Has NFI Group’s Recent 17% Drop Created a New Opportunity for Investors?

Thinking about what to do with NFI Group stock right now? You are definitely not alone. This is a company that has drawn plenty of attention from value-minded investors, and with good reason. Despite a rough patch in the last month, as the stock is down 17.6% over 30 days, the longer term numbers tell a more nuanced story. Up 5.6% year-to-date, but still a ways off from its three-year high with only an 18.6% gain and down 12.7% over the past year, NFI's price movements reflect both the optimism and the uncertainty swirling around the public transit and electric bus sector lately.

Some of that volatility can be traced to broader shifts in how the market views companies tied to the electrification of transportation. Every time a major city pledges to update its bus fleet with greener technology or a government offers new incentives to public transit operators, NFI Group pops up on investor radars, sparking quick share price reactions. But the ups and downs also hint at shifting risk tolerance, not just in NFI but in the wider sector. That means the current price could present an opportunity for those who know where to look.

And here is where the numbers get really compelling. According to the latest valuation checks, NFI Group scores a perfect 6 out of 6 on undervaluation tests. That alone deserves a deeper look, especially for long-term value-seekers. Let us dig into the different valuation methods, and then tackle what I think is the smarter way to gauge whether NFI Group is actually a buy at these levels.

Why NFI Group is lagging behind its peers

Approach 1: NFI Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to today's dollars. For NFI Group, this involves analyzing how much free cash the business is expected to generate and then calculating what that is worth in the present moment.

Currently, NFI Group reports a last twelve months (LTM) free cash flow of -$101.7 Million, highlighting recent challenges in reaching positive operating cash. However, projections appear optimistic, as analysts expect free cash flow to rebound and reach $167.8 Million by the end of 2026. Extended forecasts by Simply Wall St estimate this figure could climb to over $1 Billion within 10 years.

