Is ADM Fairly Priced After Nutrition Segment Growth and a 25% Rebound in 2025?

If you’re looking at Archer-Daniels-Midland and wondering whether it’s the right time to buy, sell, or simply hold steady, you’re definitely not alone. Investors and analysts alike have been watching this stock’s latest moves with keen interest, especially as broader market shifts are reshaping expectations for food industry giants. Over the past year, Archer-Daniels-Midland has seen a strong rebound, returning 25.2% so far this year and 11.6% over the last twelve months. Shorter-term numbers, like the 2.6% uptick in just the past week, suggest renewed optimism, even after a longer-term dip of nearly 22% over three years. The climbing price may reflect shifting risk perceptions as global commodity trends and economic uncertainty prompt investors to rethink where true value sits in the market.

So, does the current rally mean Archer-Daniels-Midland is undervalued, or are we looking at a stock that is already caught up to its fundamentals? When we run the numbers, the company actually scores a 1 out of 6 on leading valuation checks, hinting that only one major metric flags ADM as undervalued right now. But valuation is more than just a checklist, and how you interpret these numbers matters. In the sections ahead, I’ll break down the different approaches to measuring a stock’s value and share a perspective at the end that goes beyond the standard methods, giving you an even clearer way to think about ADM’s true worth.

Archer-Daniels-Midland scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Archer-Daniels-Midland Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a commonly used tool to estimate a company's intrinsic value by projecting its future cash flows and discounting them back to the present. This approach looks at what Archer-Daniels-Midland (ADM) is expected to produce in terms of cash, both in the near and longer term. It calculates what that future stream is worth in today's dollars.

For ADM, current Free Cash Flow stands at $4.21 Billion. Analyst projections provide specific figures for the next several years, with free cash flows estimated at $1.86 Billion in 2026 and $2.25 Billion in 2027. Beyond that, forecasts are extrapolated out to 2035, suggesting some fluctuation but not dramatic growth over the coming decade.

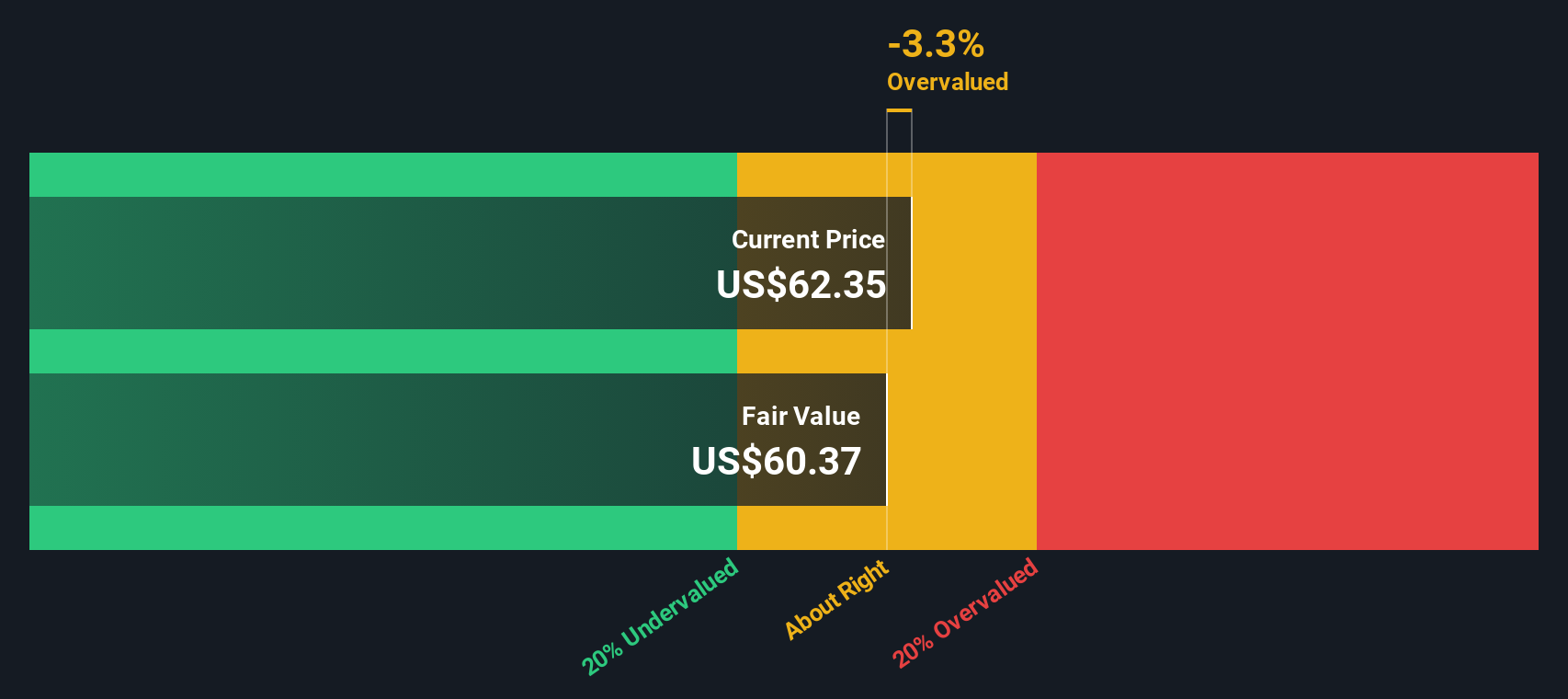

Based on these projections and using a 2 Stage Free Cash Flow to Equity model, the DCF calculation results in an intrinsic value of $64.53 per share. The current share price shows an implied discount of 2.5%, which means ADM trades at a level that is just slightly below its projected fair value according to this model.

