Firefly Aerospace (FLY): Valuation in Focus After Rocket Test Failure and Sharply Lower Share Price

Firefly Aerospace (FLY) is under the microscope after its Alpha Flight 7 rocket exploded during a preflight test. This incident sent shares tumbling and intensified investor unease about the company’s reliability and commercial future.

See our latest analysis for Firefly Aerospace.

Shares of Firefly Aerospace rallied after its August IPO but quickly lost altitude, with the 30-day share price return slipping and investor sentiment cooling in the wake of its Alpha rocket mishap and disappointing quarterly results. Despite headline-grabbing NASA contract wins and a recent S&P TMI Index addition, the momentum has faded as risk perceptions rise and the company’s early promise faces real world setbacks.

Amid these turbulent launches and shifting momentum, it could be the perfect time to see which other aerospace innovators are on investors’ radar. See the full list for free.

With shares now trading at a sharp discount to analyst targets after disappointing results and rocket setbacks, is the market overlooking Firefly's long-term potential, or is all of the risk already priced in?

Price-to-Sales Ratio of 38.2x: Is it justified?

Firefly Aerospace is trading at a price-to-sales ratio of 38.2x, placing the stock at a sharp premium compared to both its direct peers and the broader US Aerospace & Defense sector.

The price-to-sales (P/S) ratio compares the company’s stock price to its revenues. This metric is especially relevant for early-stage aerospace firms that may not yet be profitable, as it helps investors gauge expectations for future revenue growth relative to what the market is willing to pay today.

At 38.2x, Firefly’s ratio stands far above the US Aerospace & Defense industry average of 3.4x and also exceeds the peer group average of 2.7x. This steep multiple suggests the market is pricing in aggressive growth expectations or placing a premium on the company’s position in a high-potential but volatile market segment.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Sales ratio of 38.2x (OVERVALUED)

However, persistent revenue losses and recent share price declines could further erode investor confidence if commercial growth targets are not met soon.

Find out about the key risks to this Firefly Aerospace narrative.

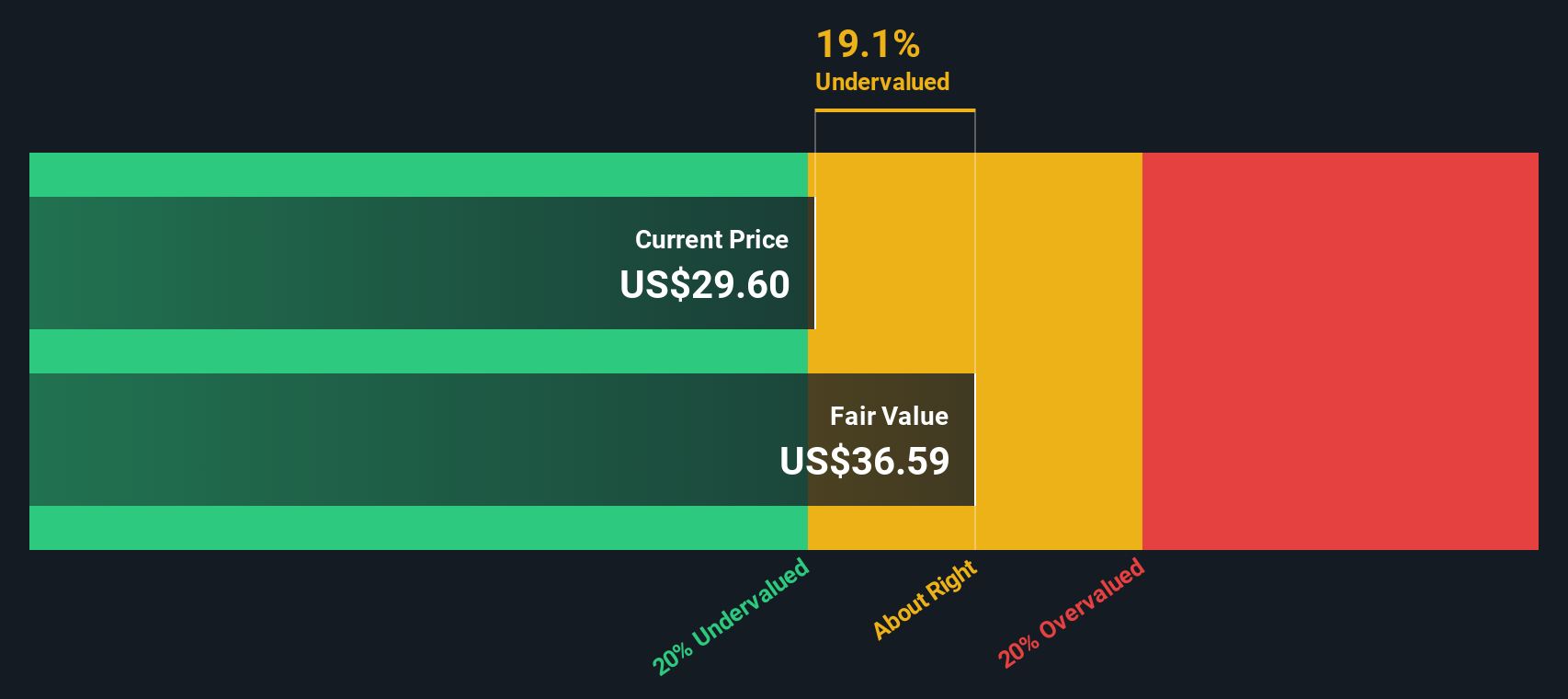

Another View: What Does Our DCF Model Say?

Looking at the SWS DCF model provides a very different perspective. Firefly Aerospace’s shares are trading at $26.80, which is about 27.4% below our estimate of fair value at $36.92. In this view, the stock appears undervalued by the market right now.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Firefly Aerospace for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Firefly Aerospace Narrative

If you want to see things from a different angle or dive deeper into the numbers yourself, you can quickly build your own view of Firefly's story. Do it your way

A great starting point for your Firefly Aerospace research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t sit on the sidelines while others seize emerging opportunities. Use these expert-vetted stock lists to hone in on tomorrow’s potential market leaders right now.

- Capitalize on the wave of artificial intelligence with these 24 AI penny stocks, which are transforming industries and outpacing traditional competitors.

- Boost your portfolio’s income by targeting these 19 dividend stocks with yields > 3%, offering reliable yields and a solid track record in volatile markets.

- Take advantage of the rapidly growing universe of digital assets by assessing these 78 cryptocurrency and blockchain stocks, positioned at the forefront of financial innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com