Assessing CAVA Stock After a 50% Drop and Recent Double-Digit Bounce in 2025

If you are wondering what to make of CAVA Group stock after a wild twelve months, you are not alone. CAVA’s share price has had a rollercoaster ride, with an impressive 8.1% rebound in the last week standing out against a much rougher longer-term picture. The stock is still down nearly 45% year-to-date and has tumbled close to 50% over the past year. For anyone trying to figure out if now is the moment to buy, hold, or steer clear, these swings highlight how investor sentiment keeps shifting, often with little warning.

Why such dramatic moves? Much of the action has been tied to sentiment shifts around the entire fast-casual dining space, as well as broader anxieties in the consumer sector. While none of the recent market developments directly explain every jump or dip, it is clear that risk perception surrounding CAVA has increased, even as the company itself continues to grow awareness and footprint among consumers.

So, where does valuation stand now? On a scale where 1 means undervalued in just one of six valuation checks, CAVA currently scores a 1. At least by the numbers, there may be fewer bargains here than growth investors hope for. Still, traditional valuation models only tell part of the story. Here is a look at the key approaches to valuing CAVA Group stock and, at the end, a more nuanced way to consider what the market might be missing.

CAVA Group scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

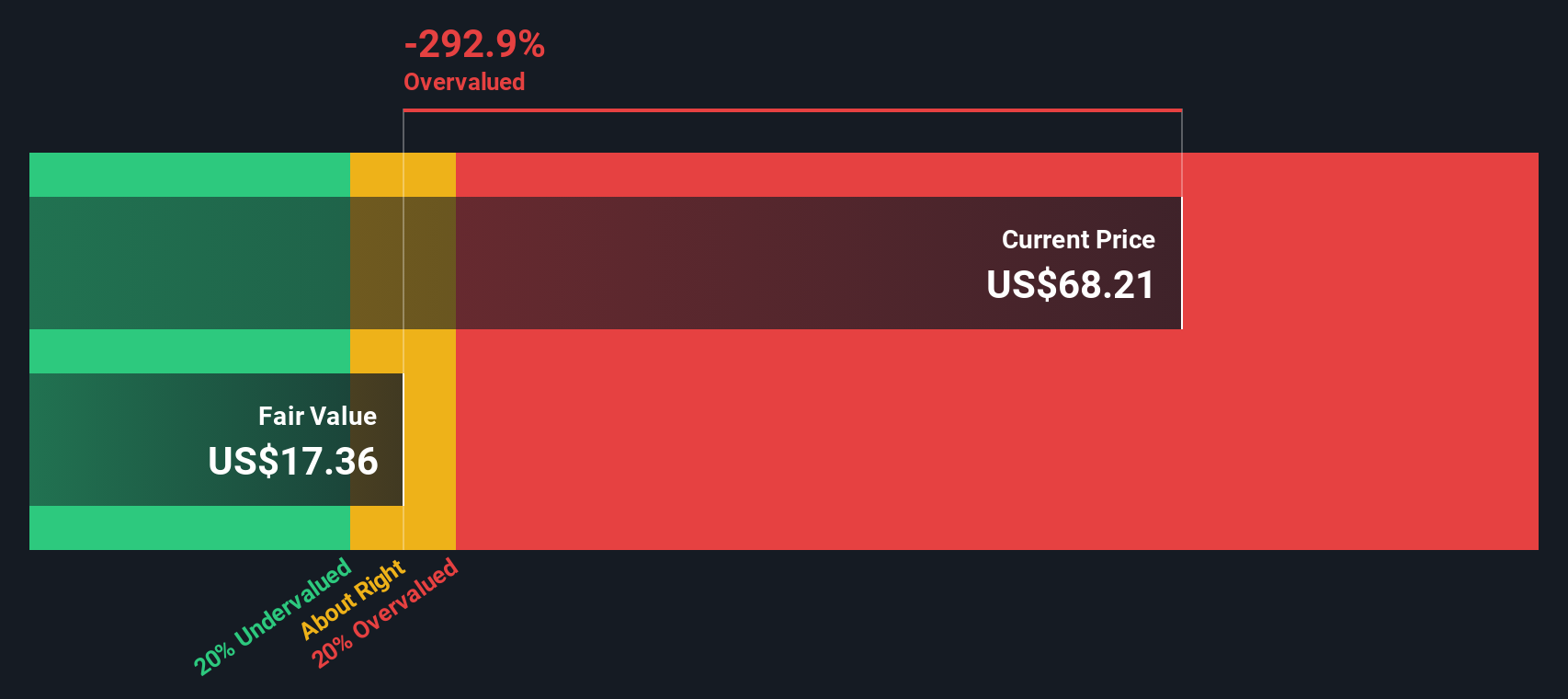

Approach 1: CAVA Group Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to their present value. This approach focuses on what the business is expected to generate in Free Cash Flow (FCF) over the next several years.

