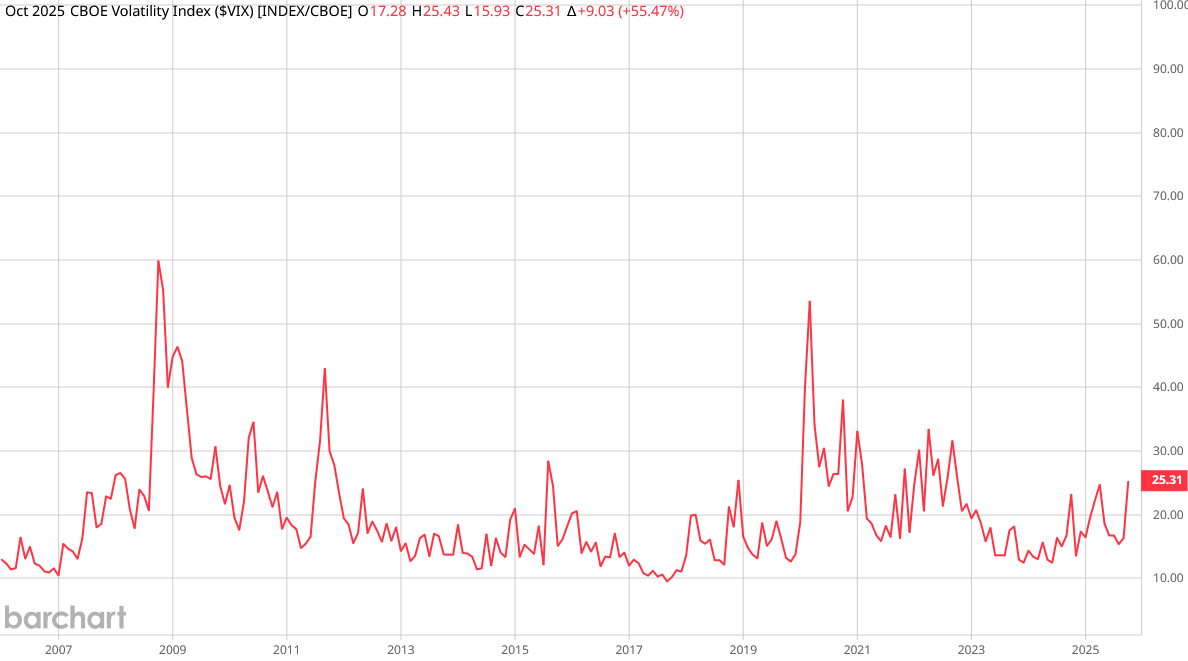

Interpreting the VIX and Practical Uses

The VIX or CBOE Volatility Index ($VIX) was launched in 2003 and is known as the “Fear Index” because it projects the potential range of movement or volatility in the U.S. equity markets (specifically the S&P 500) above/below its current level, in the immediate future.

The VIX ($VIX) measures the implied volatility of S&P 500 ($SPX) put and call options over the next 30 days. Essentially, by analyzing the price of these options, the VIX calculates the level of volatility that investors are factoring into their pricing.

When implied volatility is high, the VIX level is high, and the range of likely values of the S&P 500 ($SPX) is broad. When implied volatility is low, the VIX level is low, and the range of potential outcomes is narrow.

How is the VIX Measured?

The VIX is reported as an annualized number, which can be interpreted as the expected magnitude of a one-standard-deviation move over the next year.

The Empirical Rule of statistics states that 68% of normally distributed data falls within one standard deviation of the mean. Therefore, the VIX level represents the percentage range, plus or minus, that the market is expected to move over the next year with a 68% confidence level.

Example: Interpreting the VIX in Real Time

For example, looking at the VIX today while it trades at a level of 16.0, it suggests a 68% probability that the S&P 500 will experience a +/-16% move over the next year.

To understand the expected monthly volatility, the VIX can be de-annualized by dividing its value by the square root of 12 (the number of months in a year). Using the same example, a VIX level of 16.0 suggests a monthly implied volatility of +/-4.6% for the S&P 500 ($SPX).

Therefore, the VIX index’s level provides a quick indication of market sentiment:

- A low VIX level (0-15) typically suggests optimism and low expected volatility.

- A moderate level (15-20) indicates a normal market environment.

- Levels considered high (above 25) suggest growing concern or turbulence in the market.

Practical Uses of the VIX

Some general use cases of the VIX include:

- Diversifying/Hedging a Portfolio – Since the VIX has negative correlation with the S&P 500 ($SPX), the more the S&P 500 ($SPX) falls, the more the VIX rises. Therefore, investors who have a long position in equities could use the VIX to hedge their position if they speculate that there will be some weakness in the market. They could do this by taking a long position on the VIX with options or futures or potentially use a VIX ETF.

Trading/Speculating for Profits – Beyond hedging, some traders use the VIX to speculate on market cycles and a reversion to the mean. For example, following a period of weakness in the market and high volatility, an investor will sell VIX linked products with the expectation that volatility will moderate in the near future. Or following a period of low volatility will purchase VIX linked products in anticipation of future periods of weakness with the expectation that volatility will increase in the near future.

Should You Use the VIX to Help You Manage Your Money?

While the VIX has been shown to have predictive power in forecasting short-term equity volatility, it should not significantly influence how long-term investors manage their money. Short-term traders pay close attention to the VIX, but for long-term investors, month-to-month and even year-to-year volatility is largely random. The focus for long-term investors should be on their portfolio’s long-term returns rather than short-term market fluctuations – specifically the quality companies that they chose to build their portfolio with. Want research-backed guidance on building a stronger portfolio? Become a KeyStone client today and access our expert stock recommendations, analysis, and long-term strategies.