Rethinking ZOZO Stock Valuation After a 15% Drop in 2025

If you’ve ever tried to decide what to do with a stock that’s down for the year but still up by double digits over the long term, then you know how tricky it can be to decode the story behind the numbers. That is exactly where ZOZO finds itself today. The share price has slipped by 0.7% over the last week and is down 3.8% for the past month. More notably, it is off 15.4% year-to-date and down 21.7% over the last twelve months. However, when you look at the bigger picture, the gains since 2019 become clear, with the stock up 44.5% over three years and 45.9% over five years.

Recent months in the broader market have been defined by changing risk perceptions and shifting appetites for growth. While these moves have not always had direct news triggers for ZOZO, investor sentiment has generally turned cautious toward online retail after an extended period of optimism. This has led some investors to question whether now is a good time to buy, hold, or let go of ZOZO stock altogether.

So how does the company stack up on valuation? If we run it through a standard checklist approach with six key ways a company can look undervalued, ZOZO scores a 0. In other words, based on these common checks, it does not appear undervalued in any area. But are those the only ways to think about value here? Next, we will look at what those methods actually tell us, and why the best way to assess ZOZO’s true worth might surprise you.

ZOZO scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

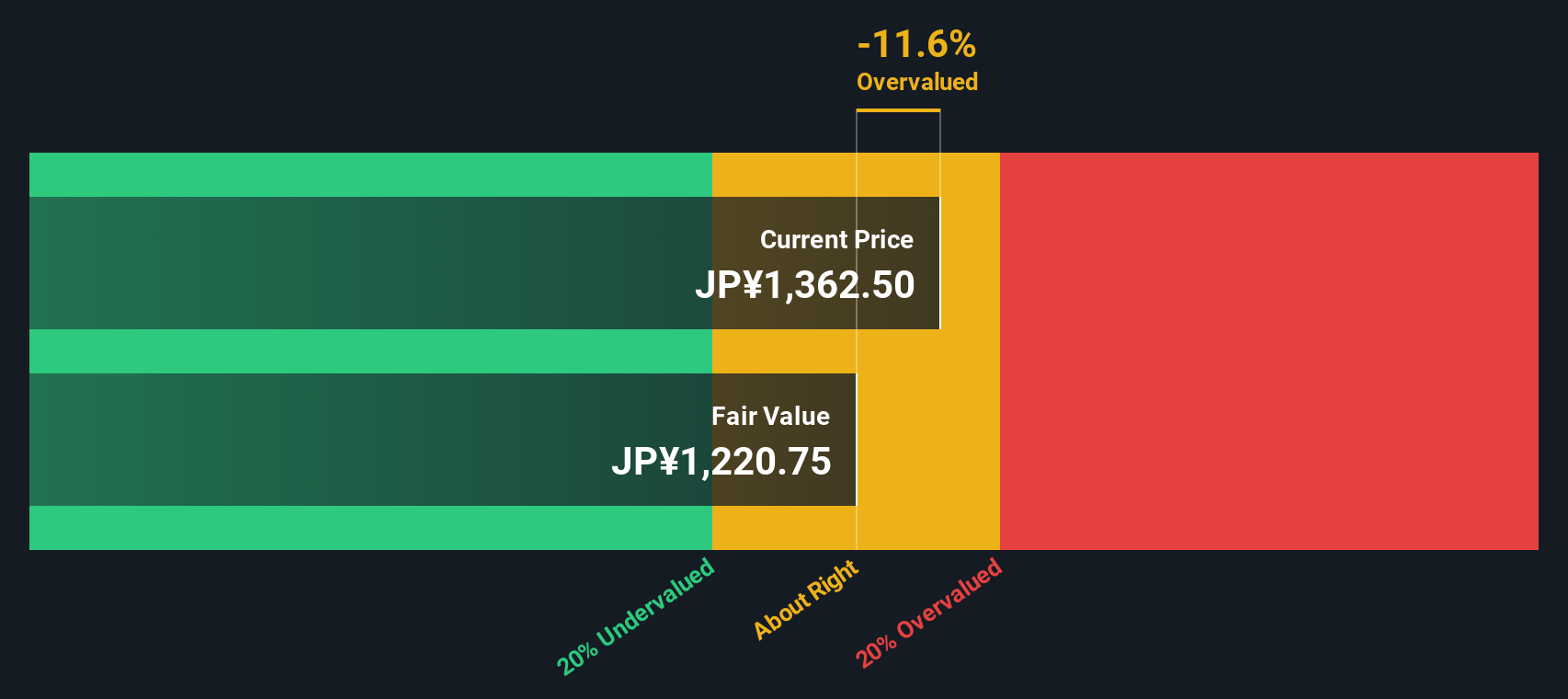

Approach 1: ZOZO Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the intrinsic value of a company by projecting its future cash flows and discounting them back to today’s value. This approach aims to determine what the business is worth based on its expected ability to generate cash in the future. All figures are considered in Japanese yen (¥).

