Should UPS's (UPS) Shift to Higher-Margin Clients Signal a New Approach to Dividend Sustainability?

- In recent days, United Parcel Service has accelerated cost-cutting efforts and shifted focus toward higher-margin customers, even while facing concerns about meeting long-term targets and the sustainability of its dividend.

- Market observers have questioned the company's dividend resilience, interpreting the elevated yield as a warning sign for investors amid industry overcapacity and tariff uncertainty.

- We'll now explore how ongoing debate around UPS's dividend and revised business priorities could shape its future investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

United Parcel Service Investment Narrative Recap

To be a shareholder in United Parcel Service right now, you need to believe UPS can successfully pivot its business model toward higher-margin customers and maintain its capital return commitments, even as it faces questions over revenue growth and dividend sustainability. The most important short-term catalyst remains the company’s ability to execute cost cuts without significantly disrupting operations, while the biggest risk is whether ongoing margin pressure and falling volumes force a dividend reduction in the near term, recent news has heightened, not lessened, this risk.

Of the recent company developments, the confirmation of UPS’s scheduled quarterly dividend payout of US$1.64 per share stands out. This announcement has direct relevance as it reflects management’s attempts to reassure investors even as market sentiment grows concerned that current cash flows may not be enough to sustain the dividend if current business pressures persist. Investors are closely watching such measures as the debate over payout sustainability unfolds.

By contrast, investors should be equally mindful of…

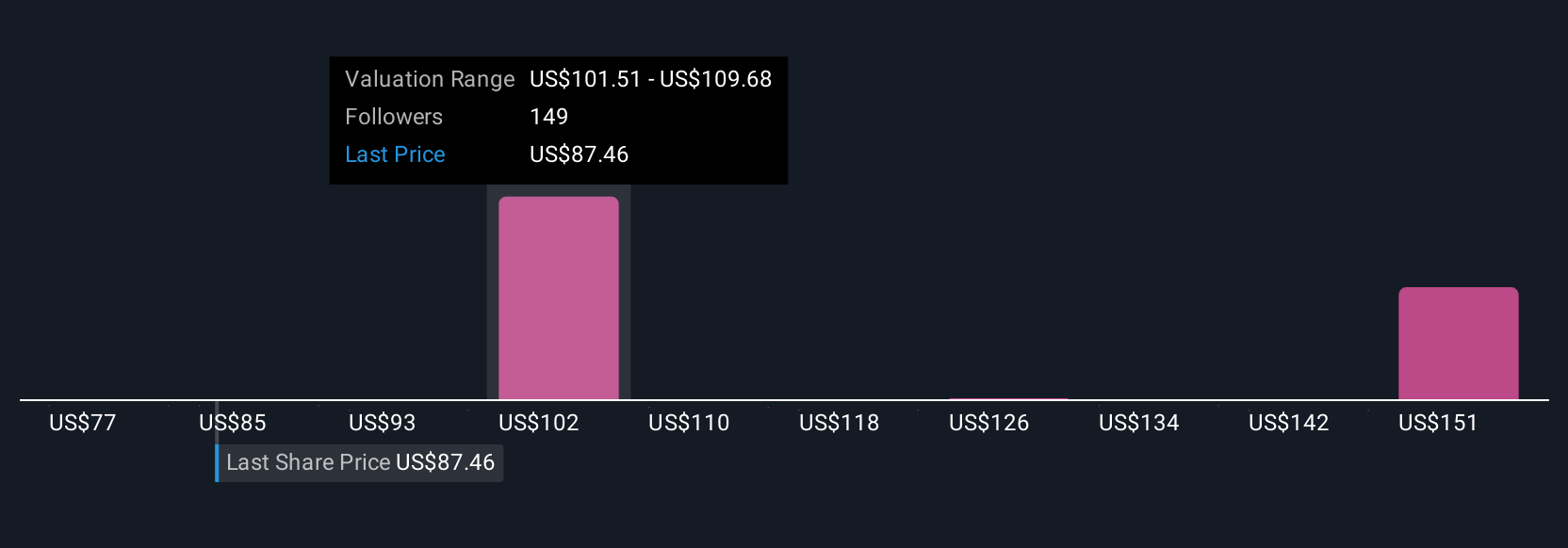

Read the full narrative on United Parcel Service (it's free!)

United Parcel Service's outlook anticipates $94.5 billion in revenue and $7.1 billion in earnings by 2028. This is based on a projected annual revenue growth rate of 1.5% and a $1.4 billion increase in earnings from the current $5.7 billion.

Uncover how United Parcel Service's forecasts yield a $101.43 fair value, a 17% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts were expecting UPS earnings to reach US$8,000,000,000 by 2028, painting a picture of strong growth led by faster automation and global route expansion. If you see risks differently, like the threat from tech-driven competitors taking market share, remember that these varied forecasts show just how much investor opinions can differ, especially as recent developments could reshape even the most bullish outlooks.

Explore 27 other fair value estimates on United Parcel Service - why the stock might be worth as much as 88% more than the current price!

Build Your Own United Parcel Service Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United Parcel Service research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United Parcel Service research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Parcel Service's overall financial health at a glance.

No Opportunity In United Parcel Service?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com