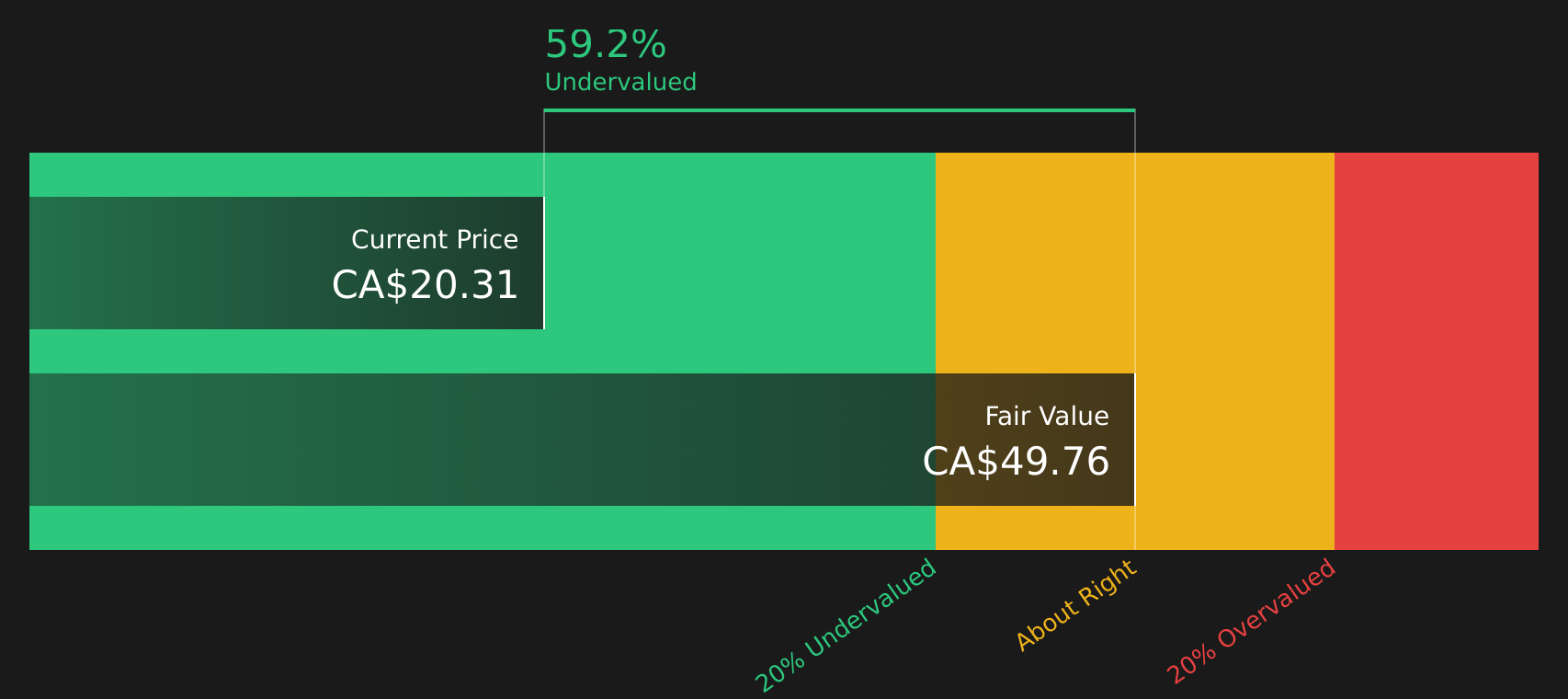

This projected growth forms the basis of the two-stage Free Cash Flow to Equity model used here. When all projected cash flows are discounted back to today, the calculated intrinsic share value stands at $115.07. According to the DCF model, this indicates that NFI Group is currently trading at an 86.8% discount to its fair value, suggesting significant undervaluation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NFI Group is undervalued by 86.8%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: NFI Group Price vs Sales

Another way to look at NFI Group's valuation is by using its price-to-sales (P/S) ratio. This multiple is especially useful for companies like NFI Group, which may be unprofitable currently but still have significant revenue. The P/S ratio gauges how much investors are paying for each dollar of the company’s sales. This provides a simple and effective metric for comparative valuation.

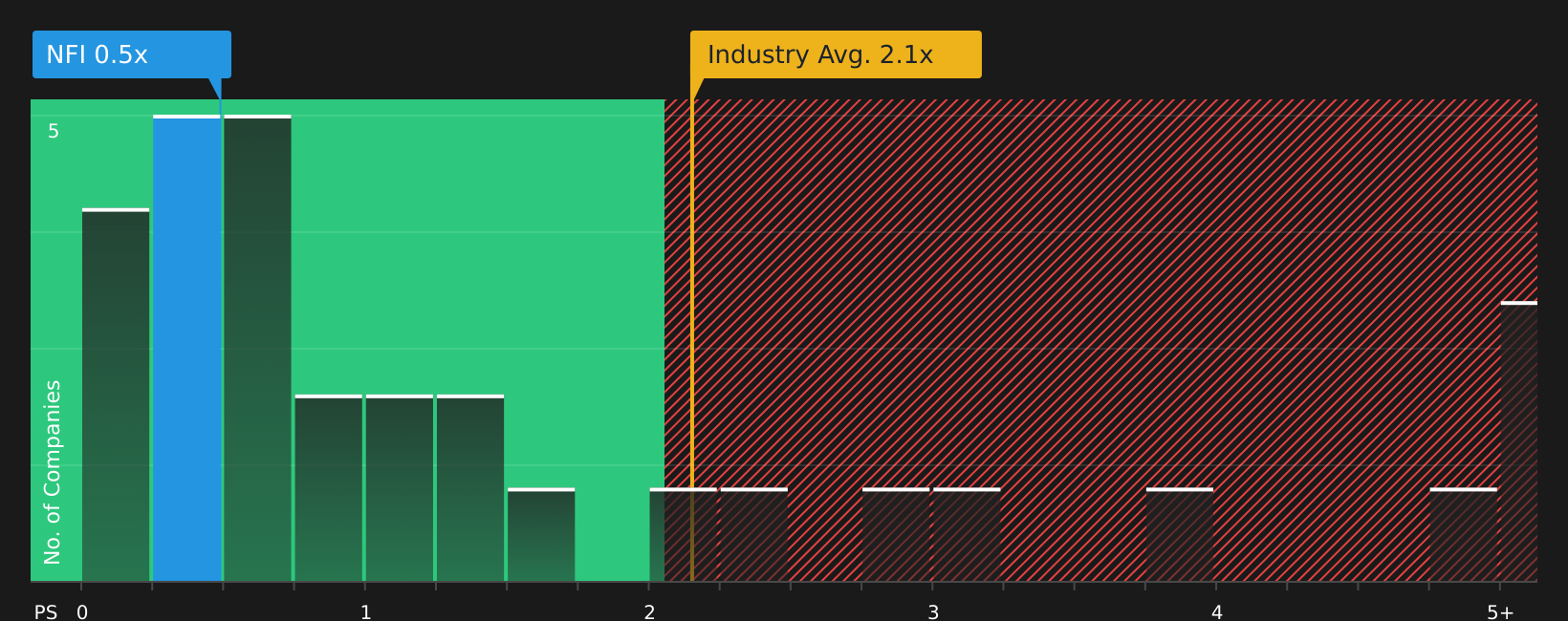

Generally, a "normal" or fair P/S ratio should reflect both growth expectations and risk. Fast-growing companies or those with defensible market positions tend to command higher P/S ratios, while those with more risk or slower growth remain closer to or below the industry average. As of now, NFI’s P/S stands at just 0.40x. For context, the broader Machinery industry averages a much higher 1.75x, and the company's peer group averages about 1.03x.