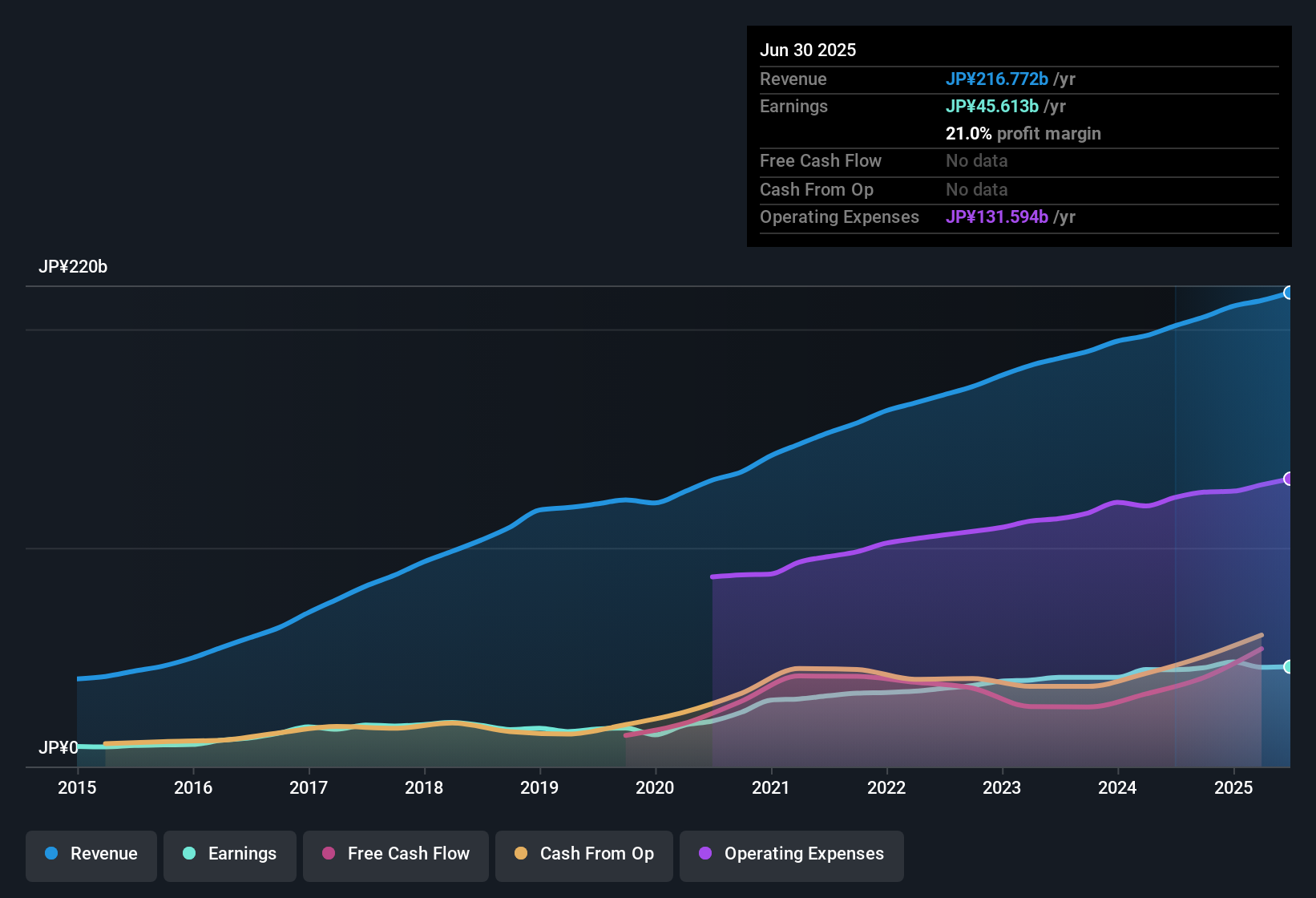

ZOZO’s most recent reported Free Cash Flow stands at ¥51.3 billion. Analyst estimates cover projections for the next five years, after which further numbers are extrapolated. By 2030, Free Cash Flow is forecast to reach ¥62.3 billion. This steady growth highlights both analyst confidence and the model's conservatism for later years.

Based on this DCF model, the estimated fair value per share comes to ¥1,212. Compared with the current market price, the model implies that the stock is trading at an 11.4% premium. This suggests ZOZO shares currently look to be overvalued using this method.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ZOZO may be overvalued by 11.4%. Find undervalued stocks or create your own screener to find better value opportunities.