This suggests that, at present, Archer-Daniels-Midland is roughly in line with what its long-term cash flows would justify.

Result: ABOUT RIGHT

Simply Wall St performs a valuation analysis on every stock in the world every day (check out Archer-Daniels-Midland's valuation analysis). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes.

Approach 2: Archer-Daniels-Midland Price vs Earnings

For established and profitable companies like Archer-Daniels-Midland, the Price-to-Earnings (PE) ratio is a widely used indicator to gauge whether a stock is trading at a reasonable valuation. The PE ratio measures how much investors are willing to pay for each dollar of a company's earnings. This makes it a straightforward way to compare companies within the same industry or against their own history.

Growth expectations and perceived risks influence what is considered a "fair" PE ratio. Companies with higher expected earnings growth or lower risk typically trade at higher PE multiples, as investors are willing to pay more today for anticipated higher profits in the future. Conversely, companies facing uncertainty or slower growth often see lower ratios.

Currently, Archer-Daniels-Midland trades at a PE ratio of 27.5x. This is well above the food industry average of 18x and also above the average of its peers at 20.9x. On the surface, this suggests ADM's stock price is relatively expensive compared to industry norms.

However, looking closer, Simply Wall St’s proprietary Fair Ratio for ADM is 22.5x. This metric is designed to go beyond the basic benchmarks by taking into account the company’s earnings growth, profitability, industry fundamentals, market capitalization, and specific business risks. Relying on the Fair Ratio offers a more nuanced and accurate view than simply comparing to broad averages, as it recognizes what makes ADM unique.

With ADM’s PE at 27.5x and the Fair Ratio at 22.5x, the stock appears slightly overvalued, but not dramatically so.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Archer-Daniels-Midland Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Rather than just focusing on ratios or price targets, a Narrative lets you build a story around Archer-Daniels-Midland by bringing together your outlook on its future revenue, profits, and margins, then connecting those details directly to your own fair value estimate. Narratives link the company's evolving story to real numbers and make your investment thesis more meaningful and actionable.

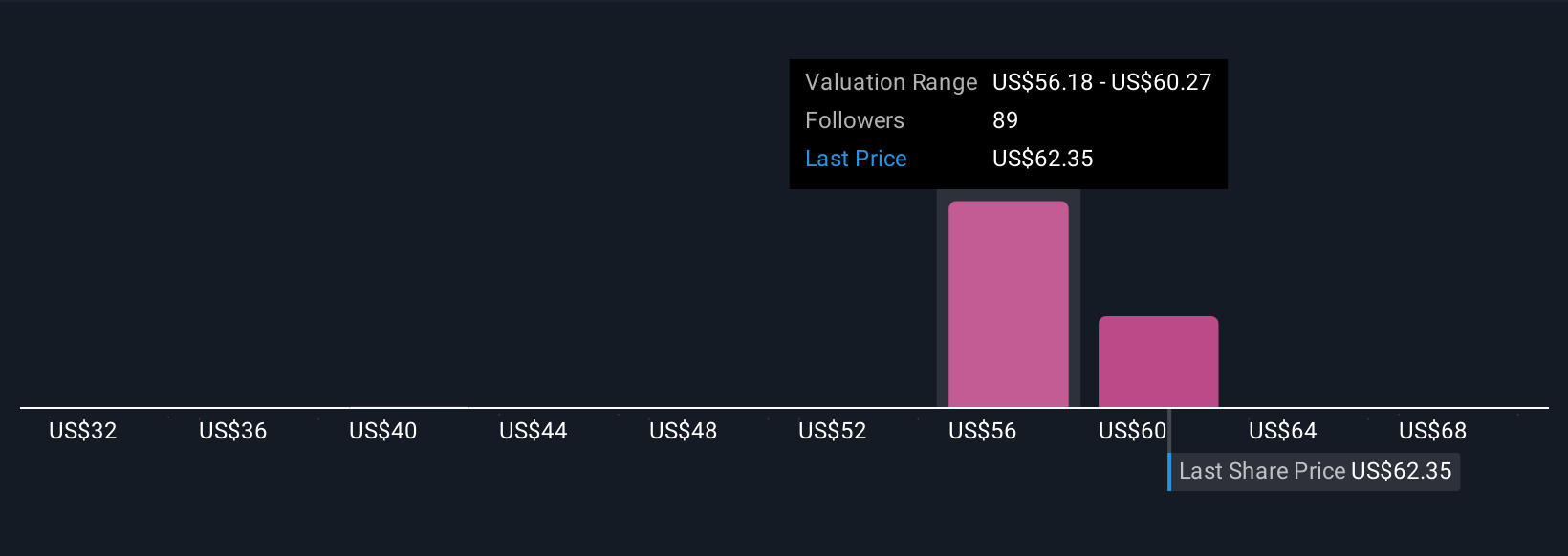

On Simply Wall St’s Community page, investors use Narratives to write and update their perspectives using intuitive tools that millions rely on worldwide. This hands-on approach helps you see exactly why others choose to buy, hold, or sell by comparing their estimated fair values to today’s price and observing how these outlooks change dynamically as new news or earnings reports are released. For example, some investors think government policy support and facility upgrades could unlock upside and assign Archer-Daniels-Midland a value as high as $70, while others remain cautious and see only $54 as fair. Ultimately, Narratives empower you to form your own opinion, sense-check consensus targets, and invest with more clarity and conviction.

Example: One Narrative might focus on recent biofuel subsidies and Nutrition segment growth, favoring a higher target value. Another might weigh ongoing regulatory risks or commodity price pressure, leading to a lower fair value. Your story, your numbers, your decision.

Do you think there's more to the story for Archer-Daniels-Midland? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com