NGEx Minerals (TSX:NGEX): Valuation Insights After Upsized C$175M Placement and Strategic Project Funding

NGEx Minerals (TSX:NGEX) is making waves after announcing an upsized private placement that will raise C$175 million. This move is driven by exceptionally strong demand and significant participation from the Lundin Family Trusts.

See our latest analysis for NGEx Minerals.

Recent news of the C$175 million placement comes shortly after NGEx Minerals unveiled a major drill campaign at its flagship Lunahuasi project. The market has responded to this wave of activity by nudging the share price up to $26.51. The past year’s 1.3% total shareholder return shows steady momentum, while over the past five years, NGEx has delivered a 47% total return. This reflects investors’ growing confidence in its expanding project pipeline and revamped capital position.

If this surge of exploration and investor interest has you thinking bigger, consider broadening your search and discover fast growing stocks with high insider ownership

With this capital in hand, NGEx Minerals is arguably better positioned than ever. Yet with shares now trading just below analyst targets after a sharp run-up, is there still an untapped buying opportunity here, or have markets already priced in the next leg of growth?

Price-to-Book of 38.2x: Is it justified?

NGEx Minerals is currently trading at a price-to-book (P/B) ratio of 38.2x, a substantial premium compared to both the industry and its peers. The recent closing price of CA$26.51 places the company well above the Canadian Metals and Mining industry average of 2.6x and the peer average of 2.8x. This raises sharp questions about whether this level is warranted.

The price-to-book ratio reflects how much investors are willing to pay today for each dollar of net assets. For mining and exploration companies like NGEx, high ratios often signal expectations for significant future discoveries, resource upgrades, or transformational events that have not yet been captured in reported book value.

At 38.2x book, NGEx’s valuation is notably aggressive. The market is effectively factoring in a bullish scenario for future project success, particularly given the company's current lack of revenue and ongoing losses. Compared to traditional industry and peer averages, this figure puts NGEx in the uppermost echelon of price-to-book multiples. It suggests the market is assigning a sizeable premium for its exploration pipeline and management pedigree.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 38.2x (OVERVALUED)

However, ongoing revenue absence and persistent net losses could challenge the bullish case if exploration milestones are delayed or if market sentiment shifts abruptly.

Find out about the key risks to this NGEx Minerals narrative.

Another View: SWS DCF Model Offers a Different Angle

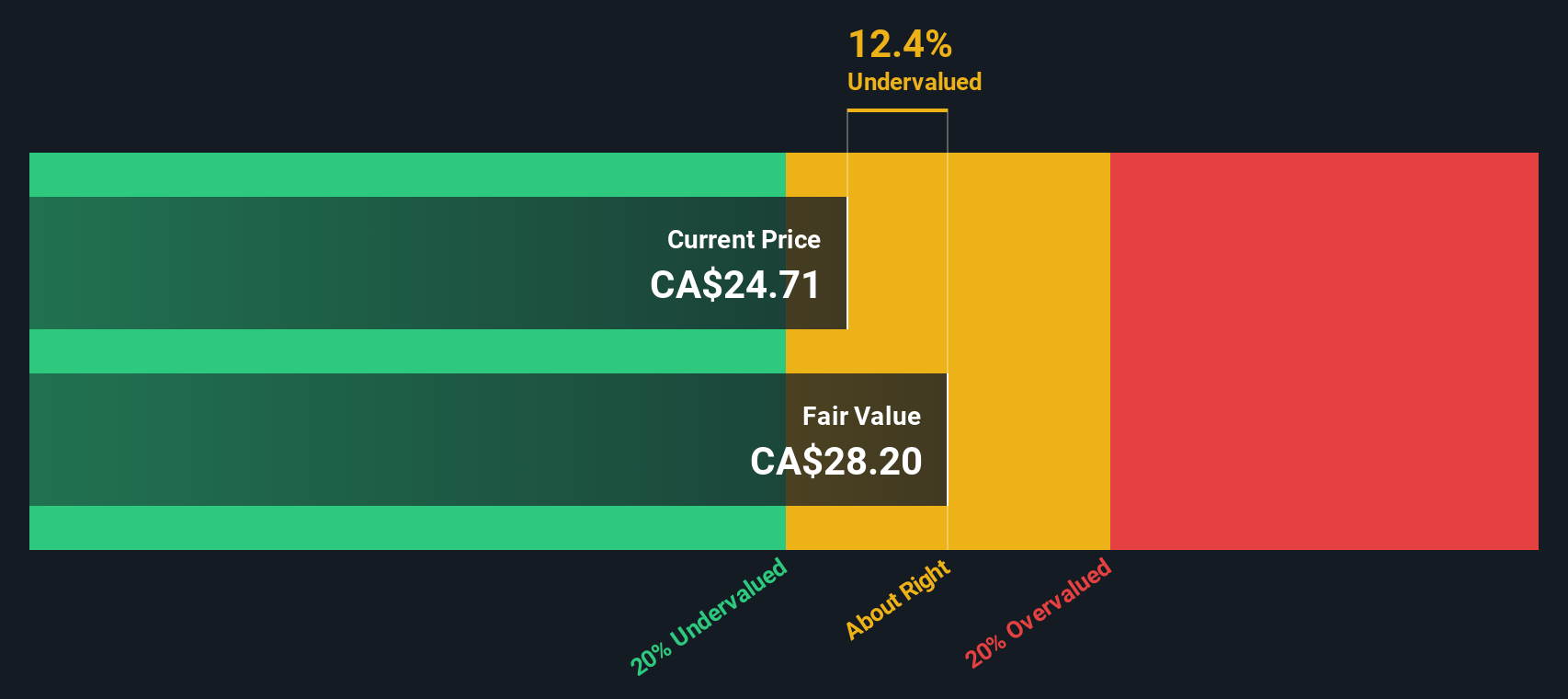

While the sky-high price-to-book ratio might suggest NGEx Minerals is overvalued, our DCF model offers a slightly different perspective. Based on future cash flow estimates, the shares are currently trading about 7.6% below our calculated fair value. This indicates the stock may actually be undervalued from this point of view.

Look into how the SWS DCF model arrives at its fair value.

This disparity between market optimism and DCF-based caution leaves investors with a classic valuation puzzle. Which perspective will prove more accurate as NGEx’s story unfolds?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NGEx Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own NGEx Minerals Narrative

If this analysis doesn’t fully line up with your own perspective, or if you’d prefer to examine the numbers yourself, creating your personal view is just a few minutes away: Do it your way

A great starting point for your NGEx Minerals research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for More Smart Investment Moves?

Supercharge your portfolio with unique stock ideas that you might have missed. Take action now and open the door to promising opportunities beyond NGEx Minerals.

- Catch powerful momentum by targeting these 886 undervalued stocks based on cash flows that trade below their cash flow-based valuations and could be poised for upside.

- Harvest consistent income by focusing on these 19 dividend stocks with yields > 3% offering attractive yields above 3%, perfect for strengthening your portfolio’s payout potential.

- Position yourself early in groundbreaking tech with these 26 quantum computing stocks shaping the next wave of innovation in computing and security.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com