Assessing Agnico Eagle After Its 121% Climb and New All-Time High in 2025

If you are wondering what to do next with Agnico Eagle Mines stock, you are definitely not alone. After all, it is not every day you see a gold miner post a jaw-dropping 107.8% return so far this year, and an incredible 121.2% over the past twelve months. Even the short-term numbers impress, with the stock up 2.2% in just the last week and notching a hefty 12.2% gain over the past month. These returns have left many investors asking whether the stock’s momentum is sustainable or if risk has caught up to the upside.

Much of the excitement around Agnico Eagle Mines has been fueled by notable shifts in the gold market. As gold prices have surged on the back of global uncertainty and shifting central bank policies, miners have come back into the spotlight. Agnico’s performance over the last three years, a remarkable 336.3%, shows just how much this sector responds when conditions turn favorable. Those moves also tend to spark strong opinions on valuation, with bulls and skeptics both weighing in.

So where does Agnico stand on valuation? Using a simple scoring system, where one point is given for each of six fundamental checks where a company appears undervalued, Agnico Eagle Mines earns just a score of 1. That signals the market may be pricing in plenty of recent growth, but is not necessarily missing a bargain.

But what does that valuation score really mean, and which approaches actually tell the full story? Let’s break down the different valuation methods and stay tuned, because at the end, I will share the one approach that can often be a game changer for long-term investors.

Agnico Eagle Mines scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Agnico Eagle Mines Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a valuation method that estimates the value of a company by projecting its future cash flows and discounting them back to today’s value. This approach helps investors gauge the true, intrinsic worth of a business based on its ability to generate cash in the future.

For Agnico Eagle Mines, analysts estimate the company’s last twelve months Free Cash Flow at $2.88 billion. Looking ahead, projections show Free Cash Flow peaking at $3.93 billion in 2026, before tapering off to about $2.07 billion by 2029. Beyond analyst estimates, Simply Wall St extends these projections out ten years, gradually adjusting for slower growth as uncertainty increases further into the future.

