Is Ferrari’s Soaring Share Price Justified After Five Years of Triple-Digit Gains?

Thinking about what to do next with Ferrari stock? You are not alone. With a last close at $426.9 and the company’s shares up 3.9% over the past week, it is no wonder investors are taking notice. Even more impressive, the stock has soared 132.3% over the past three years and an incredible 181.3% over five years. Those kinds of moves are hard to ignore, even if gains in the past month and year have been closer to 2.0% and 4.9%.

So what is behind these numbers? Much of Ferrari’s performance lately has been linked to shifts in market sentiment as investors see luxury brands and iconic names like Ferrari as a unique mix of growth and resilience. Factors like evolving consumer preferences in luxury markets and positive momentum in global equities have kept risk appetites high. But with strong long-term returns, a big question remains: how does all this translate into fair value today?

If you are looking at hard numbers, Ferrari’s valuation score stands at 0 out of 6, meaning it does not come up as undervalued by any of the six checks analysts like to use. That might raise some eyebrows, but valuation is more than just a checklist. In the next section, we will break down what those typical valuation approaches reveal. And by the end, you will see why understanding Ferrari’s true worth may take one more step beyond the usual methods.

Ferrari scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ferrari Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates what a company is really worth by projecting its future cash flows and discounting those sums back to today’s value. For Ferrari, this means looking at how much cash the business is expected to generate each year and then calculating how much that future money is actually worth right now.

Currently, Ferrari’s Free Cash Flow (FCF) stands at approximately €1.3 billion. Analyst projections show steady growth, with FCF expected to reach about €1.8 billion by the end of 2029. While analysts typically only forecast up to five years ahead, further estimates through 2035 are extrapolated, offering a longer-term view of the business’s cash-generating power in the luxury auto market.

