Tootsie Roll (TR) Valuation: Is the Classic Candy Stock Trading Above or Below Fair Value?

Tootsie Roll Industries (TR) stock has quietly outperformed over the past year, delivering a 45% return while flying under the radar for many investors. This steady climb draws attention to its classic candy business and resilient cash flow.

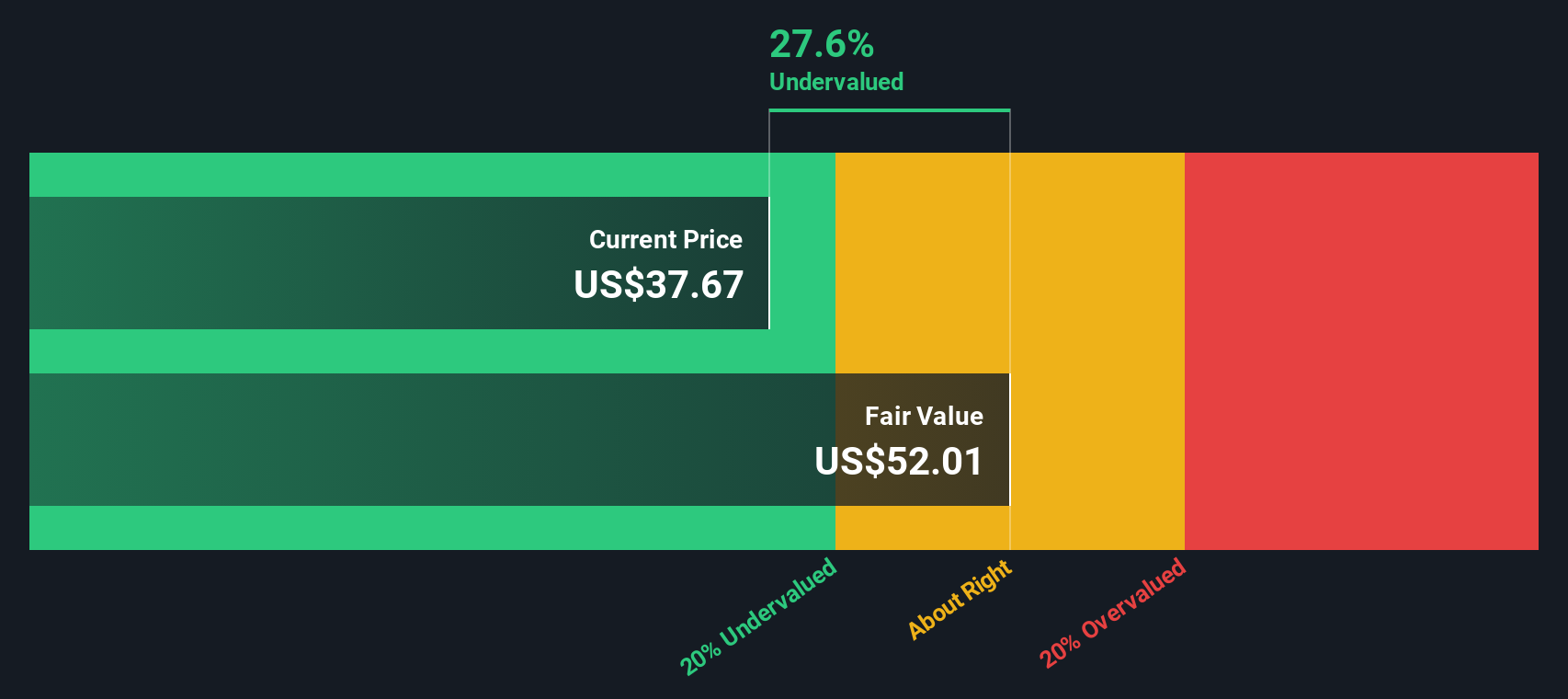

See our latest analysis for Tootsie Roll Industries.

Shares have surged this year, with a 32.3% year-to-date share price return highlighting growing optimism around Tootsie Roll Industries. Even after last week’s pullback, the 1-year total shareholder return of 44.6% reflects persistent momentum and renewed interest from investors.

If you're considering what else is catching investors’ attention lately, now is a good time to broaden your search and discover fast growing stocks with high insider ownership.

But with shares at decade highs and a 20% estimated intrinsic discount, the real question is whether Tootsie Roll Industries is undervalued or if the market has already factored in all future growth. Is there still a buying opportunity?

Price-to-Earnings of 33.5x: Is it justified?

At a closing price of $41.87, Tootsie Roll Industries trades at a notably high price-to-earnings (P/E) ratio of 33.5x. This places it well above its industry peers and signals that the market is assigning a premium to the stock.

The price-to-earnings multiple represents what investors are willing to pay today for each dollar of the company’s earnings. For Tootsie Roll Industries, a P/E of 33.5x means investors are currently paying much more for its earnings compared to similar companies in the food sector.

This multiple stands out as expensive. The average P/E ratio among the company’s peers is just 19.8x, while the broader US Food industry trades around 17.7x. The current market price clearly reflects higher expectations for Tootsie Roll Industries’ future performance, even though recent profit growth has not outpaced the industry or broader market. Unless future results meaningfully improve, there is a risk the valuation could revert closer to peer levels.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 33.5x (OVERVALUED)

However, slower revenue or profit growth could quickly change sentiment. This could make the current high valuation vulnerable if expectations are not met.

Find out about the key risks to this Tootsie Roll Industries narrative.

Another View: DCF Suggests Undervaluation

While the price-to-earnings ratio highlights Tootsie Roll Industries as expensive compared to its peers, the SWS DCF model offers a different perspective. According to our DCF analysis, the current price is trading nearly 20% below estimated fair value, suggesting potential undervaluation.

Look into how the SWS DCF model arrives at its fair value.

With both valuation methods painting such a different picture, which one will the market ultimately trust? What factors could influence the outcome in either direction?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tootsie Roll Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Tootsie Roll Industries Narrative

If you have a different perspective or enjoy building your own investment thesis, it only takes a few minutes to craft your unique narrative. Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Tootsie Roll Industries.

Looking for more investment ideas?

Uncover your next investment win by using these expert-curated lists. Smart moves now could put you ahead of the crowd. Opportunities like these do not wait.

- Capture high yield potential by scanning these 18 dividend stocks with yields > 3% that consistently deliver strong payouts above 3%, helping you grow passive income while you invest.

- Get ahead of market shifts with these 25 AI penny stocks poised to benefit most as artificial intelligence transforms entire industries and unlocks new growth.

- Target hidden value by browsing these 891 undervalued stocks based on cash flows where cash flow fundamentals point to overlooked companies primed for a rerating.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com