Baytex Energy (TSX:BTE): Is the Stock Undervalued After Recent Momentum?

See our latest analysis for Baytex Energy.

The strong 25% share price return over the past three months signals that momentum is building for Baytex Energy, even as its 1-year total shareholder return remains in the red at -15.5%. While there have not been any headline-making events lately, this recent rally suggests that the market may be reassessing Baytex’s growth story and risk profile in light of past underperformance.

If you’re curious to see what other fast-moving opportunities the market holds right now, why not explore fast growing stocks with high insider ownership?

With momentum picking up but long-term returns still lagging, the next question is whether Baytex Energy’s recent surge means the stock is undervalued or if all the potential is already factored into the current price. This raises the issue of whether there is a true buying opportunity or not.

Most Popular Narrative: 16.7% Undervalued

With the prevailing narrative assigning Baytex Energy a fair value of CA$3.95, the stock’s latest close of CA$3.29 still leaves notable upside, giving investors plenty to debate about the story behind these numbers.

The company expects to generate $400 million of free cash flow in 2025 at USD 70 WTI, indicating a robust generation of excess cash that could be utilized for further debt reduction and shareholder returns, potentially improving earnings and financial stability.

Interested in what supports this growth outlook? The path to this valuation is shaped by aggressive corporate targets and an earnings roadmap that many consider ambitious. Curious about which financial levers truly distinguish Baytex? Only a thorough analysis of the narrative reveals the full picture.

Result: Fair Value of $3.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, key risks remain, such as a drop in oil prices or shifting U.S. tariffs. Either of these factors could derail Baytex's current growth assumptions.

Find out about the key risks to this Baytex Energy narrative.

Another View: Looking at Earnings Multiples

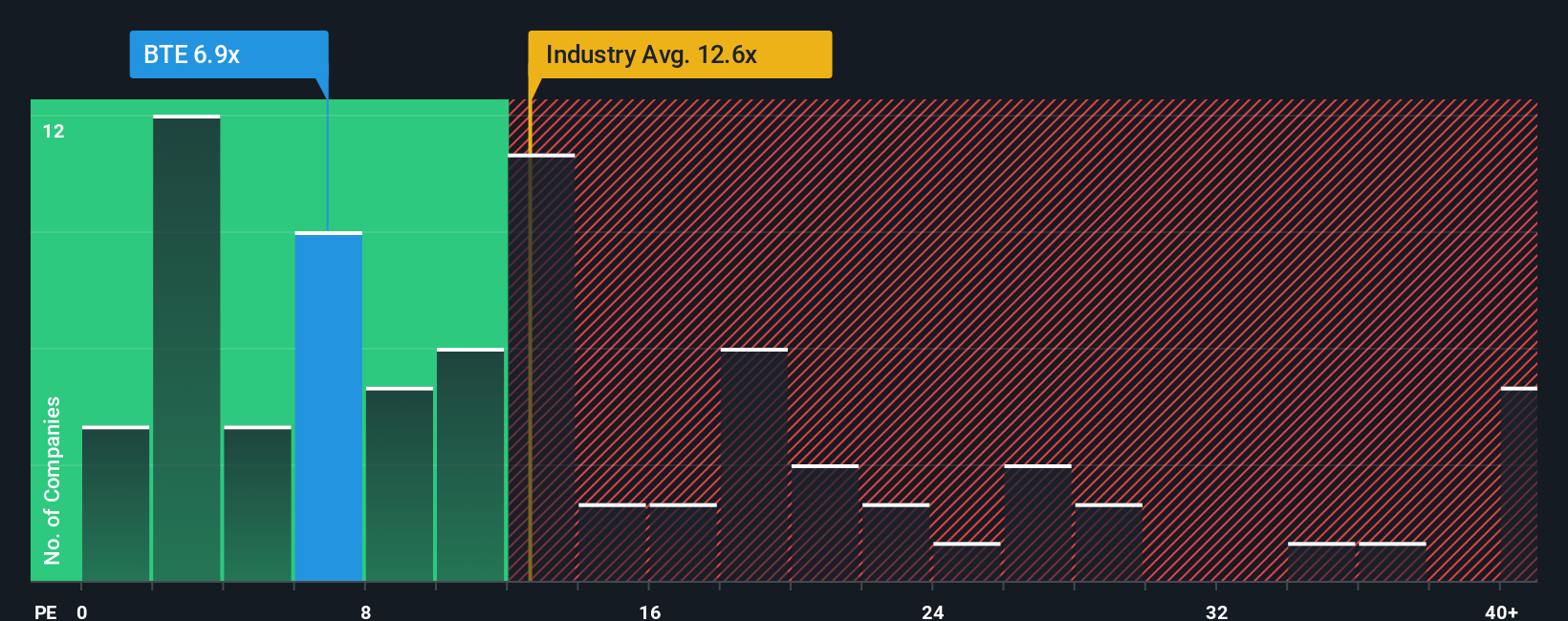

While the analyst consensus points to Baytex being undervalued, our comparison with industry benchmarks reveals a more nuanced picture. Baytex’s price-to-earnings ratio stands at 6.9x, which is well below the Canadian market average of 16.7x and the oil and gas industry’s 12.2x. This suggests value. However, the ratio remains above its fair ratio of 4.5x, indicating that the stock might not be as cheap as it first appears. Does this gap hint at hidden risks or a real opportunity?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Baytex Energy Narrative

If you have a different perspective or want to take a hands-on approach, you can dig into the numbers and shape your own investment story in just a few minutes. Do it your way.

A great starting point for your Baytex Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Opportunities?

Don’t let potential winners slip past you. The market is full of bold possibilities and untapped strategies, perfectly matched to your interests and ambitions.

- Tap into rapid sector growth by checking out these 24 AI penny stocks that are capitalizing on artificial intelligence trends and unlocking new levels of performance.

- Maximize value in your portfolio by seeking these 875 undervalued stocks based on cash flows based on their long-term cash flow fundamentals, before the broader market catches on.

- Accelerate your income strategy with these 18 dividend stocks with yields > 3% that consistently provide attractive yields and a track record of rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com