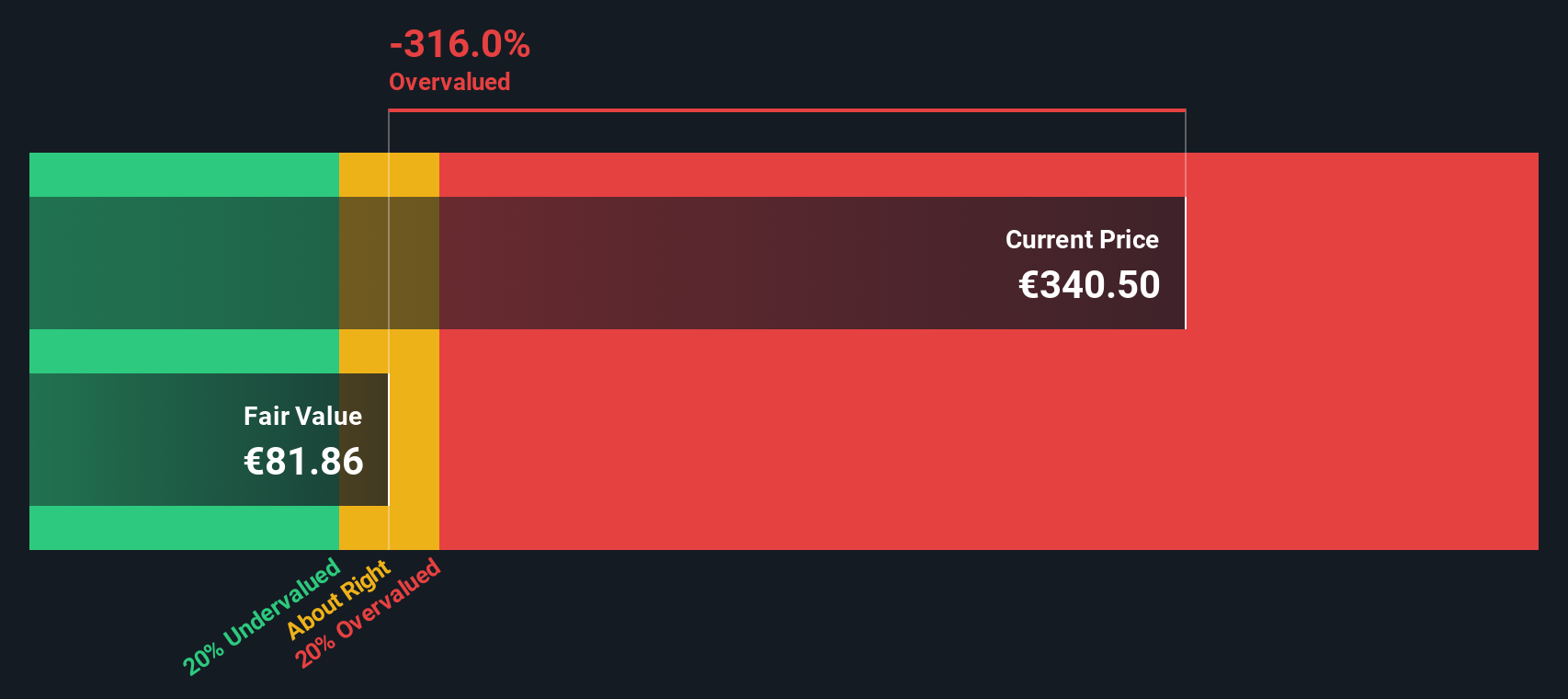

Based on these cash flow projections, the DCF model calculates an intrinsic value of just €75.48 per share. With the current share price at €426.90, this suggests Ferrari stock is trading at a significant premium, roughly 465.6% above its estimated fair value according to this method.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ferrari may be overvalued by 465.6%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Ferrari Price vs Earnings

For profitable companies like Ferrari, the Price-to-Earnings (PE) ratio is often the go-to valuation metric. This ratio tells us how much investors are paying for each euro of the company's profits, which is especially relevant for established firms with predictable earnings.

What makes a “normal” or “fair” PE ratio depends on how fast a company is expected to grow and the risks it faces. High-growth, well-known brands like Ferrari often command higher multiples. In contrast, slower-growing or riskier companies usually trade at lower ones.

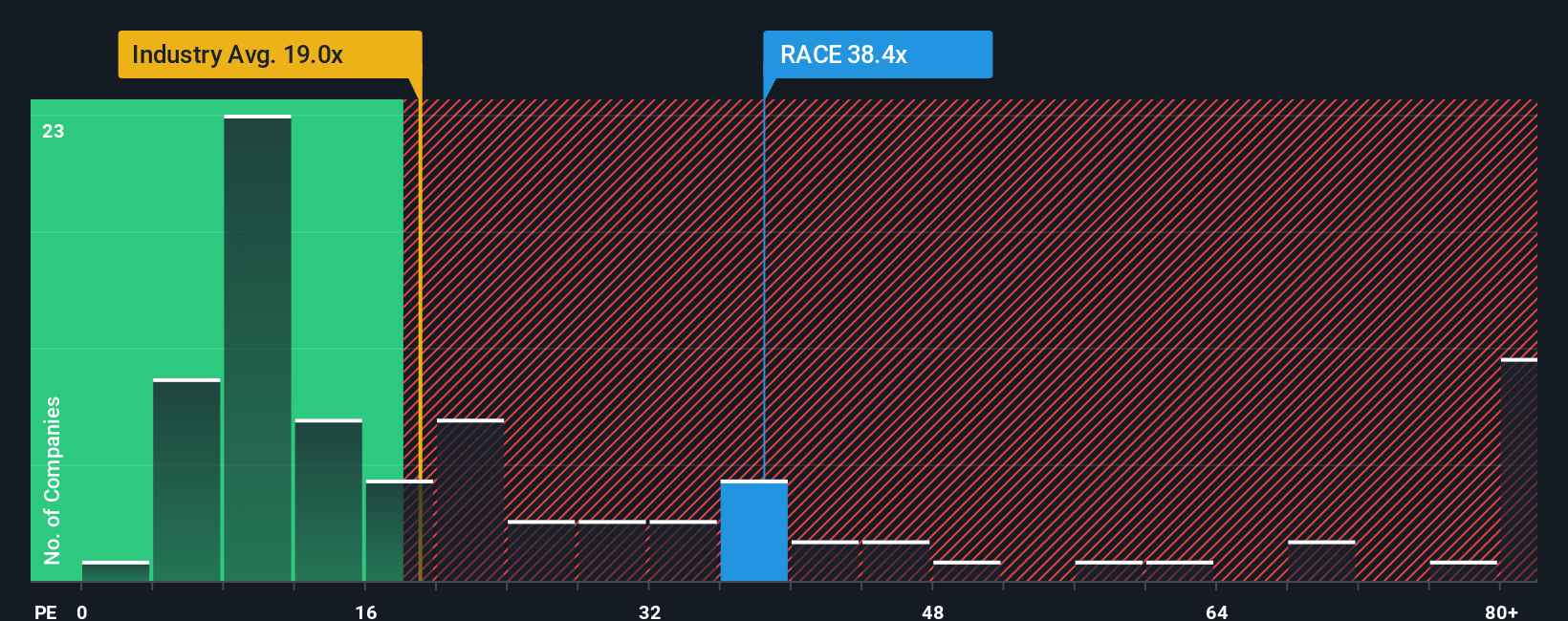

Currently, Ferrari’s PE ratio stands at 47.6x. That is well above the auto industry average of 18.0x and also higher than the average for its peers at 14.5x. On the surface, this makes Ferrari look expensive. However, not all companies grow at the same rate or have the same market positioning, so a simple industry comparison can be misleading.

