Audinate Group (ASX:AD8) Valuation: Fresh Look Following Major Shareholder Exit and New Incentive Scheme

Audinate Group (ASX:AD8) has caught investor attention following news that Fisher Funds Management Limited is no longer a substantial holder. This development comes alongside the company’s recent issuance and quotation of new securities under its employee incentive scheme.

See our latest analysis for Audinate Group.

After a sharp climb in the past month, with a 1-month share price return of 38.5%, Audinate Group’s recent announcements around incentive schemes and changing major shareholders have reignited market curiosity. Despite this momentum, its one-year total shareholder return stands at -33.2%. This highlights that the road has not been smooth, but there is renewed optimism building as the company takes strategic steps to strengthen its position.

If you’re watching these shifts in leadership and sentiment, consider using this moment to broaden your perspective and discover fast growing stocks with high insider ownership.

With the share price rebounding sharply and long-term returns still lagging, the real question is whether Audinate Group now offers value for savvy investors or if the recent gains already reflect the company’s future prospects.

Most Popular Narrative: 23.9% Undervalued

The prevailing narrative sees Audinate Group’s fair value nearly 24% above its recent A$6.44 close, highlighting a striking mismatch between consensus expectations and current market pricing. With ever-changing cloud and software trends shaping the business outlook, investors are paying close attention to what fuels this gap.

Management is investing heavily in the rollout and scaling of new software and cloud-based products (Dante Director, Iris), which target the growing demand for integrated audio, video, and control in modern AV systems (including remote and hybrid workflows). This unlocks higher-margin, recurring SaaS revenue streams and positions the company for sustained gross margin expansion and more predictable earnings.

Want to know why this outlook justifies a much loftier price? One set of projections in this narrative will surprise you, especially the bold calls for future profit margins and potential profit multiples rarely seen outside the fastest-growing tech platforms. Intrigued? Uncover the drivers behind this valuation for Audinate Group.

Result: Fair Value of $8.46 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, looming risks such as slowing AV industry growth and rising operating costs could challenge the optimistic outlook and hinder Audinate’s recovery.

Find out about the key risks to this Audinate Group narrative.

Another View: What Do Multiples Say?

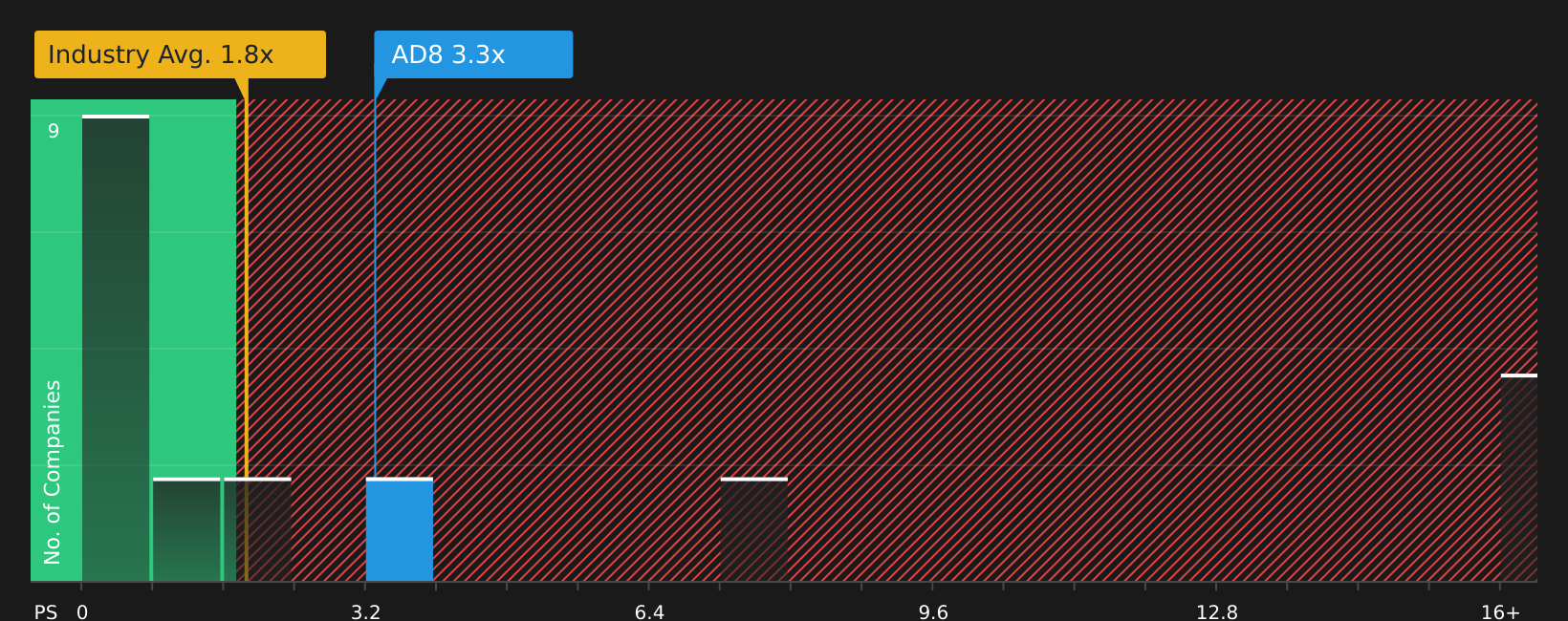

Looking at Audinate Group through market multiples, the price-to-sales ratio stands at 8.7x. This is well above both its estimated fair ratio of 5.9x and the industry average of 1.8x. However, it remains lower than peer averages at 22.8x. These figures suggest much of the optimism may already be priced in, making the valuation story less clear-cut for investors seeking under-the-radar opportunities. Could the market be getting ahead of itself, or does Audinate have room to grow into this premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Audinate Group Narrative

If you have a different perspective or prefer diving into the data on your own terms, it only takes a few minutes to shape your personal view. Do it your way.

A great starting point for your Audinate Group research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let opportunity pass you by. Use the Simply Wall Street Screener to put smart investing possibilities on your radar and take the lead in building your portfolio.

- Uncover stocks offering strong yields by checking out these 20 dividend stocks with yields > 3% for stable income potential above 3%.

- Capture value opportunities by seeking these 873 undervalued stocks based on cash flows with real promise based on solid cash flow fundamentals.

- Tap into the next wave of artificial intelligence growth with these 24 AI penny stocks that are driving innovation in the AI sector.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com