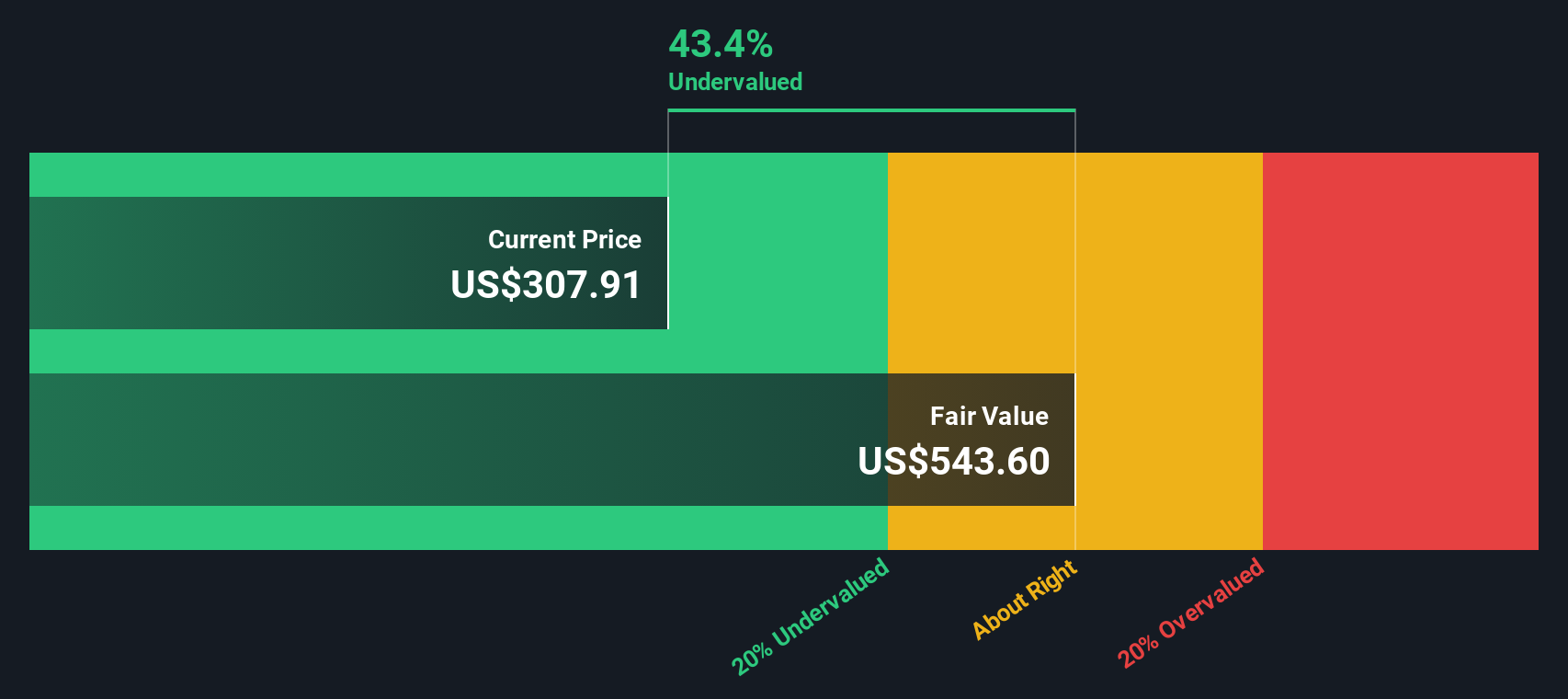

Using this two-stage DCF analysis, Duolingo’s intrinsic value lands at $480 per share. This model indicates the stock is trading at a 31.1% discount to its fair value, making it appear solidly undervalued at current prices.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Duolingo is undervalued by 31.1%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Duolingo Price vs Earnings (PE)

