Honeywell (HON): Exploring Valuation After Subtle Share Price Shift and Spin-Off Plans

Honeywell International (HON) shares edged higher today, changing by just under 0.03%. The stock’s movement caught attention in a backdrop of generally modest trading, prompting some investors to re-examine how Honeywell’s fundamentals line up in the current market environment.

See our latest analysis for Honeywell International.

Honeywell’s share price has drifted lower lately, with a year-to-date decline of 7.5%. Despite a small uptick today, the momentum has faded somewhat compared to earlier in the year. For investors looking at the bigger picture, total shareholder return has remained positive over longer periods, with a 23.6% gain over three years and 33.2% over five years.

If you’re interested in finding more opportunities beyond the industrial giants, now could be the ideal moment to discover fast growing stocks with high insider ownership.

With shares lagging and trading below many analyst price targets, some investors are now weighing whether Honeywell is undervalued or if the market has already factored in the company's future growth prospects. Could there be a buying opportunity, or is everything priced in?

Most Popular Narrative: 17.5% Undervalued

According to the current narrative, Honeywell’s consensus fair value stands well above its recent closing price, suggesting the stock could have meaningful upside if projections come true.

Honeywell's decision to separate into three independent companies (Automation, Aerospace, and Advanced Materials) could unlock significant value and better position each entity for long-term growth. This may impact revenue and margins positively. The acquisition of Sundyne and strategic bolt-on acquisitions are expected to enhance Honeywell's business profile, increasing both organic growth and segment margins by expanding their portfolio of solutions.

Want to know the growth blueprint behind this ambitious price call? The narrative revolves around bolder than expected profit margins and a revenue climb that challenges its slow-growth reputation. The anticipated numbers driving this fair value are not just more of the same; they signal a strategic pivot and significant moves aimed at future earnings. Ready to see how far these forecasts go?

Result: Fair Value of $252.97 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifting global trade patterns or execution missteps in the company’s upcoming separation could challenge the optimistic outlook that analysts currently expect.

Find out about the key risks to this Honeywell International narrative.

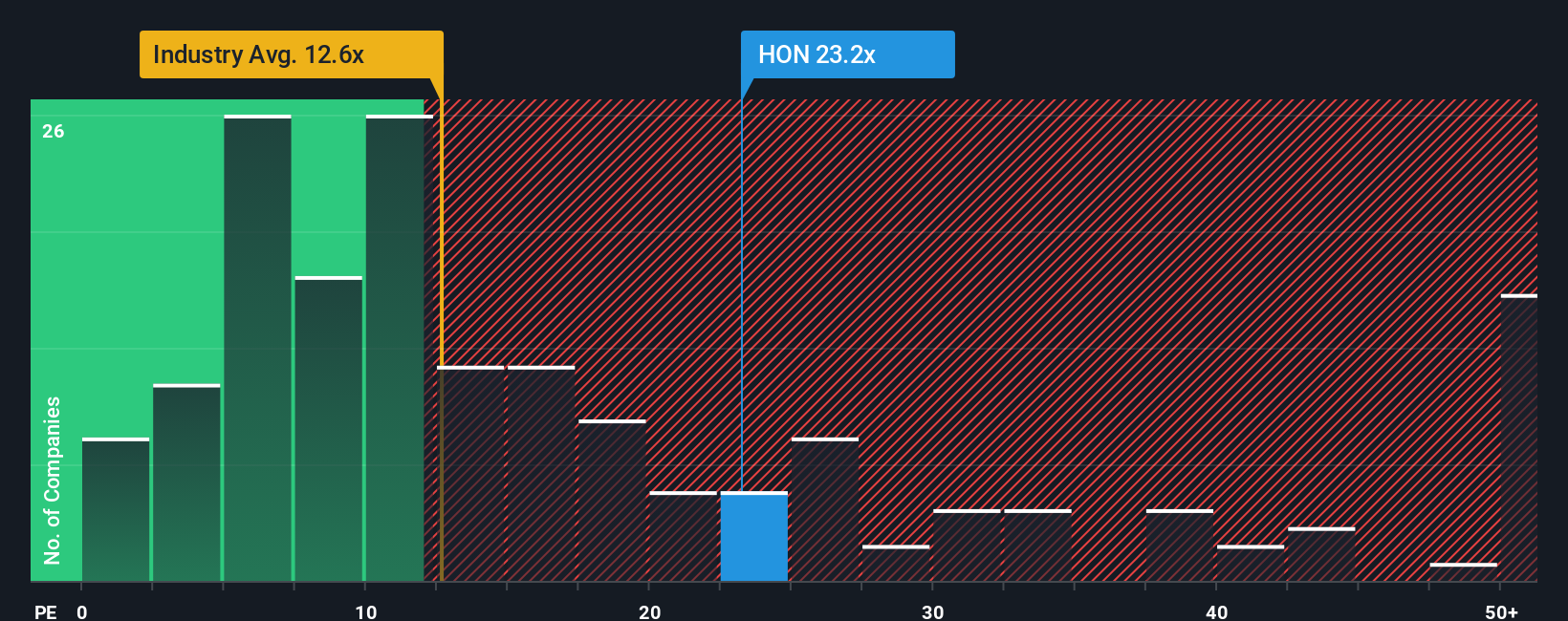

Another View: Valuation Through Market Ratios

While analyst targets suggest upside, the market’s pricing tells a more complex story. Honeywell’s price-to-earnings ratio sits at 23.2x, which is higher than the global industrials industry average of 12.7x, but still below the peer average of 27.3x and under its estimated fair ratio of 28.7x. This mix of premium and undervaluation indicators hints that market sentiment remains cautious, despite positive forecasts. Could the stock’s current price signal both risk and opportunity depending on which benchmark proves more important?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Honeywell International Narrative

If you want a different perspective or like to dig deeper on your own terms, you can shape your own Honeywell story in just a few minutes. Do it your way.

A great starting point for your Honeywell International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors keep options open, and the right screener tools can reveal exciting stocks that most people overlook. If you want to get ahead of the curve and jump on the next big thing, don’t sit on the sidelines.

- Tap into next-generation healthcare breakthroughs by using these 33 healthcare AI stocks to spot companies harnessing artificial intelligence for medical innovation.

- Find hidden value by reviewing these 881 undervalued stocks based on cash flows to see which stocks stand out for strong cash flow potential and attractive pricing.

- Start growing your income stream now by using these 18 dividend stocks with yields > 3% to uncover high-yield opportunities delivering more than 3% returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com