This is where Simply Wall St’s Fair Ratio stands out. The Fair Ratio, currently calculated at 1.15x for NFI Group, is more comprehensive than a simple peer or industry comparison. It incorporates NFI's unique factors such as growth prospects, profit margin outlook, industry specifics, market cap, and risk profile. This offers a tailored view of fair value in today’s market rather than relying on blunt averages.

With NFI Group’s current P/S at 0.40x, well below the Fair Ratio of 1.15x, this proprietary analysis suggests the stock is trading at a substantial discount to what would be considered reasonable based on its fundamentals and outlook.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your NFI Group Narrative

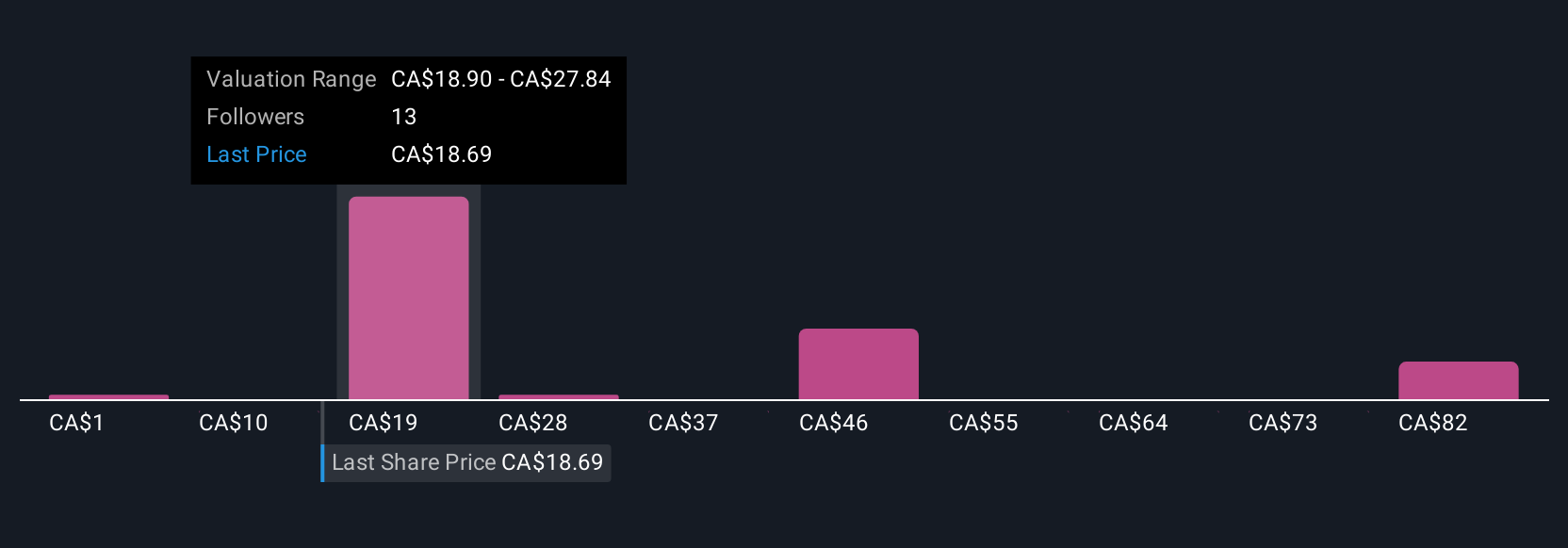

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply your own story about where you believe NFI Group is heading, connecting the facts of the business with your assumptions about its future revenue, earnings, and margins.

Rather than just sticking to rigid models or averages, Narratives empower you to link the company’s business reality to your personal forecasts, and then quantify your fair value for the stock. This approach allows you to make investment decisions that truly reflect your view of the company, not just what the market thinks.

Narratives are available directly on Simply Wall St’s Community page, used by millions of investors, making sophisticated stock analysis accessible to everyone. They help you quickly see if your view means NFI Group is a buy or a sell, by comparing your calculated Fair Value with today’s share price.

Even better, Narratives update automatically as new news or earnings come out, so you are always working with the latest information. For example, one investor might see NFI’s record backlog and government funding as powerful drivers, and set a Fair Value of CA$26.98, while another worries about debt and competition and uses CA$22.96. Each Narrative tells a story behind the number.

Do you think there's more to the story for NFI Group? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com