This is where Simply Wall St’s proprietary “Fair Ratio” comes in. The Fair Ratio for Ferrari is calculated at 20.2x, which takes into account its earnings growth outlook, high profit margins, its size, and even the risks it faces. Unlike basic peer or industry averages, the Fair Ratio adjusts for unique qualities and gives a more tailored view of what Ferrari should be worth right now.

Since Ferrari is trading at a 47.6x PE, well above its Fair Ratio of 20.2x, this approach also suggests the stock is overvalued by this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ferrari Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your own story about Ferrari’s future, connecting the company’s strategy and prospects with your assumptions about its future revenue, earnings, and fair value. It is not just what the numbers say now, but why you think they could change.

Narratives make investing more personal and practical by letting you link your outlook on Ferrari’s electrification plans, global demand, and brand power directly to a financial forecast and a calculation of fair value. On Simply Wall St’s Community page, millions of investors are already using Narratives as a dynamic tool to see how their perspective stacks up against the market. There is also the ability to instantly compare the Fair Value generated by their story to the current share price.

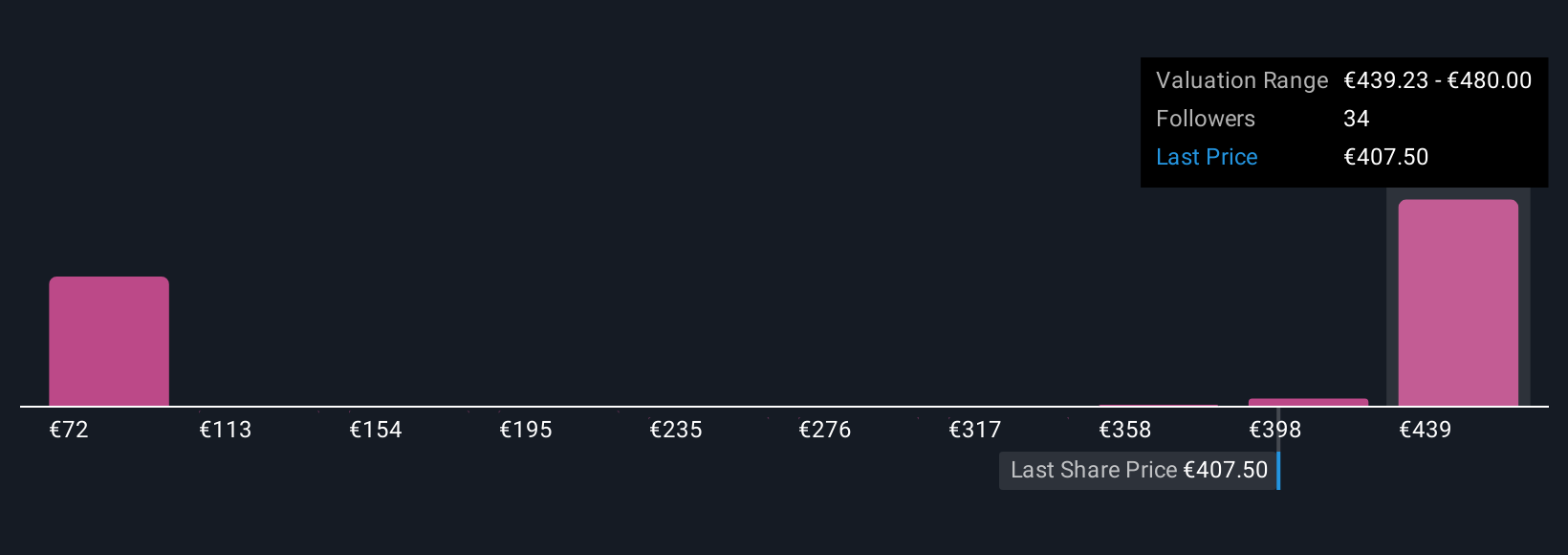

Because Narratives update with every new earnings result or important news headline, they keep your decisions relevant and grounded as the facts change. For example, some see Ferrari’s electrification strategy, pricing power, and order backlog as signs that its fair value could be as high as €548, while others are more cautious, estimating only €380 based on long-term risks and evolving luxury trends.

Do you think there's more to the story for Ferrari? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com