ASX Penny Stocks Spotlight: D3 Energy And Two Others To Watch

Australian shares are set to experience a modest rise as trading resumes in New South Wales and Queensland, with ASX 200 futures indicating a slight uptick. In this context, penny stocks remain an intriguing segment of the market, often representing smaller or newer companies that can offer both value and growth potential. Despite being considered an outdated term by some, these stocks continue to capture investor interest when backed by strong financials; we'll explore three such promising candidates on the ASX.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Rewards & Risks |

| Alfabs Australia (ASX:AAL) | A$0.495 | A$141.86M | ✅ 4 ⚠️ 3 View Analysis > |

| EZZ Life Science Holdings (ASX:EZZ) | A$2.57 | A$121.24M | ✅ 2 ⚠️ 2 View Analysis > |

| Dusk Group (ASX:DSK) | A$0.80 | A$49.81M | ✅ 4 ⚠️ 2 View Analysis > |

| IVE Group (ASX:IGL) | A$2.75 | A$423.4M | ✅ 4 ⚠️ 3 View Analysis > |

| MotorCycle Holdings (ASX:MTO) | A$3.22 | A$237.66M | ✅ 4 ⚠️ 2 View Analysis > |

| Pureprofile (ASX:PPL) | A$0.043 | A$50.3M | ✅ 3 ⚠️ 1 View Analysis > |

| SHAPE Australia (ASX:SHA) | A$4.95 | A$407.61M | ✅ 3 ⚠️ 2 View Analysis > |

| West African Resources (ASX:WAF) | A$3.04 | A$3.47B | ✅ 4 ⚠️ 1 View Analysis > |

| Praemium (ASX:PPS) | A$0.745 | A$355.9M | ✅ 5 ⚠️ 2 View Analysis > |

| Service Stream (ASX:SSM) | A$2.24 | A$1.37B | ✅ 3 ⚠️ 1 View Analysis > |

Click here to see the full list of 424 stocks from our ASX Penny Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

D3 Energy (ASX:D3E)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: D3 Energy Limited is engaged in the acquisition, exploration, and development of natural gas and helium in South Africa, with a market cap of A$66.44 million.

Operations: D3 Energy Limited has not reported any specific revenue segments.