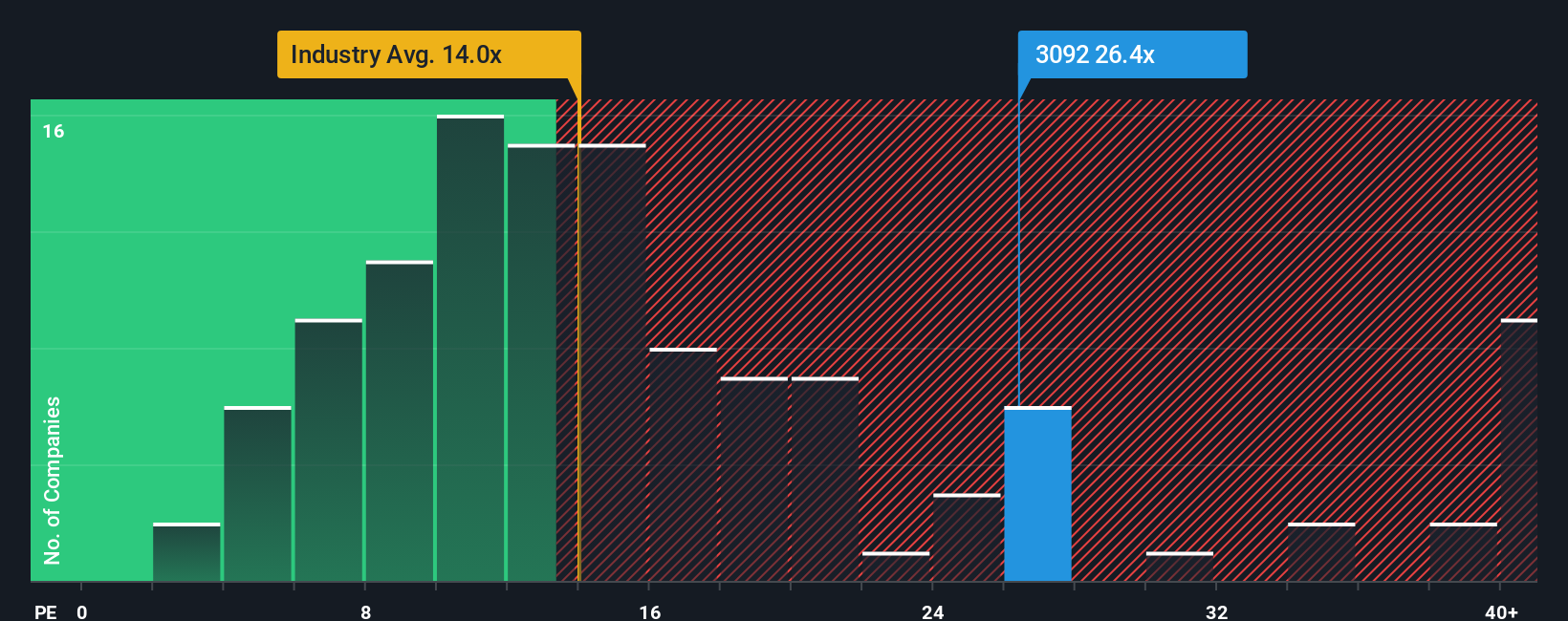

Approach 2: ZOZO Price vs Earnings (PE Ratio)

The Price-to-Earnings (PE) ratio is a widely used metric for valuing profitable companies because it shows how much investors are willing to pay for a unit of current earnings. For companies like ZOZO with a healthy profit history, the PE ratio offers a quick way to gauge whether the stock's price makes sense relative to what it actually earns.

Growth expectations and risk both play crucial roles in shaping what a “normal” PE ratio should be. Investors typically accept a higher PE for companies with faster earnings growth or lower risk, while those with uncertain prospects or slower growth tend to trade on lower multiples by comparison.

Currently, ZOZO trades at a PE ratio of 26.2x. That stands noticeably above the specialty retail industry average of 14.3x and even above the average for its closest peers at 22.8x. However, headline comparisons do not always tell the full story. This is where the Fair Ratio comes in. Simply Wall St’s Fair Ratio for ZOZO is 20.9x, reflecting what would be a reasonable PE for the company after factoring in its unique growth outlook, profit margins, risks, and market position.

Rather than using industry or peer benchmarks, the Fair Ratio provides a nuanced measure tailored to ZOZO, combining both company-specific strengths and broader market realities. It helps avoid the pitfalls of one-size-fits-all valuation comparisons.

Looking at ZOZO’s current PE of 26.2x versus the Fair Ratio of 20.9x, the stock trades well above its justified valuation. This suggests that, based on earnings, ZOZO is overvalued relative to the factors that matter most for its future returns.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ZOZO Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story about a company, a perspective that goes beyond the numbers, weaving together your assumptions about its future revenue, profit margins, risks and what you believe is a fair value for the shares. Narratives link ZOZO’s unique business story to a financial forecast and then connect that to a concrete estimate of fair value.

With Narratives, you do not have to be a finance expert; they are an intuitive, accessible tool available to millions of investors on Simply Wall St's Community page. Narratives empower you to decide for yourself when it makes sense to buy, hold, or sell by comparing your calculated Fair Value with the current Price. They update dynamically as new news or earnings results roll in, so your viewpoint stays relevant and informed.

For example, some investors see ZOZO’s international expansion and AI-powered personalization as catalysts for strong growth and set a bullish fair value as high as ¥2,100. Others focus on risks from competition and margin pressure and estimate a fair value as low as ¥1,000. Your Narrative can be anywhere in between, and you’re always in control.

Do you think there's more to the story for ZOZO? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com