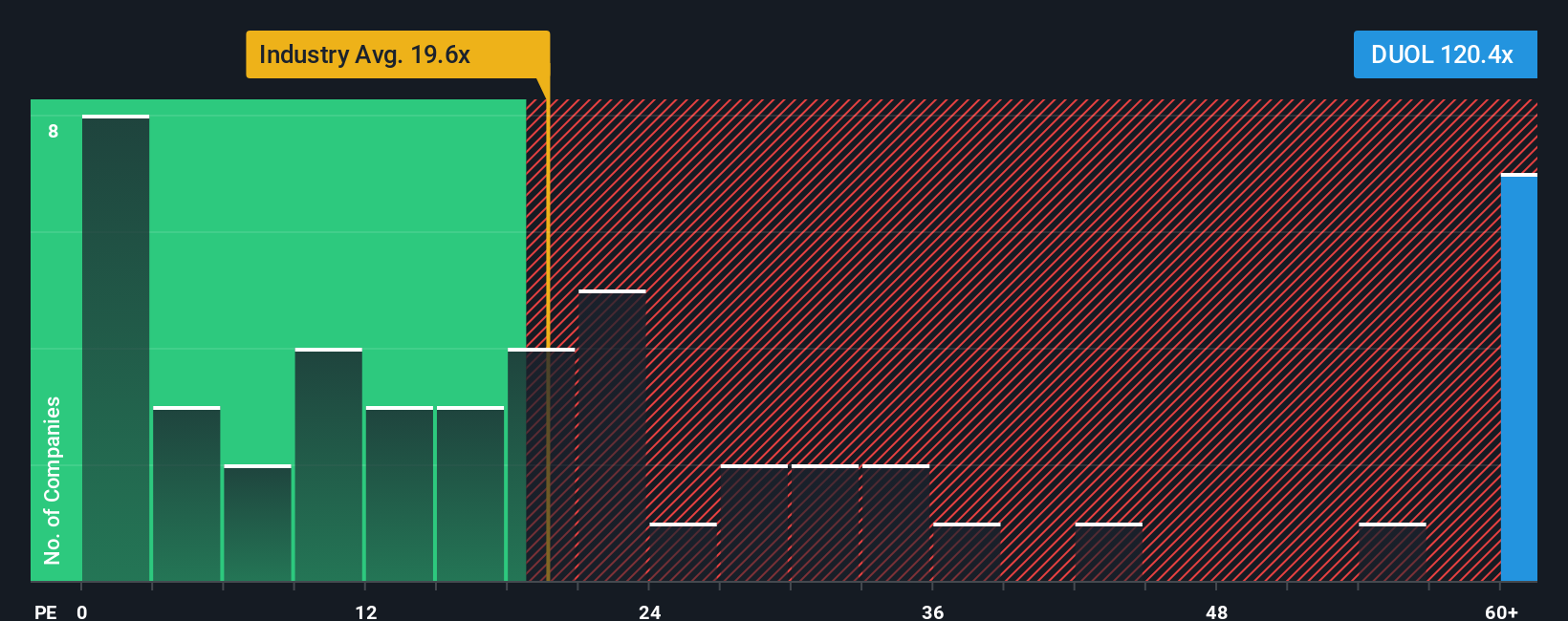

The Price-to-Earnings (PE) ratio is a popular metric for valuing consistently profitable companies like Duolingo, as it directly connects a company’s stock price with its actual earnings power. Investors often use the PE ratio to gauge how much they are paying for each dollar of a company’s earnings. This makes it a go-to measure for those focused on revenue-generating, mature businesses.

However, the “right” PE ratio is not one-size-fits-all. High-growth companies tend to justify higher PE multiples, as investors expect earnings to accelerate rapidly. In contrast, firms facing higher business risk or slower growth usually trade at lower multiples. It is crucial to consider factors like growth expectations, profit stability, and risk when judging if a company’s PE is fair.

