Harmonic Drive Systems (TSE:6324): Is Robotics Growth Driving an Overvalued Stock?

Investor sentiment around Harmonic Drive Systems (TSE:6324) is building as the company strengthens its foothold in the humanoid robot sector and continues investing in industrial automation, even as it faces ongoing difficulties for its automotive clients such as Nissan Motor.

See our latest analysis for Harmonic Drive Systems.

Momentum is starting to pick up as Harmonic Drive Systems pivots toward robotics, despite a sluggish automotive sector. The 1-year total shareholder return is almost flat at -0.18%, which suggests the market is still weighing both the risks and the longer-term growth prospects.

If robotics innovation has your attention, consider broadening your search and discover See the full list for free.

With analyst targets still well above the current share price and momentum building in robotics, investors are left to wonder whether Harmonic Drive Systems offers hidden value at these levels or if the market has already accounted for future growth.

Price-to-Earnings of 68.7x: Is it justified?

Harmonic Drive Systems shares are currently trading at a price-to-earnings (P/E) ratio of 68.7x, which is well above both its peers and the wider JP Machinery sector. At a last close of ¥2,698, the stock commands a premium, reflecting high market expectations or potential optimism around future growth.

The price-to-earnings ratio measures how much investors are willing to pay today for each yen of company earnings. It is especially relevant for this sector as it helps gauge whether investor enthusiasm aligns with future profit potential in automation and robotics. In these industries, strong profit growth can sometimes justify higher multiples.

Harmonic Drive Systems is priced at a substantially higher multiple than the peer average (18.8x) and the JP Machinery industry average (13.2x). Compared to the estimated fair P/E of 41.1x, the current valuation appears stretched, signaling that the market may be factoring in robust growth prospects. However, the premium is significant and could adjust if expectations are not met.

Explore the SWS fair ratio for Harmonic Drive Systems

Result: Price-to-Earnings of 68.7x (OVERVALUED)

However, weaker long-term share returns and the possibility of growth expectations being revised down could still challenge the current optimism around Harmonic Drive Systems.

Find out about the key risks to this Harmonic Drive Systems narrative.

Another View: What Does the SWS DCF Model Suggest?

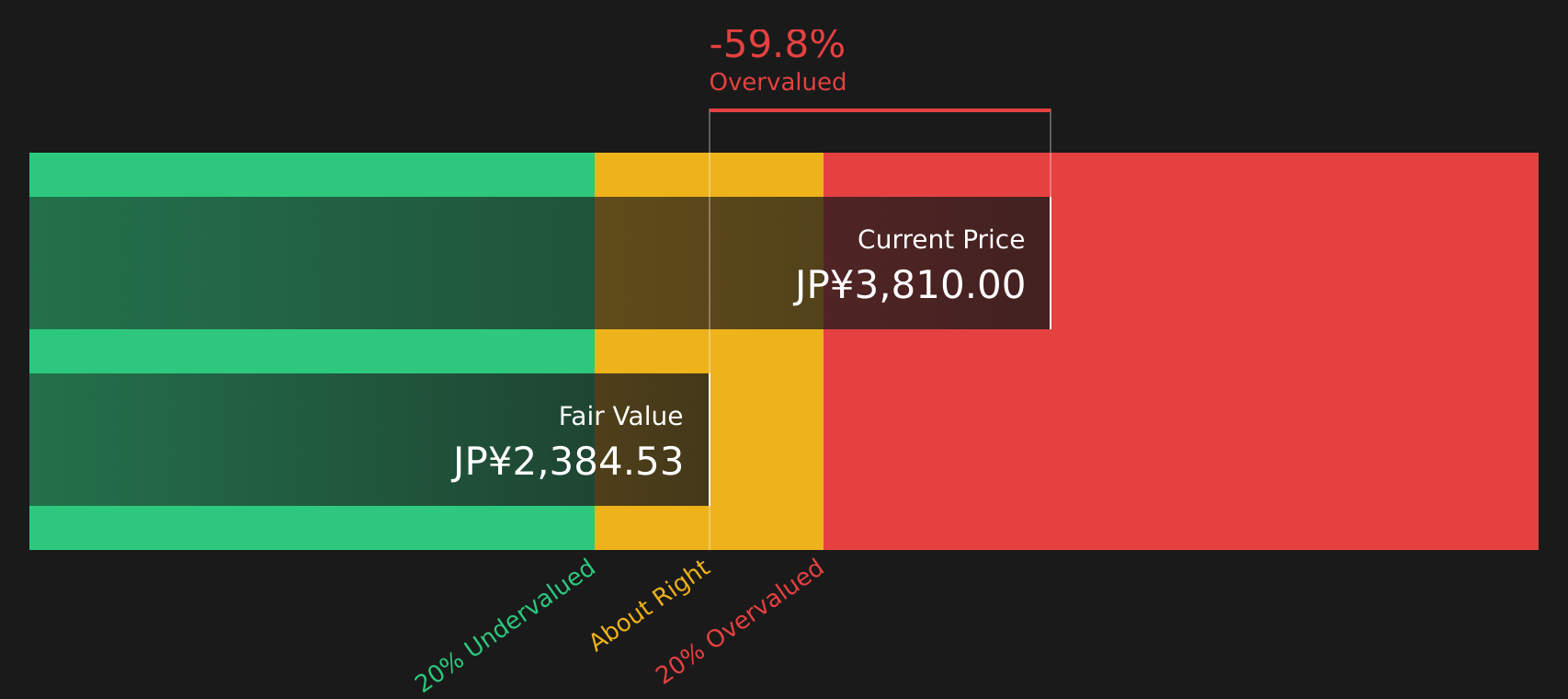

Looking from another angle, the SWS DCF model pegs Harmonic Drive Systems’ fair value at ¥1,553.61, well below its current share price of ¥2,698. This model indicates the stock may be overvalued, offering a clear contrast to the optimism reflected in earnings multiples. Is the market too hopeful, or is future growth being underestimated?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Harmonic Drive Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Harmonic Drive Systems Narrative

If you would rather form your own view or dig deeper into the numbers, it only takes a few minutes to assemble your own perspective. Do it your way.

A great starting point for your Harmonic Drive Systems research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

You could miss out if you stop here. There are even more smart opportunities waiting in the Simply Wall Street Screener, tailored for every kind of investor.

- Capitalize on rising healthcare breakthroughs by starting your search with these 31 healthcare AI stocks, where innovation meets long-term demand.

- Jump in on global digital trends and spot hidden winners through these 78 cryptocurrency and blockchain stocks, bringing you tomorrow’s blockchain and crypto leaders.

- Grow your passive income with ease by accessing these 19 dividend stocks with yields > 3%, spotlighting companies paying consistently strong yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com