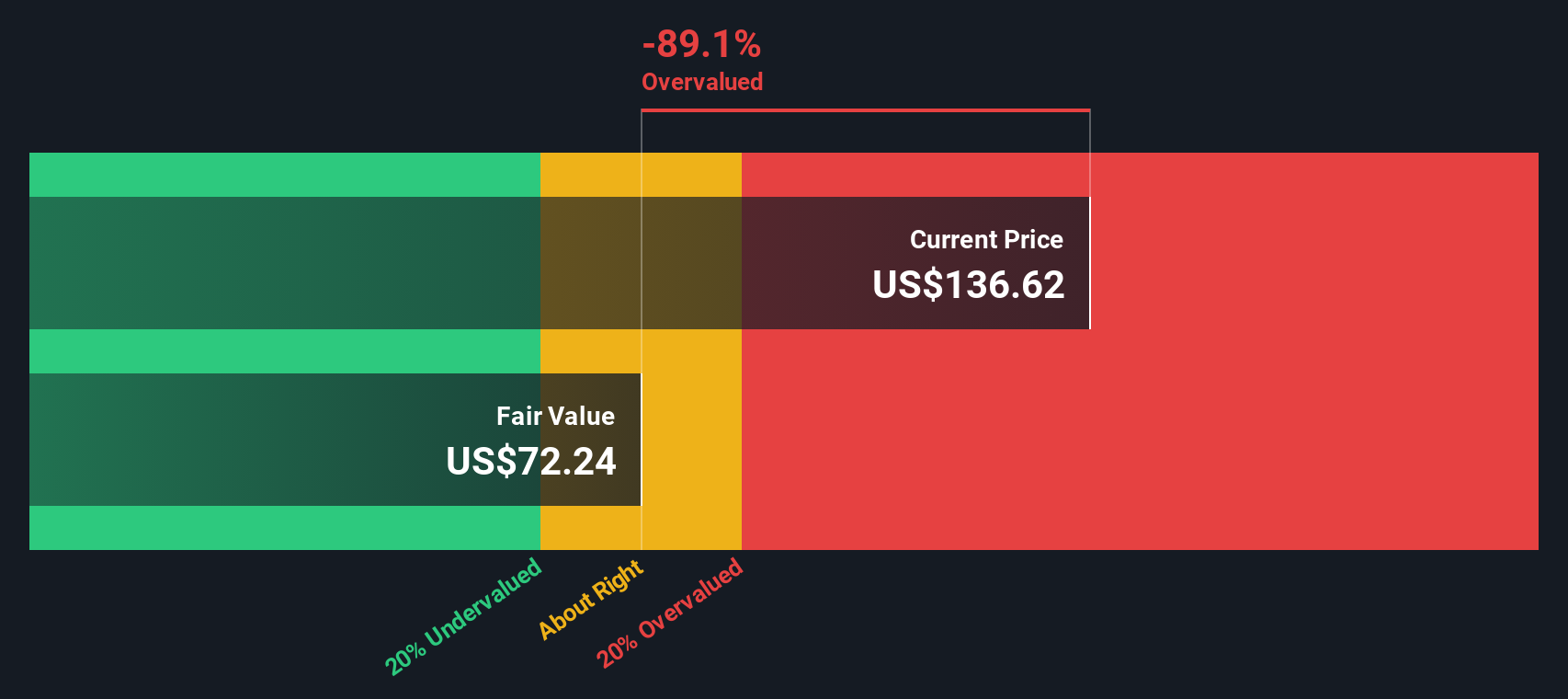

The DCF calculation, using these assumptions, suggests an intrinsic value of $77.83 per share. Given the current share price, this implies Agnico Eagle Mines is trading about 119% above its fair value. In other words, the stock appears to be significantly overvalued according to this model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Agnico Eagle Mines may be overvalued by 118.9%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Agnico Eagle Mines Price vs Earnings

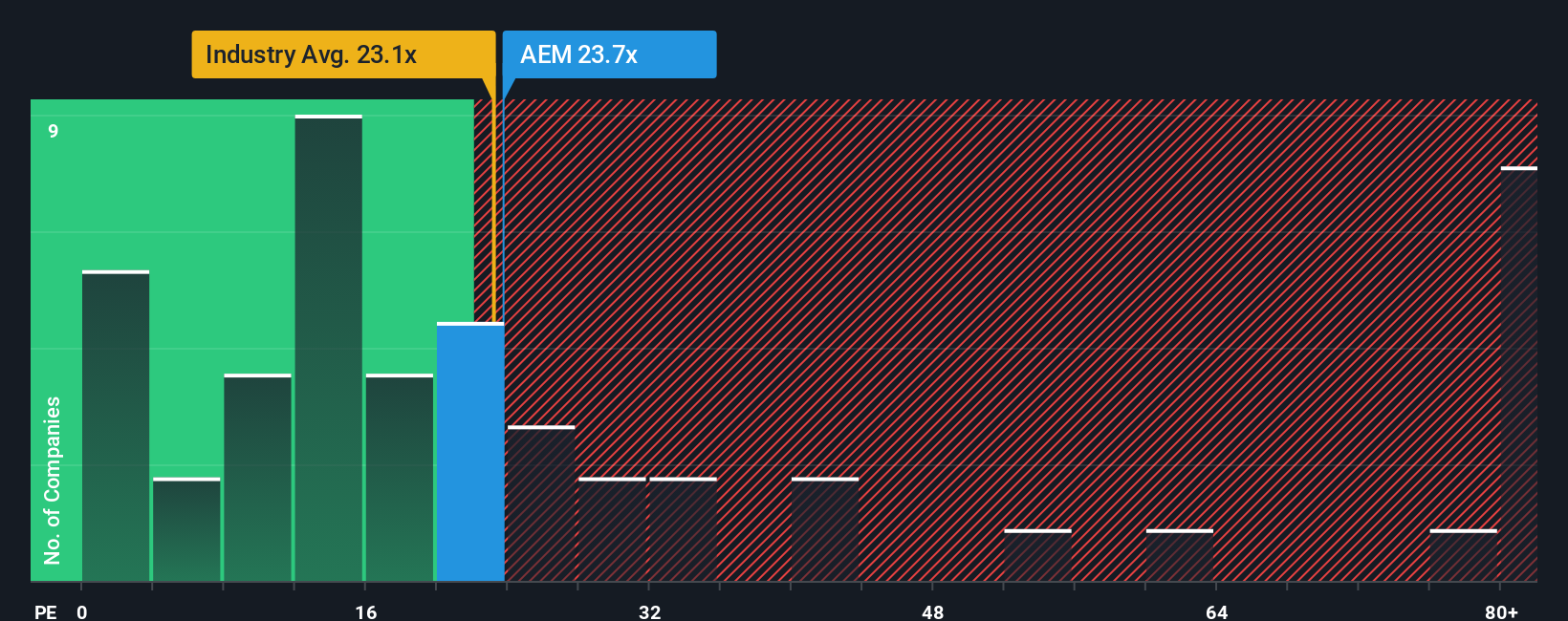

For profitable companies like Agnico Eagle Mines, the Price-to-Earnings (PE) ratio is one of the most widely used metrics for valuation. This ratio gives investors a sense of how much they are paying for each dollar of the company’s current earnings. It is especially helpful for established businesses generating consistent profits, as it helps put today's share price into the context of earnings generation.

When looking at PE ratios, growth expectations and risk play a key role in deciding what is considered “fair.” Faster-growing companies or those with stable earnings usually command higher PE ratios, while those surrounded by uncertainty or cyclical risk see theirs move lower. This is why context matters for every company, including Agnico Eagle Mines.

