Has HKEX Rallied Too Far After Latest Mainland Listing Rule Change?

If you're watching Hong Kong Exchanges and Clearing right now, you're definitely not alone. This stock is on the radar of investors looking for both stability and a shot at long-term growth, especially after its recent rollercoaster performance. Just glance at the numbers: while the last week and month saw some red, with dips of -7.1% and -6.1% respectively, the stock has soared an impressive 47.9% year-to-date and is up 81.2% over the past three years. Even over five years, it has delivered a healthy 30.7% gain. That is a track record that is hard to ignore, especially with recent market dynamics in Hong Kong shaking things up for major financial institutions.

Despite the volatility, some analysts are buzzing about future reforms and renewed global capital flows into Hong Kong, hinting at real upside. But with all this momentum, what about value? Our latest assessment runs the stock through six key valuation checks, including major measures like earnings, sales, and assets. The result is a value score of 0 out of 6. In plain terms, the company is considered overvalued on every front by our standard metrics.

But does that tell the whole story? In the next sections, we will break down what each valuation method is saying about Hong Kong Exchanges and Clearing. Then we will dig into a smarter, more nuanced way to understand what the stock is really worth.

Hong Kong Exchanges and Clearing scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

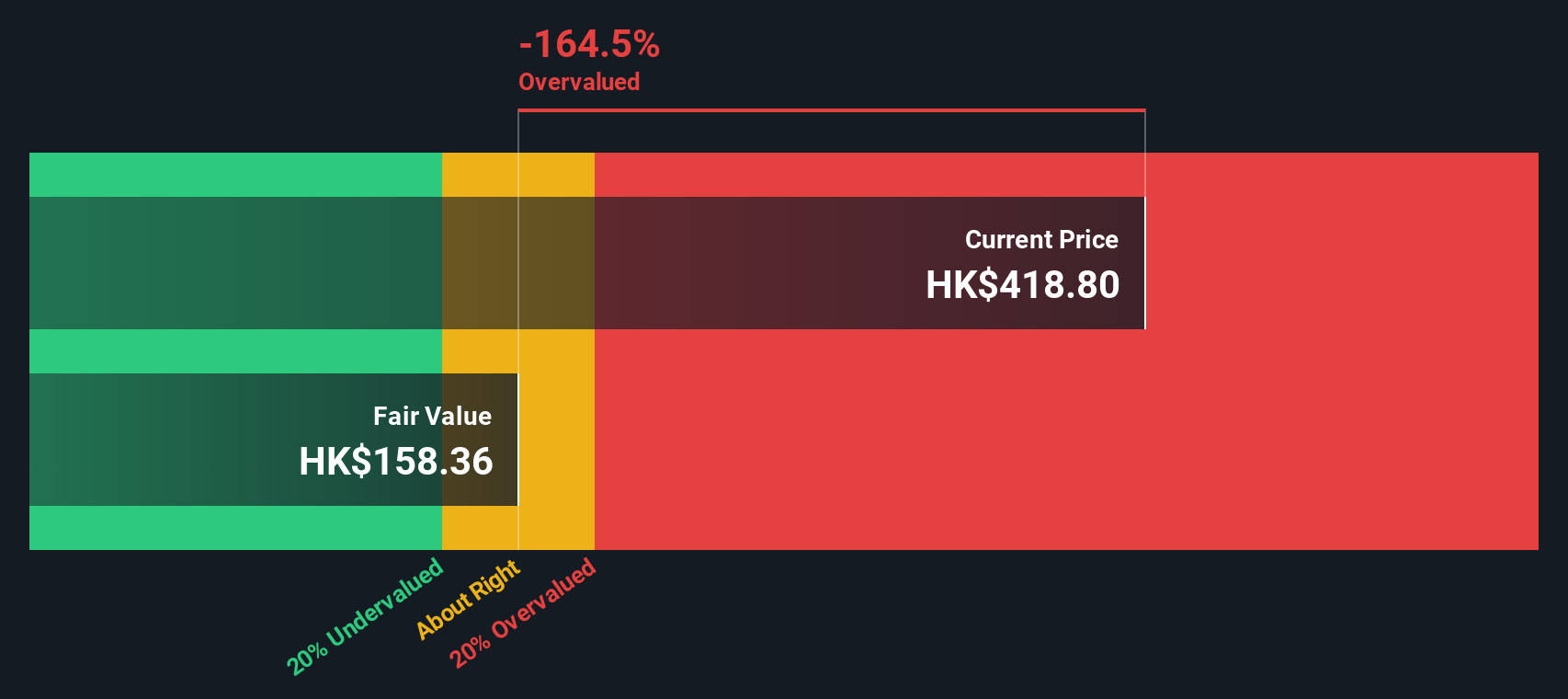

Approach 1: Hong Kong Exchanges and Clearing Excess Returns Analysis

The Excess Returns model is designed to evaluate how effectively a company turns shareholder equity into profits, after accounting for the basic cost of that equity. For Hong Kong Exchanges and Clearing, this approach highlights not just the earnings but also how much value is being created above what investors could have expected from a low-risk alternative.

Let's look at the details. The latest book value for the company stands at HK$45.03 per share, while the long-term stable earnings per share are estimated at HK$13.79, based on future Return on Equity assessments from 18 analysts. The calculated cost of equity is HK$3.76, meaning the company is generating an excess return of HK$10.03 per share. The average future Return on Equity is a robust 29.94%. Recent analyst projections suggest a stable book value of HK$46.06 per share, underlining confidence in sustained underlying asset strength.

According to this model, the stock's intrinsic value is significantly less than its current trading price, with an implied 85.3% overvaluation. The Excess Returns approach signals that, despite strong profitability metrics, the market price has run well ahead of the company’s true value.

Result: OVERVALUED

Our Excess Returns analysis suggests Hong Kong Exchanges and Clearing may be overvalued by 85.3%. Find undervalued stocks or create your own screener to find better value opportunities.