Market Cap: A$66.44M

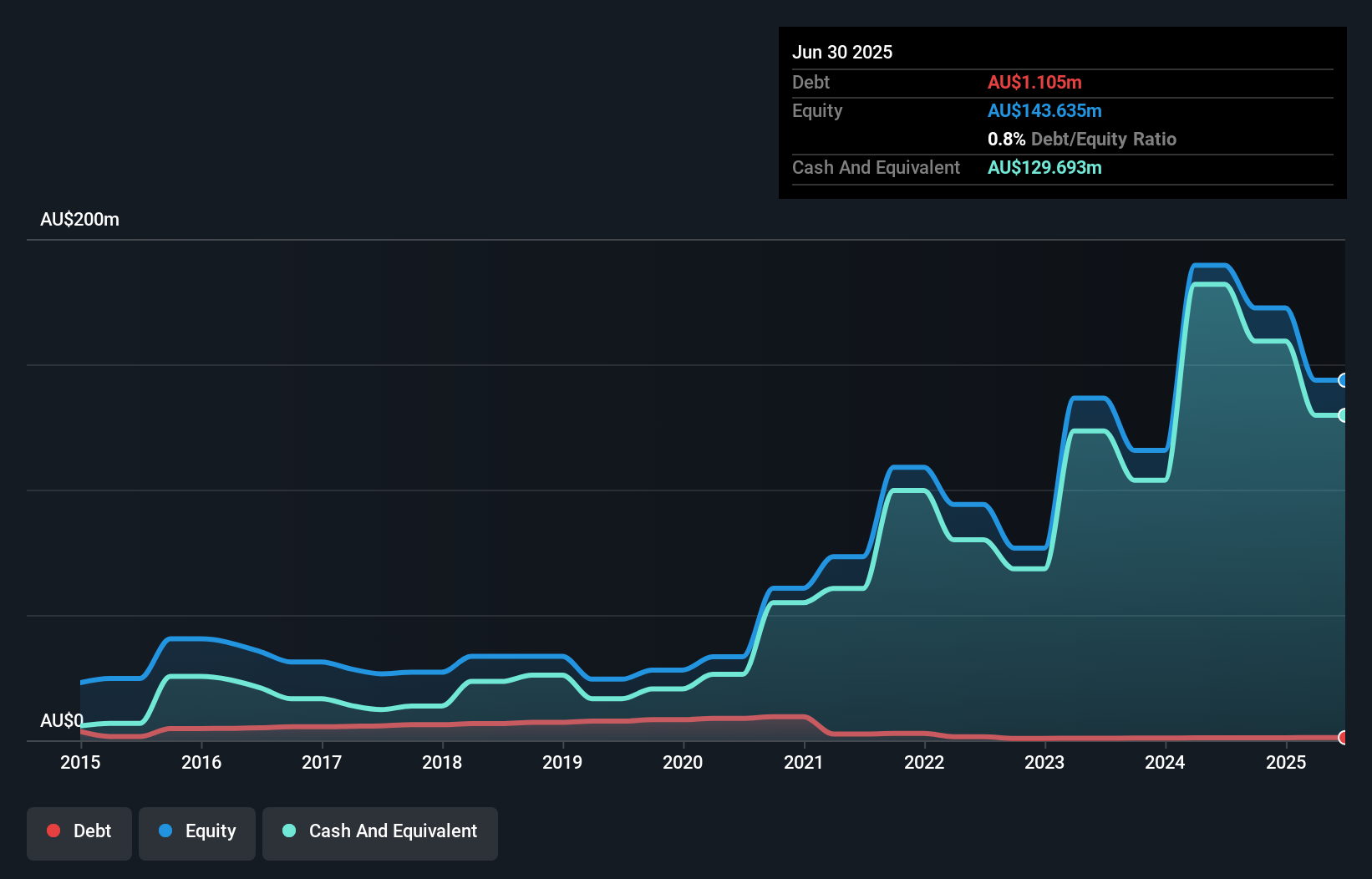

D3 Energy Limited, with a market cap of A$66.44 million, remains pre-revenue as it focuses on natural gas and helium exploration in South Africa. Despite its unprofitability and high share price volatility, the company benefits from being debt-free with sufficient cash runway exceeding one year. Recent developments include launching a 6MW floating solar project in Ohio under a long-term Power Purchase Agreement, highlighting its strategic shift towards renewable energy ventures. However, D3 Energy reported an increased net loss of A$4.08 million for the fiscal year ending June 2025, reflecting ongoing financial challenges typical of early-stage companies in this sector.

- Click to explore a detailed breakdown of our findings in D3 Energy's financial health report.

- Assess D3 Energy's previous results with our detailed historical performance reports.

Immutep (ASX:IMM)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Immutep Limited is a biotechnology company focused on developing innovative Lymphocyte Activation Gene-3 related immunotherapies for cancer and autoimmune diseases in Australia, with a market cap of A$425.68 million.

Operations: The company generates revenue primarily from its immunotherapy segment, which accounts for A$5.03 million.