Currently, Agnico Eagle Mines trades at a PE ratio of 28.9x. That is slightly below the average of its global peers at 32.9x, but above the broader Metals and Mining industry average of 24.1x. However, Simply Wall St’s proprietary “Fair Ratio” calculation for Agnico Eagle Mines is 23.3x. The Fair Ratio takes into account not just peer and industry comparisons, but also the company’s own earnings growth, market cap, profit margins, and specific risk profile. This makes it a more tailored benchmark for Agnico’s valuation than broad-based comparisons alone.

Given that the company's actual PE ratio of 28.9x is noticeably higher than its Fair Ratio of 23.3x, Agnico Eagle Mines appears to be overvalued when using this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Agnico Eagle Mines Narrative

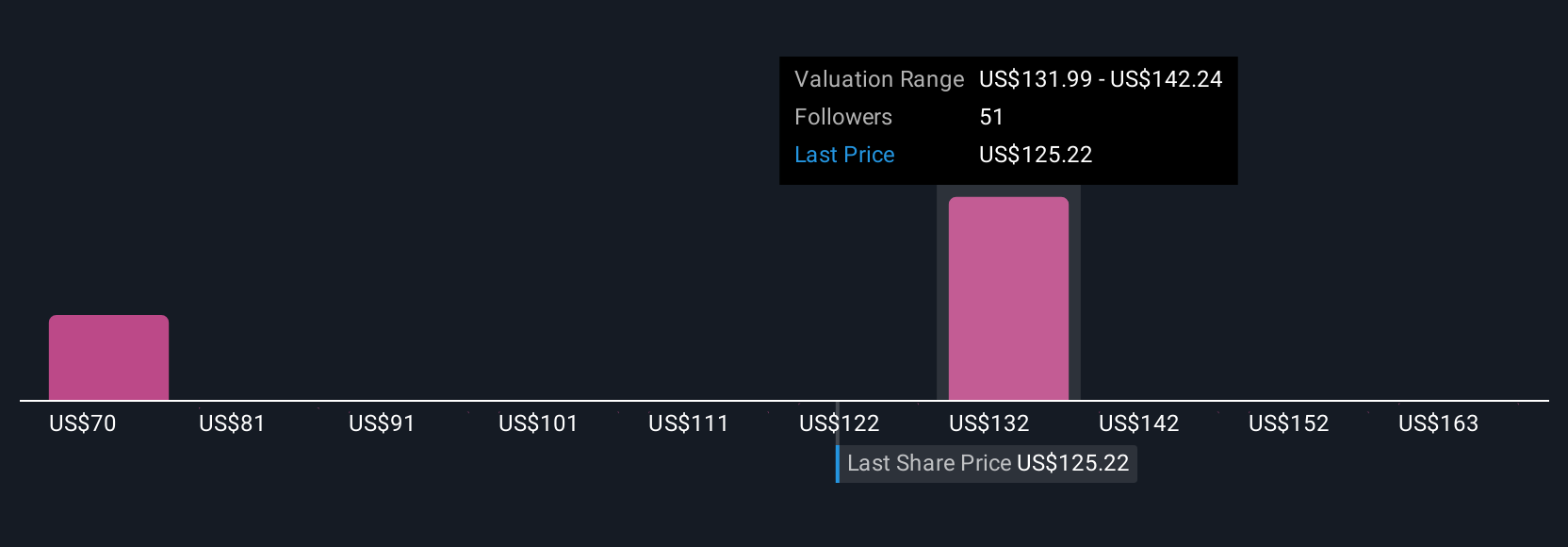

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple, yet powerful tool that lets you connect your personal perspective on a company's future, its story, growth prospects, risks, and opportunities, to your own financial forecast and estimates for key metrics like fair value, future revenue, profit margins, and earnings.

Unlike traditional valuation models that just crunch numbers, Narratives let you bridge the gap between how you see Agnico Eagle Mines performing and what the numbers may mean for its share price. It is a framework that links the company's fundamental story directly to a forecast, and then calculates a fair value all in one place. Available right on Simply Wall St’s Community page (where millions of investors share their views), Narratives are designed to be easy for any user to create, follow, and update.

As new information such as earnings reports or news emerges, Narratives update automatically. This ensures your fair value always reflects the latest developments. For example, one investor might build a bullish Narrative around continued reserve expansion and high gold prices, justifying a fair value approaching $209.00 per share. Another may focus on operational risks or falling gold prices and see value closer to $66.00. Narratives help you compare these outlooks directly to today’s price, so you can confidently decide whether Agnico Eagle Mines is a buy, hold, or sell for you.

Do you think there's more to the story for Agnico Eagle Mines? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com