A Fresh Look at monday.com (MNDY) Valuation Following Buyback Announcement and Upcoming Earnings

Investor interest in monday.com (MNDY) has picked up ahead of its upcoming earnings, with expectations for growth in both revenue and earnings. Despite sector swings and some cautious sentiment, management’s US$870 million share buyback signals their confidence in the company’s long-term prospects.

See our latest analysis for monday.com.

monday.com’s share price has been affected by recent sell-offs in the tech sector, with a 90-day share price return of -34.9% and a year-to-date return of -19.9%. However, taking a broader view reveals another perspective: after last year’s strong gains, the 1-year total shareholder return is still down by 36.6%, but long-term shareholders have seen a 97.2% gain over three years. Momentum has slowed since previous highs, but investor interest continues as reflected by buyback news and growth prospects.

If you’re curious what other high-momentum growth stories are unfolding right now, it’s a great moment to discover fast growing stocks with high insider ownership

With analysts split and shares trading well below the consensus price target, the question now is whether monday.com represents an undervalued opportunity or if the market has already accounted for its potential growth.

Most Popular Narrative: 31.3% Undervalued

With monday.com’s most widely-followed narrative fair value set at $269.46, the last closing price of $185.03 is far below expectations, highlighting major upside according to consensus forecasts. This gap puts the focus squarely on ambitious growth and profitability assumptions driving the story forward.

Ongoing global shift toward digital transformation, remote/hybrid work, and rising SaaS adoption continues fueling strong demand for cloud-based productivity and collaboration platforms like monday.com, supporting high double-digit revenue growth and future ARR expansion. Rapid integration of generative AI and low-code/no-code capabilities (e.g., Monday Magic, Vibe, Sidekick) enable broader automation and workflow customization, strengthening platform differentiation and stickiness. This will likely improve customer retention, ARPU, and net margins as monetization scales.

What core forces justify such a premium? The real action is in bold growth forecasts, especially the future profit margins and sales ramp included in this valuation. Want to see the numbers that drive this potential?

Result: Fair Value of $269.46 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain, particularly around slowing self-serve customer growth and heightened competition. These factors could challenge revenue momentum and monday.com's current narrative.

Find out about the key risks to this monday.com narrative.

Another View: Are Market Multiples Sending a Different Signal?

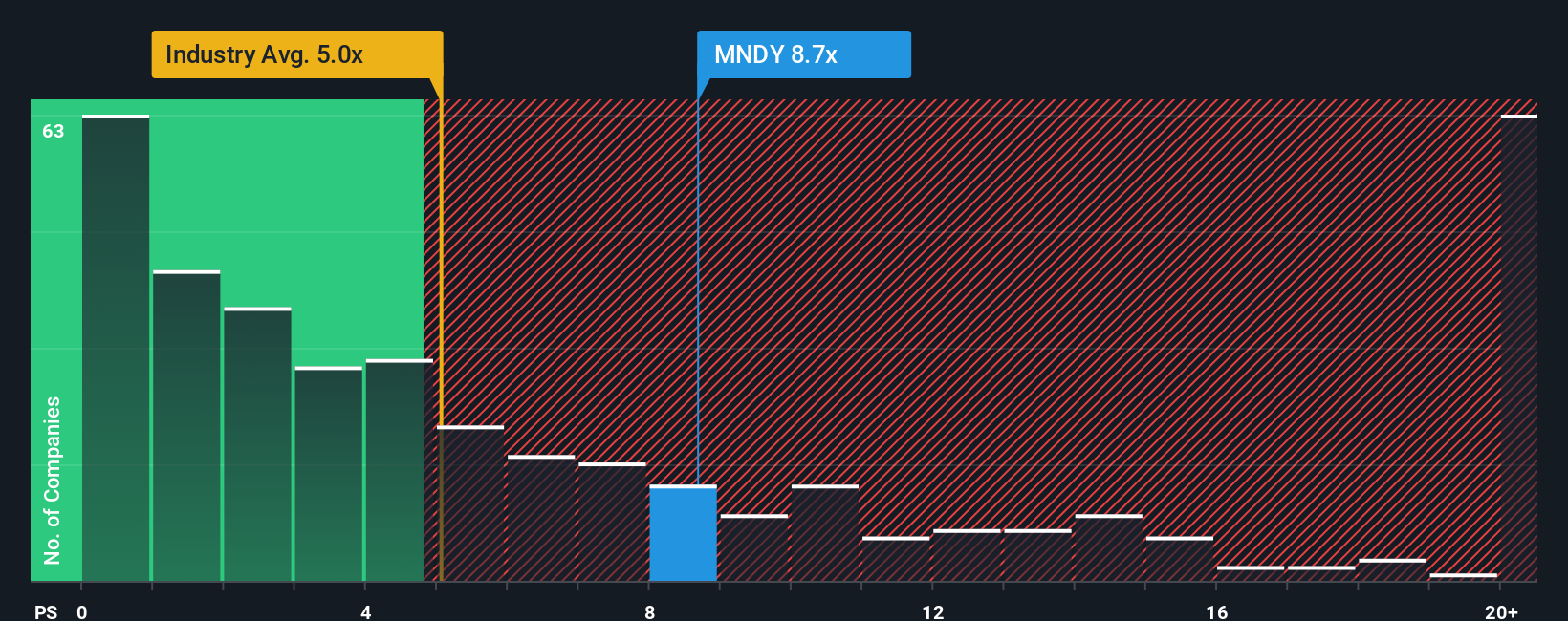

Looking through the lens of price-to-sales, monday.com trades at 8.7 times sales, which is above both the US Software industry average of 5x and the peer group’s 7.1x. However, it remains below the fair ratio of 12x. This creates a tension between perceived expensiveness in today’s market and potential upside if the market shifts. Could the gap close, or is current pricing a warning sign?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own monday.com Narrative

If you see the story differently or want to dive deeper into your own research, you can build your own thesis in just a few minutes, too. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding monday.com.

Looking for More Smart Investment Ideas?

Don’t let fresh opportunities slip through your fingers when the next great stock could be right around the corner. Open the door to powerful new trends with these handpicked screeners:

- Uncover established companies offering attractive payouts by reviewing these 19 dividend stocks with yields > 3%. These options boast yields above 3% and strong income potential.

- Tap into the future of medicine by checking out these 33 healthcare AI stocks, which highlights innovation with artificial intelligence in healthcare and patient solutions.

- Spot undervalued growth stories by assessing these 891 undervalued stocks based on cash flows that appear to be positioned for a comeback based on compelling cash flow signals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com