For CAVA Group, the most recent $11.5 million in Free Cash Flow sets the starting point. Analysts provide forecasts for the next five years, and according to these projections, the company’s FCF could grow rapidly, reaching as high as $160.9 million by 2029. After that, estimates rely on extrapolation based on historical growth rates.

When all those future cash flows are discounted back, the DCF model gives an intrinsic value of $30.06 per share. However, this is notably lower than the current market price, implying the stock is about 111.3% overvalued based on these cash flow projections alone.

Put simply, while the company may show promise, the DCF model suggests that CAVA Group’s current price bakes in a lot more optimism than the earnings or cash flows justify today.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CAVA Group may be overvalued by 111.3%. Find undervalued stocks or create your own screener to find better value opportunities.

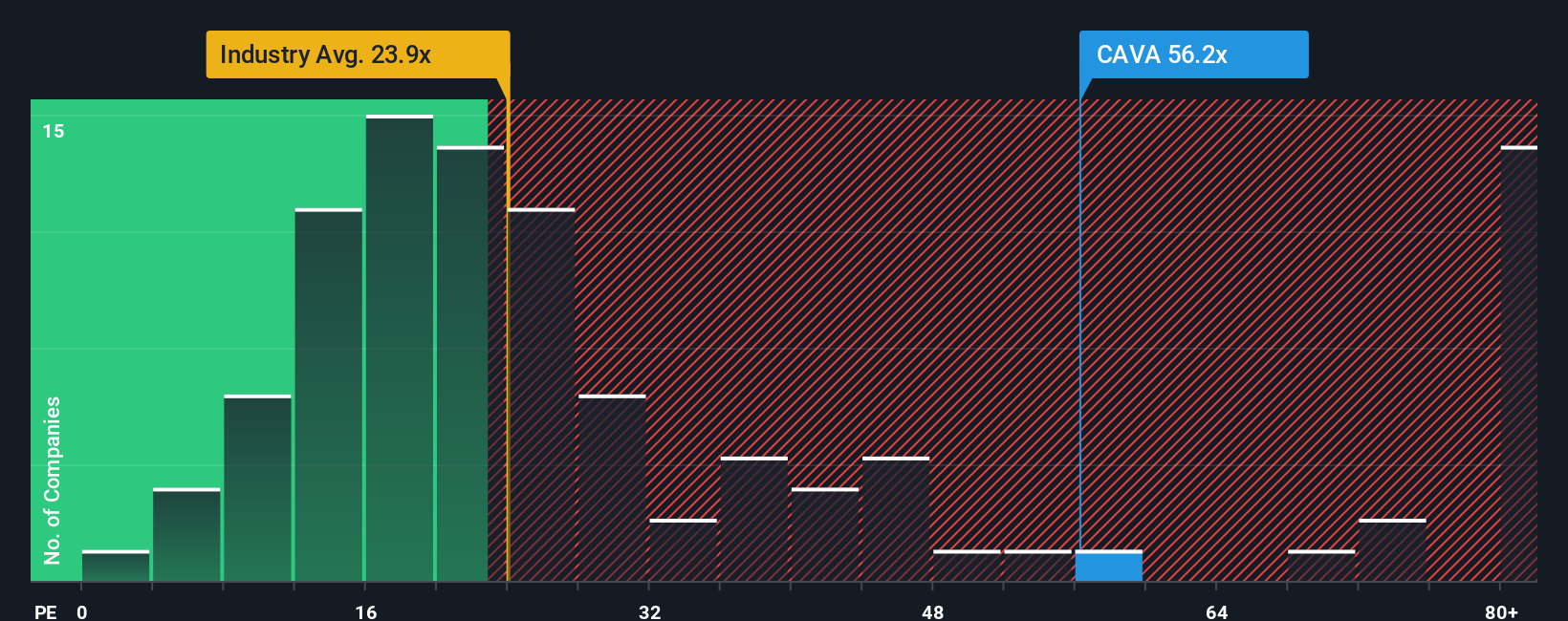

Approach 2: CAVA Group Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation tool for profitable companies, as it helps investors assess how much they are paying for a company's earnings. The underlying idea is simple: the PE ratio tells you how many dollars investors are willing to pay today for each dollar of current earnings.

That said, what counts as a "normal" or "fair" PE ratio depends not just on the company's sector, but on its growth prospects and risk profile. High-growth companies can command higher PE ratios since investors are willing to pay more for future potential, while companies facing uncertainty often see lower ratios.