Currently, Duolingo trades at a lofty PE of 129.3x. By comparison, the average for its Consumer Services industry is just 17.5x, and the average for its closest peers is 35.1x. Simply Wall St’s proprietary “Fair Ratio” for Duolingo is 38.4x. This Fair Ratio improves on simple benchmarks by blending in company-specific factors such as robust growth prospects, strong profit margins, and unique risks. This approach provides a more tailored standard than a straightforward industry or peer comparison. When we set Duolingo’s actual PE of 129.3x against its Fair Ratio of 38.4x, the gap is wide, implying the stock is notably overvalued based on current earnings multiples.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Duolingo Narrative

Earlier we mentioned there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is more than just numbers; it is a story you create about a company, tying together your perspective on its future with your own expectations for growth, profit margins and risk. Narratives connect the dots from a company’s story to a financial forecast and then to a fair value, providing a powerful framework to make smarter, more personalized investment decisions.

On Simply Wall St’s Community page, Narratives are accessible to all investors and updated automatically as new news or earnings come in. This accessible tool, used by millions of investors, helps you clearly compare the fair value you believe in with the current price, so you know when your story suggests a buy, a sell, or a wait.

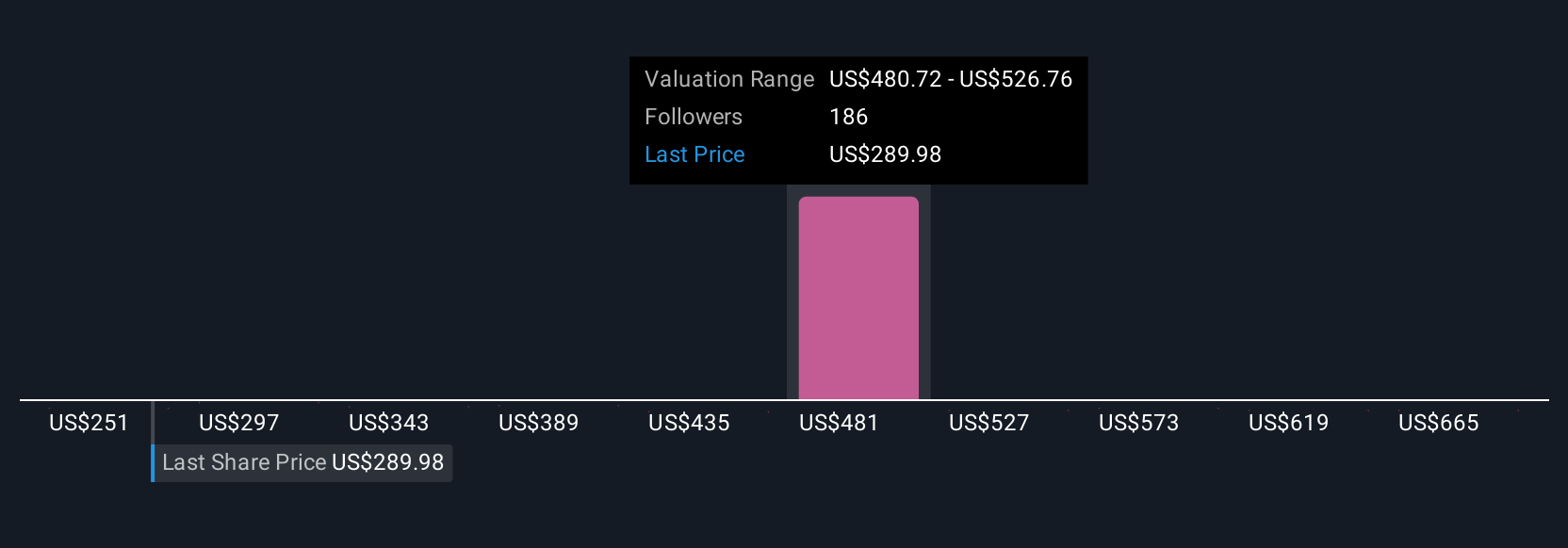

For example, some Duolingo investors will build optimistic Narratives focused on international expansion, AI-driven personalization, and new features, leading to a fair value as high as $600 per share. Others, concerned about slowing growth or competition, may take a different view, arriving at a fair value as low as $239. This range comes directly from real, current Narratives, showing how your own story can (and should!) guide your investing decisions.

Do you think there's more to the story for Duolingo? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com