How Investors May Respond To WiseTech Global (ASX:WTC) Trading Below Historical Valuations Amid Renewed Interest

- WiseTech Global, a leading developer of cloud-based logistics software, has recently seen its shares trade below their historical price-to-sales ratio, following a significant price decline earlier this year despite the company's robust historical revenue performance.

- This disconnect between the share price and WiseTech’s track record has sparked renewed interest among investors, with some viewing the company as potentially undervalued given its established market presence and product portfolio.

- With WiseTech Global trading at a lower valuation relative to history, we'll assess what this could mean for its future investment outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

WiseTech Global Investment Narrative Recap

To be a WiseTech Global shareholder, you need to believe in the ongoing transformation of global supply chains and WiseTech’s ability to harness technology for long-term logistics industry growth. The recent fall in the company’s share price and price-to-sales ratio has caught attention, but the core catalysts, delivery of the E2open integration and successful rollout of the transaction-based CargoWise model, remain in place, while risks from integration complexity and slowing organic growth still require close monitoring. For now, the recent price move does not appear to materially shift these key drivers. Among recent announcements, the confirmation of discussions to acquire E2open Parent Holdings, Inc. (May 2025) stands out. This acquisition marks a significant expansion of WiseTech’s product reach and addresses one of the largest short-term catalysts: delivering operational and financial synergies from this integration that could define WiseTech’s longer-term earnings footprint. By contrast, one risk investors should be mindful of is the complexity and cost pressure associated with integrating a business as large as E2open...

Read the full narrative on WiseTech Global (it's free!)

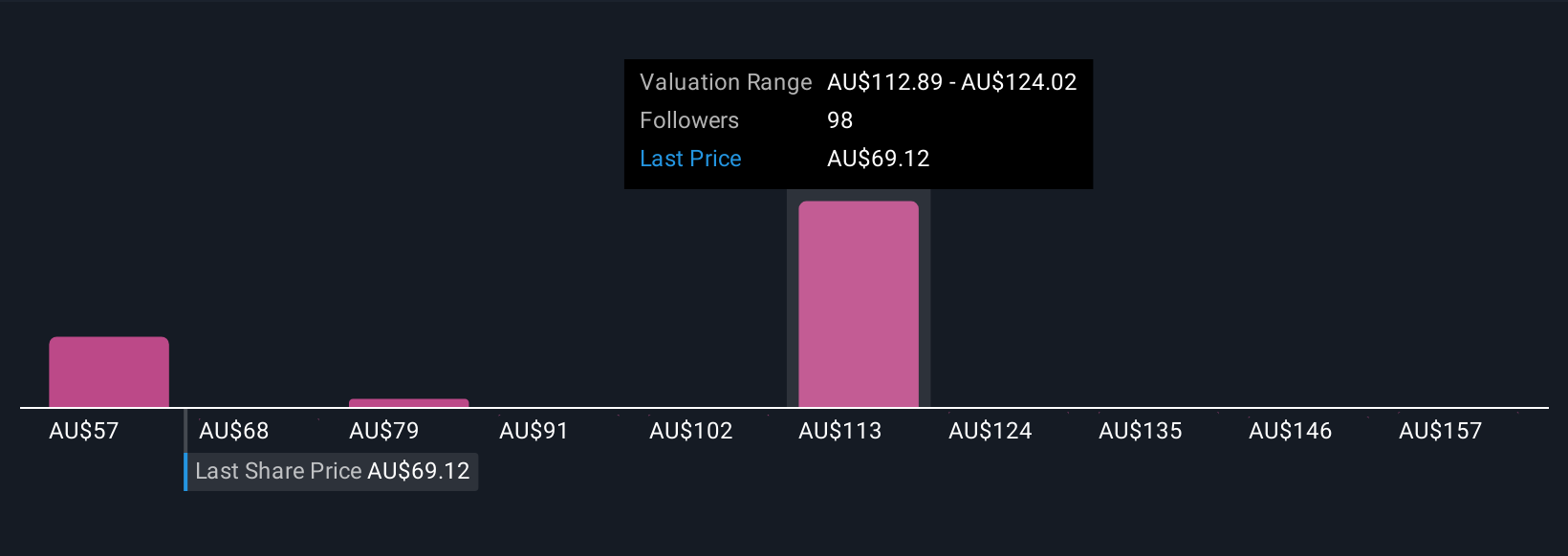

WiseTech Global's narrative projects $2.0 billion in revenue and $486.9 million in earnings by 2028. This requires 35.8% yearly revenue growth and a $286.2 million earnings increase from $200.7 million today.

Uncover how WiseTech Global's forecasts yield a A$123.28 fair value, a 47% upside to its current price.

Exploring Other Perspectives

Nineteen fair value estimates from the Simply Wall St Community range from A$52.43 up to A$339.13, showing how varied investor outlooks can be. While some anticipate significant uplift from the E2open deal, others continue to flag that execution risks could weigh heavily on WiseTech’s performance, reminding you to consider several viewpoints before forming your own conclusion.

Explore 19 other fair value estimates on WiseTech Global - why the stock might be worth 37% less than the current price!

Build Your Own WiseTech Global Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your WiseTech Global research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free WiseTech Global research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate WiseTech Global's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com