Currently, CAVA Group trades at a PE ratio of 52.4x. This stands well above the Hospitality industry average of 24.4x and also outpaces the peer average of 48.3x. At first glance, this premium might raise eyebrows; however, context matters.

This is where Simply Wall St’s "Fair Ratio" comes in. The Fair Ratio is a proprietary benchmark that adjusts the PE multiple based on a company’s specific earnings growth outlook, risk factors, profit margins, industry type, and size. Unlike blunt comparisons to industry or peer averages, the Fair Ratio offers a much more tailored and holistic sense of value.

According to this approach, CAVA’s Fair Ratio is 21.6x. With the current PE ratio more than doubling this benchmark, the stock looks expensive even after accounting for its growth story and industry position.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CAVA Group Narrative

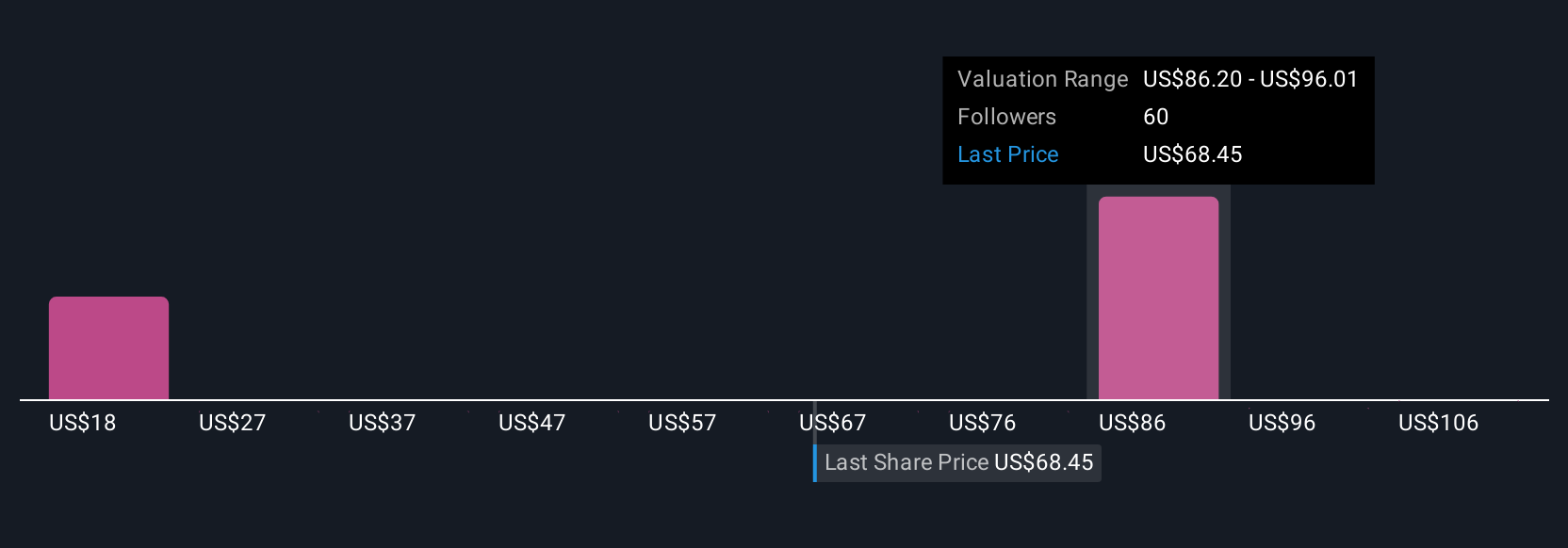

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is simply your story or perspective about CAVA Group’s future, connecting what you believe about its business growth, strategy, and risks with what those beliefs mean for its financial forecasts and fair value.

Instead of relying just on numbers and ratios, Narratives allow you to anchor your investment decisions to a company’s underlying story. This makes it easy to see how your assumptions translate into actual estimates of earnings, revenue, margins, and ultimately a fair value for the stock.

On Simply Wall St’s Community page, used by millions of investors, Narratives are an accessible tool that shows you how your view compares to others. They update automatically as new news or earnings information is released.

Narratives help you decide when to buy or sell by letting you compare your Fair Value to the current share price and adapt your stance in real time as new developments occur.

For example, some investors set optimistic Narratives for CAVA, assigning a fair value as high as $125 based on aggressive expansion and margin improvement. Others are more cautious, seeing more risk and a fair value closer to $72.

Do you think there's more to the story for CAVA Group? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com