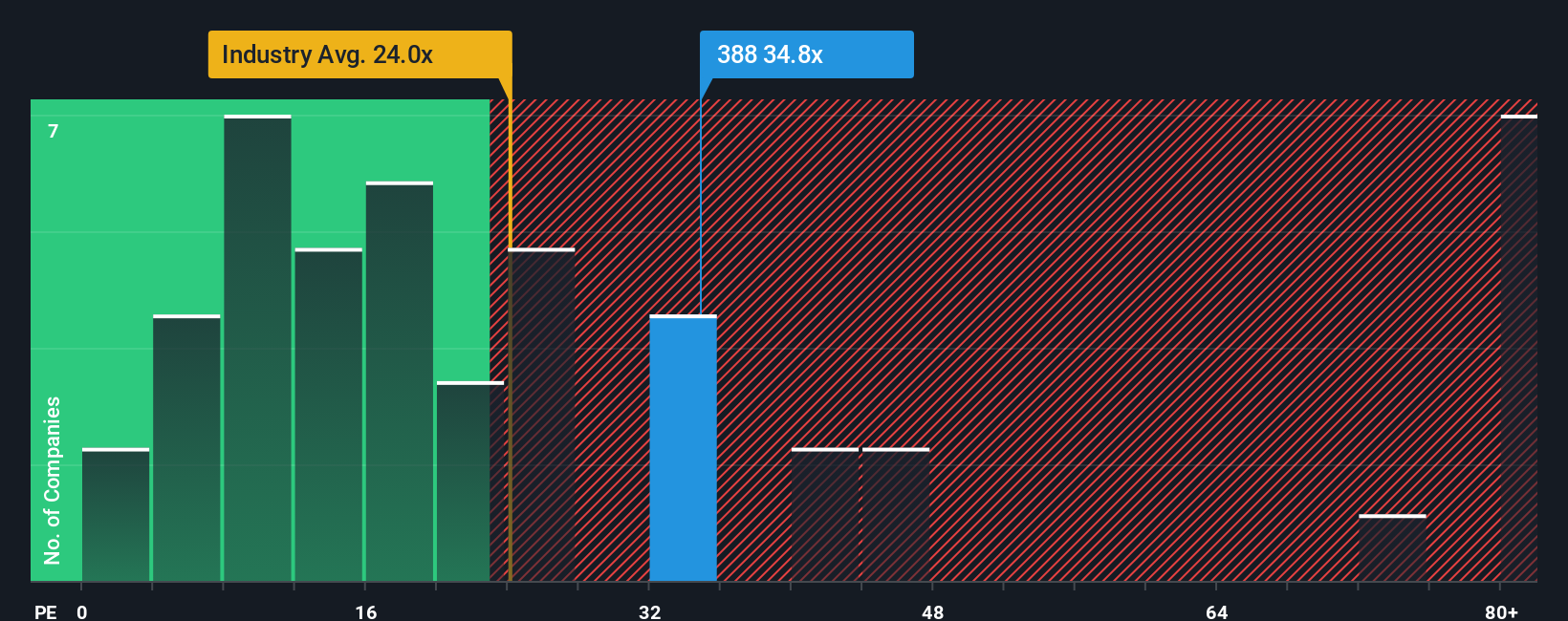

Approach 2: Hong Kong Exchanges and Clearing Price vs Earnings

For profitable companies like Hong Kong Exchanges and Clearing, the Price-to-Earnings (PE) ratio is an especially useful valuation metric. It helps investors quickly gauge how much they are paying for each dollar of a company’s earnings, making it easier to weigh value for money in the context of expected growth and risk.

In general, a higher PE ratio is justified for companies with strong earnings growth and lower perceived risk, as investors are willing to pay a premium for future potential. Conversely, higher risk or weaker growth prospects typically warrant a lower PE multiple. This context is crucial, as what seems expensive in one industry may be standard in another, and strong fundamentals can shift what is considered “fair.”

Currently, Hong Kong Exchanges and Clearing is trading on a PE ratio of 34.7x. That is well above the industry average for Capital Markets at 23.9x, and substantially higher than the peer average of 14.6x. However, instead of comparing to these blunt yardsticks, the Simply Wall St Fair Ratio is designed to be more precise. It is proprietary and custom-fitted, factoring in the company’s actual earnings growth, risks, profit margin, industry trends, and market capitalization. For Hong Kong Exchanges and Clearing, the Fair Ratio is 15.7x, reflecting what investors should reasonably pay for its underlying qualities in today’s market. This Fair Ratio is a sharper tool, ensuring comparisons are meaningful and based on the company’s real prospects, rather than broad averages.

Since the stock’s current PE of 34.7x is markedly above the Fair Ratio of 15.7x, it strongly suggests the shares are overvalued on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hong Kong Exchanges and Clearing Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your own story and outlook about a company, connecting your perspective on where Hong Kong Exchanges and Clearing is heading to specific assumptions about its future revenue, earnings, and margins, and ultimately, what you believe the fair value should be. Narratives bridge the gap between the numbers and the real-world reasons behind them, linking company stories and catalysts to a clear financial forecast and fair value estimate.

On Simply Wall St's Community page, millions of investors use Narratives as an easy and accessible tool to build or follow these stories. Narratives update automatically as new news or earnings are released, so your view stays fresh and relevant. By comparing your Narrative-based fair value with the current share price, you can quickly decide if it might be time to buy, sell, or hold.

For example, some investors believe Hong Kong Exchanges and Clearing deserves a price as high as HK$542, driven by the region's economic momentum and expansion into new financial products. Others take a more cautious approach with targets around HK$340, reflecting concerns over competition and regulatory risks. Narratives empower you to decide what you think is most probable and invest accordingly.

Do you think there's more to the story for Hong Kong Exchanges and Clearing? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com