Market Cap: A$425.68M

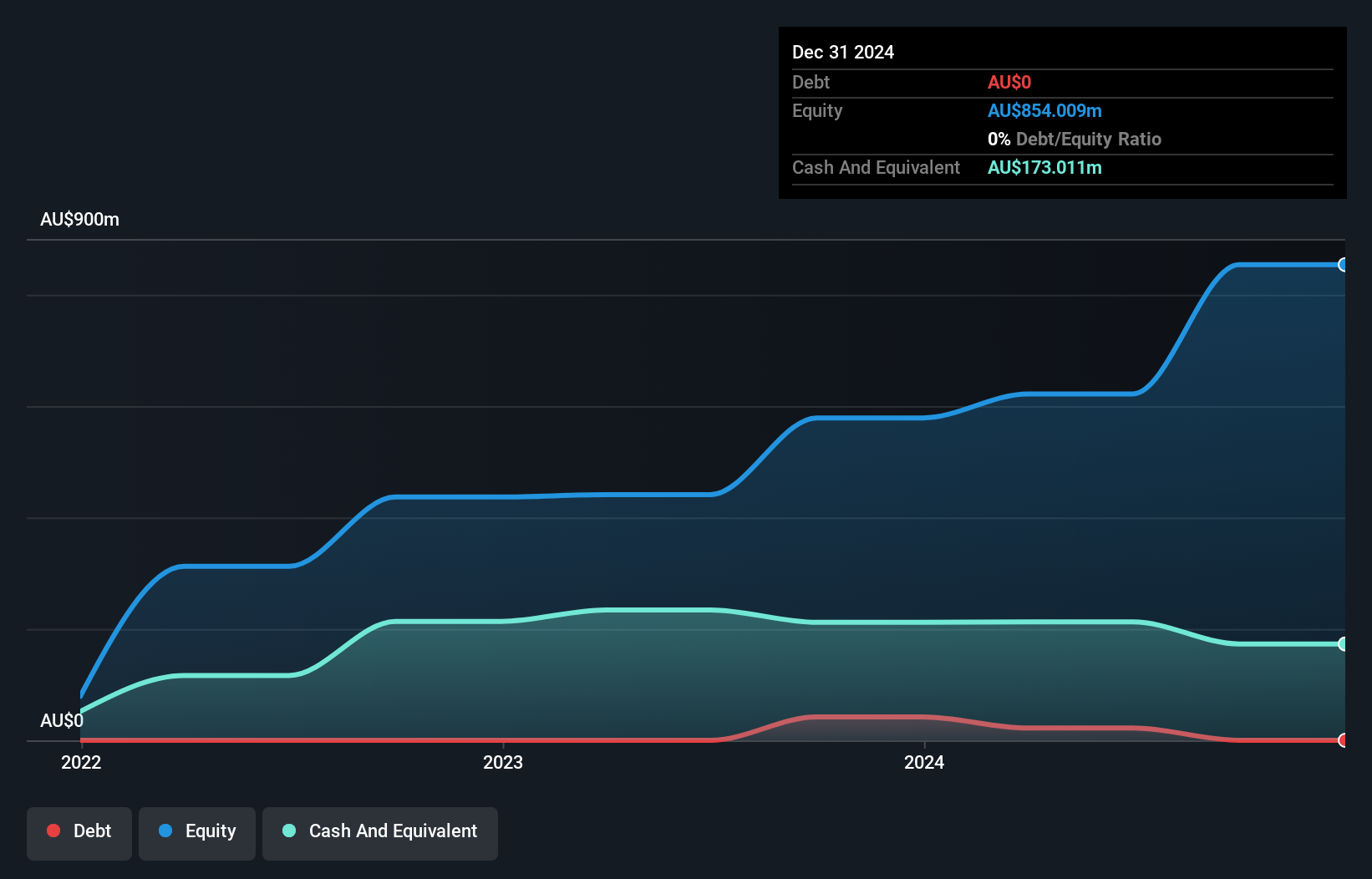

Immutep Limited, with a market cap of A$425.68 million, is pre-revenue, generating A$5.03 million primarily from its immunotherapy segment. Despite being unprofitable and experiencing increased losses over the past five years, the company has reduced its debt significantly and maintains more cash than total debt. Recent strategic alliances include a Phase II trial for their lead product eftilagimod alfa (efti) in breast cancer treatment, supported by grants and technical collaboration with The George Washington University Cancer Center. Positive feedback from the FDA on efti's potential in head and neck cancer highlights promising avenues for future development.

- Get an in-depth perspective on Immutep's performance by reading our balance sheet health report here.

- Review our growth performance report to gain insights into Immutep's future.

Regal Partners (ASX:RPL)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Regal Partners Limited is a privately owned hedge fund sponsor with a market cap of A$1.21 billion.

Operations: The company generates revenue of A$245.45 million through its investment management services segment.

