Mitsubishi Chemical Group (TSE:4188): Evaluating Valuation as Shares Consolidate and Forecasts Diverge

Mitsubishi Chemical Group (TSE:4188) shares have moved little in recent sessions. This has encouraged some investors to look beyond the headlines and reexamine the company’s latest financials and longer-term performance trends.

See our latest analysis for Mitsubishi Chemical Group.

Although Mitsubishi Chemical Group’s share price has barely budged in recent sessions, its longer-term story tells more. While the 1-year total shareholder return is essentially flat, the 3- and 5-year metrics show meaningful gains for investors confident enough to hold through volatility.

If you’re looking for fresh ideas beyond chemicals and materials, now’s the perfect moment to widen your search and discover fast growing stocks with high insider ownership

With shares trading at a notable discount to analyst targets and the company posting improving earnings, the question arises: Is Mitsubishi Chemical Group currently undervalued, or is the market already factoring in its future growth prospects?

Most Popular Narrative: 7.6% Undervalued

While Mitsubishi Chemical Group’s latest close of ¥835.8 sits below the narrative’s fair value estimate of ¥905, the valuation hinges on future earnings growth and profit margin improvements that only a few companies in the sector have managed to deliver.

Rising demand for display-related, semiconductor, and barrier packaging materials, directly tied to trends like electric vehicle proliferation and technology hardware growth, is already outpacing initial forecasts and is expected to contribute robustly to revenue and profit growth in upcoming periods.

Which bold assumptions power this outlook? The most popular narrative leverages high demand drivers and bets on substantial margin jumps. Ready to uncover the forecasted financials behind this bullish target? Click to see what is fueling Mitsubishi Chemical Group’s projected turnaround.

Result: Fair Value of ¥905 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent oversupply in core markets or delays in executing business shifts could pose specific challenges to Mitsubishi Chemical Group’s optimistic turnaround expectations.

Find out about the key risks to this Mitsubishi Chemical Group narrative.

Another View: P/E Ratio Signals Caution

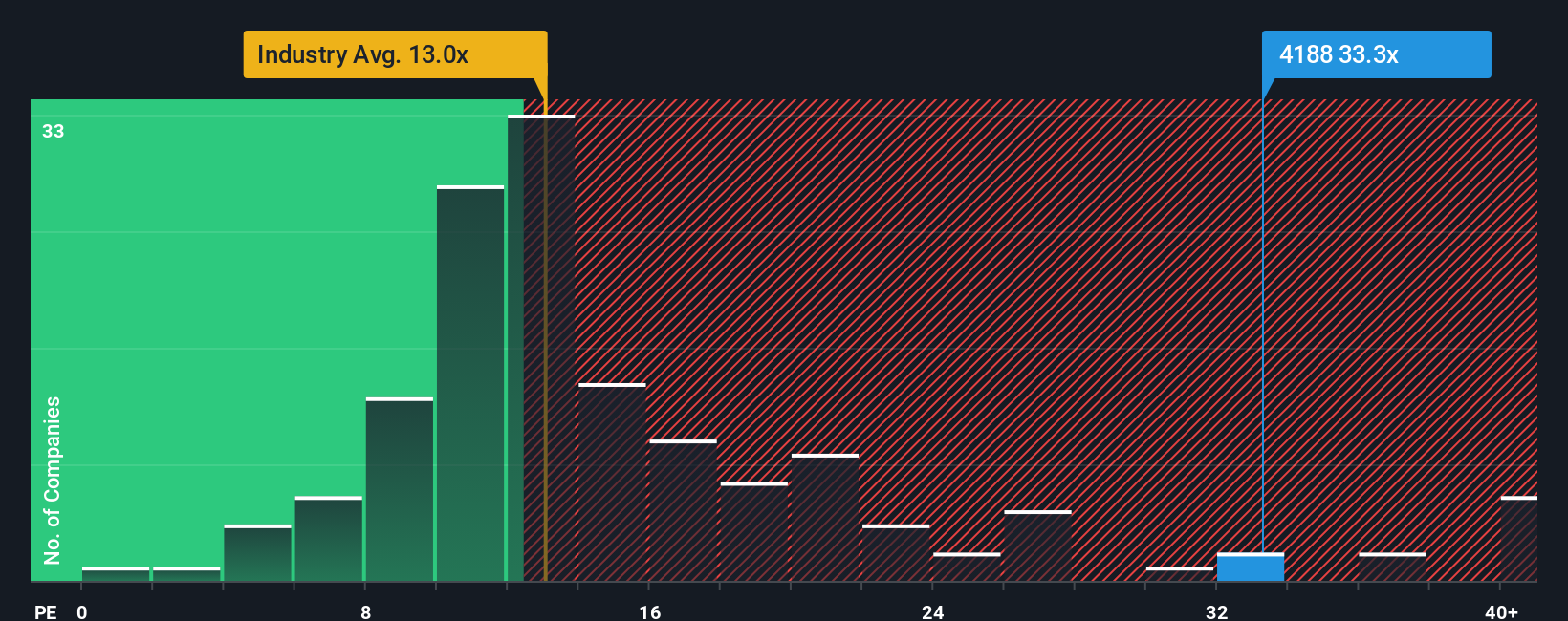

Looking at Mitsubishi Chemical Group’s valuation through its price-to-earnings ratio offers a different perspective compared to the fair value estimate. The stock trades at 31.4 times earnings, which is significantly higher than the Chemicals industry average of 12.6 times and even its fair ratio of 21.3 times. This substantial gap could expose investors to valuation risk if market sentiment changes or if earnings fall short of expectations. Can the company justify this premium, or will reality catch up?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Mitsubishi Chemical Group Narrative

If you see the numbers differently or want a hands-on approach to the story, dive in and shape your own perspective. It takes just minutes to create your own. Do it your way

A great starting point for your Mitsubishi Chemical Group research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let a single stock define your portfolio. Level up your investing by tapping into untapped opportunities tailored just for forward-thinking investors like you.

- Uncover high-yield opportunities and get ahead of the curve with these 19 dividend stocks with yields > 3%, offering reliable income streams above 3%.

- Target the next technology disruptors shaping tomorrow by tracking momentum in these 24 AI penny stocks.

- Strengthen your strategy by identifying value picks with long-term upside through these 896 undervalued stocks based on cash flows, all based on thorough cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com