How Rising Loan Losses at M&T Bank (MTB) Have Shifted Its Credit Quality Investment Narrative

- M&T Bank Corporation recently reported that net charge-offs reached US$146 million for the third quarter ended September 30, 2025, up from US$108 million in the previous quarter and US$120 million in the same period last year.

- This increase in loan losses comes just ahead of M&T Bank's scheduled earnings report, drawing investor attention to the bank's credit quality trends.

- We'll explore how the rise in net charge-offs could influence the outlook for M&T Bank's future earnings and capital management plans.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

M&T Bank Investment Narrative Recap

To be a shareholder in M&T Bank, you need to believe in its focus on capital strength, efficient balance sheet management, and steady fee income growth as core drivers of value. While the recent uptick in net charge-offs to US$146 million is drawing scrutiny ahead of the earnings report, it does not appear to materially shift the most important short-term catalyst: maintaining robust profitability and stable capital levels. However, credit quality remains a visible risk, and any signs of deterioration could shape market sentiment in the near term.

Among recent company announcements, the board’s 11% increase in the quarterly dividend to US$1.50 per share is most relevant. This move highlights management’s ongoing confidence in M&T’s underlying earnings power and capital position, key factors that could counterbalance concerns about rising credit losses. Dividends and capital returns remain central themes for shareholders seeking income and reassurance amidst recent headlines.

But investors should be aware, in contrast to these positives, that higher loan losses can heighten focus on underlying credit risk and its potential impact on future returns...

Read the full narrative on M&T Bank (it's free!)

M&T Bank's narrative projects $10.2 billion revenue and $2.6 billion earnings by 2028. This requires 4.5% yearly revenue growth and a $0.1 billion earnings increase from $2.5 billion.

Uncover how M&T Bank's forecasts yield a $221.17 fair value, a 20% upside to its current price.

Exploring Other Perspectives

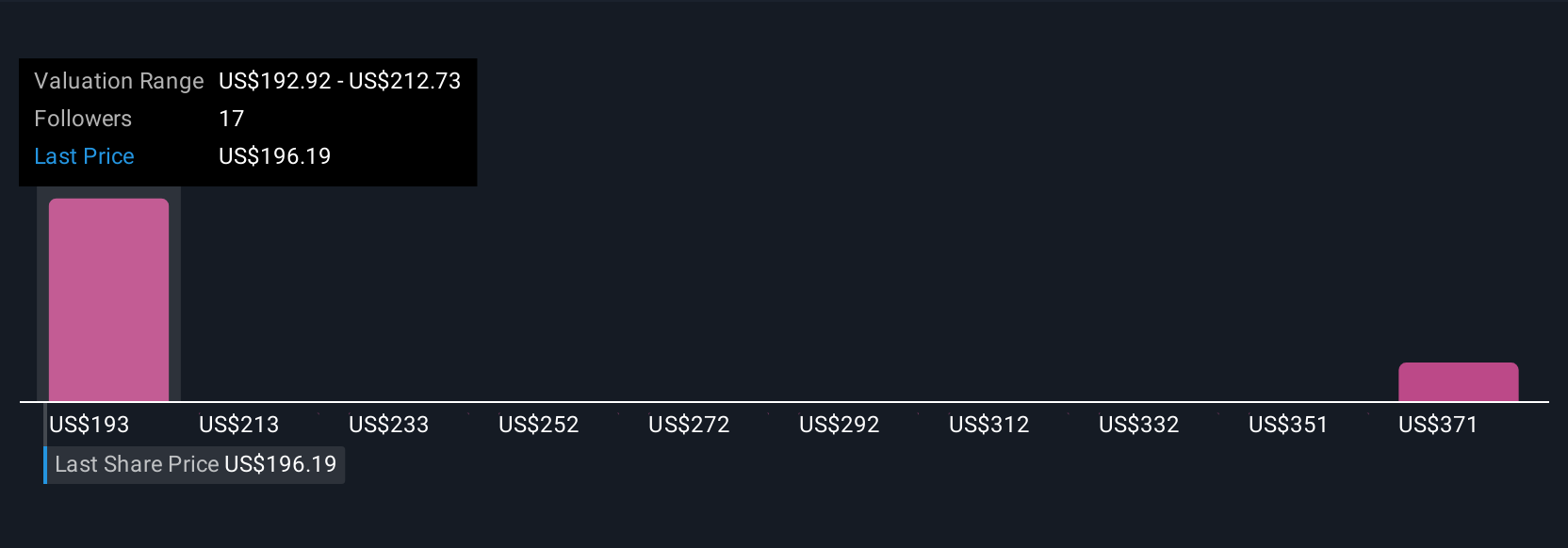

Simply Wall St Community members provided five fair value estimates for M&T Bank, ranging from US$192.92 to US$347.91 per share. As many participants weigh in, the increase in charge-offs highlights how changing credit quality may sway future earnings and investor confidence.

Explore 5 other fair value estimates on M&T Bank - why the stock might be worth as much as 88% more than the current price!

Build Your Own M&T Bank Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your M&T Bank research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free M&T Bank research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate M&T Bank's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com