Market Cap: A$1.21B

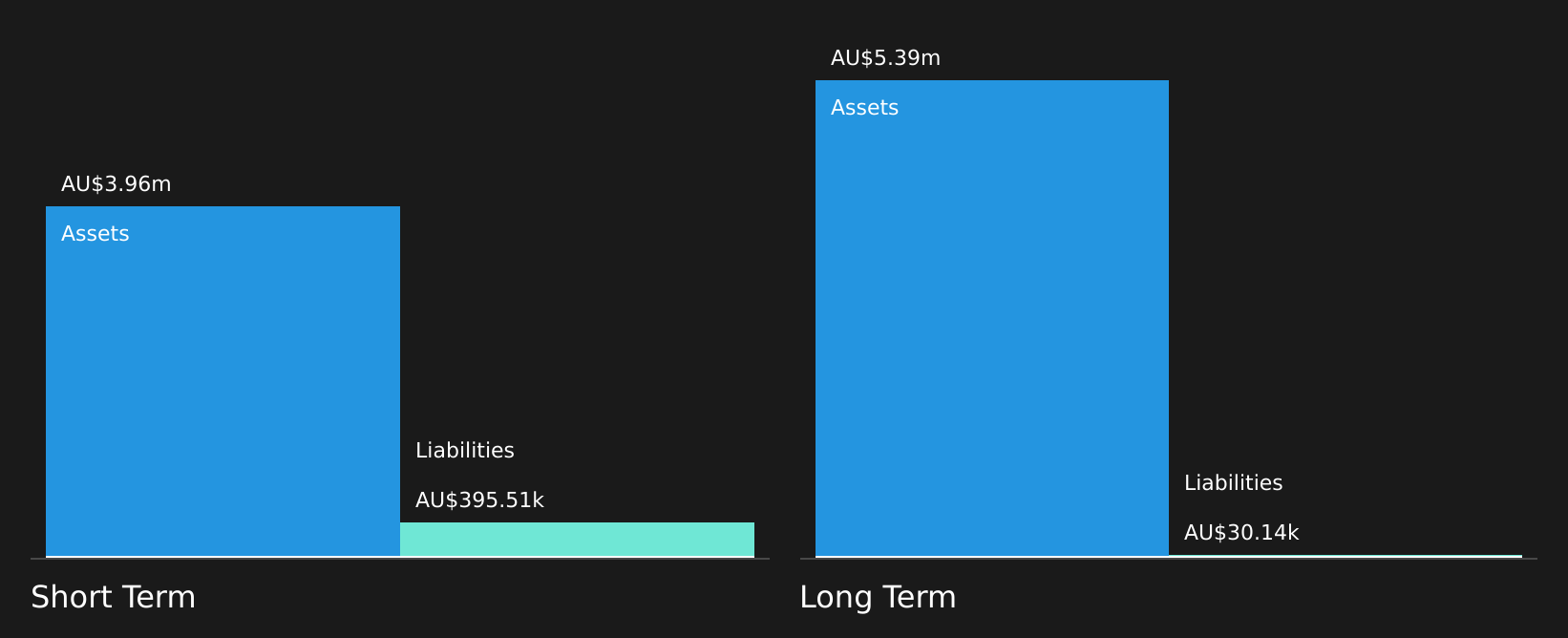

Regal Partners Limited, with a market cap of A$1.21 billion, demonstrates financial stability through its strong asset position, as short-term assets surpass both short and long-term liabilities. The company has more cash than total debt and its operating cash flow significantly covers debt obligations. Despite a low return on equity at 5.1% and declining profit margins from 28.1% to 17.2%, the company is trading below estimated fair value by 17.5%. Recent inclusion in the S&P/ASX Small Ordinaries and ASX 300 indices reflects growing recognition within the market, although insider selling has been significant recently.

- Navigate through the intricacies of Regal Partners with our comprehensive balance sheet health report here.

- Gain insights into Regal Partners' outlook and expected performance with our report on the company's earnings estimates.

Key Takeaways

- Dive into all 424 of the ASX Penny Stocks we have identified here.

- Searching for a Fresh Perspective? Trump's oil boom is here — pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com