Is Now the Right Moment for Hudbay Minerals After Its 75% Rally in 2025?

If you’ve been eyeing Hudbay Minerals lately, you’re not alone. The stock has been on a tear, gaining 10.8% in the last week, nearly 30% over the past month, and a jaw-dropping 75.9% so far this year. For longer-term holders, the returns are even more impressive, up over 270% in the past five years. These kinds of numbers grab attention and have led many investors to wonder if now is the time to get on board or if the run is getting ahead of itself.

The recent surge in Hudbay’s share price comes against the backdrop of positive market momentum in the mining sector and renewed interest in copper and base metals. Changes in risk perception, both at the company and sector level, have raised expectations for future growth, fueling much of the excitement you’re seeing in the share price today.

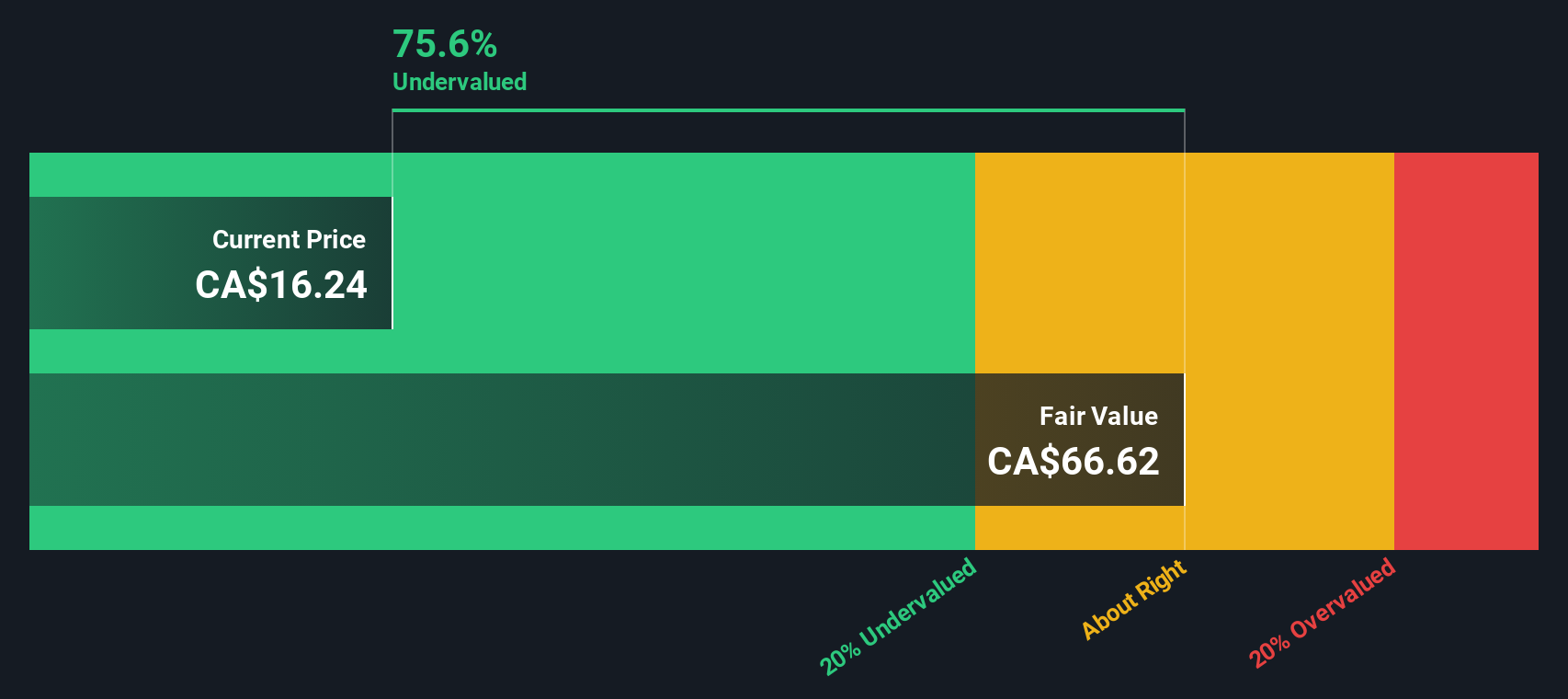

But what do these price moves mean from a value perspective? Hudbay scores a 5 out of 6 on our value score, one of the highest ratings among its peers. In other words, the company looks significantly undervalued across almost every metric we use to assess a stock’s true worth.

Curious about how we arrive at that score and what the numbers really mean for your portfolio? In the next section, we’ll break down Hudbay’s valuation using a range of proven approaches and hint at an even better way to judge value that most investors overlook.

Why Hudbay Minerals is lagging behind its peers

Approach 1: Hudbay Minerals Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates Hudbay Minerals’ true value by projecting future cash flows and discounting them back to today’s dollars. This method is based on the idea that a company’s worth is fundamentally tied to all the cash it can generate for shareholders in the years ahead.

Hudbay Minerals currently generates free cash flow of $360.7 million. Analysts forecast solid growth, with 2029 projections reaching $726 million. Beyond the analyst forecast window, cash flows are extrapolated to estimate performance up to a decade from now. These projections use a “2 Stage Free Cash Flow to Equity” approach, which captures both the near-term growth identified by analysts and longer-term trends anticipated by Simply Wall St.

According to the DCF analysis, the company’s intrinsic value is estimated at $64.32 per share. This is notable because the DCF-implied discount suggests the stock is trading about 66.5% below its calculated fair value. In other words, the current share price appears deeply undervalued based on long-term cash flow prospects.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hudbay Minerals is undervalued by 66.5%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

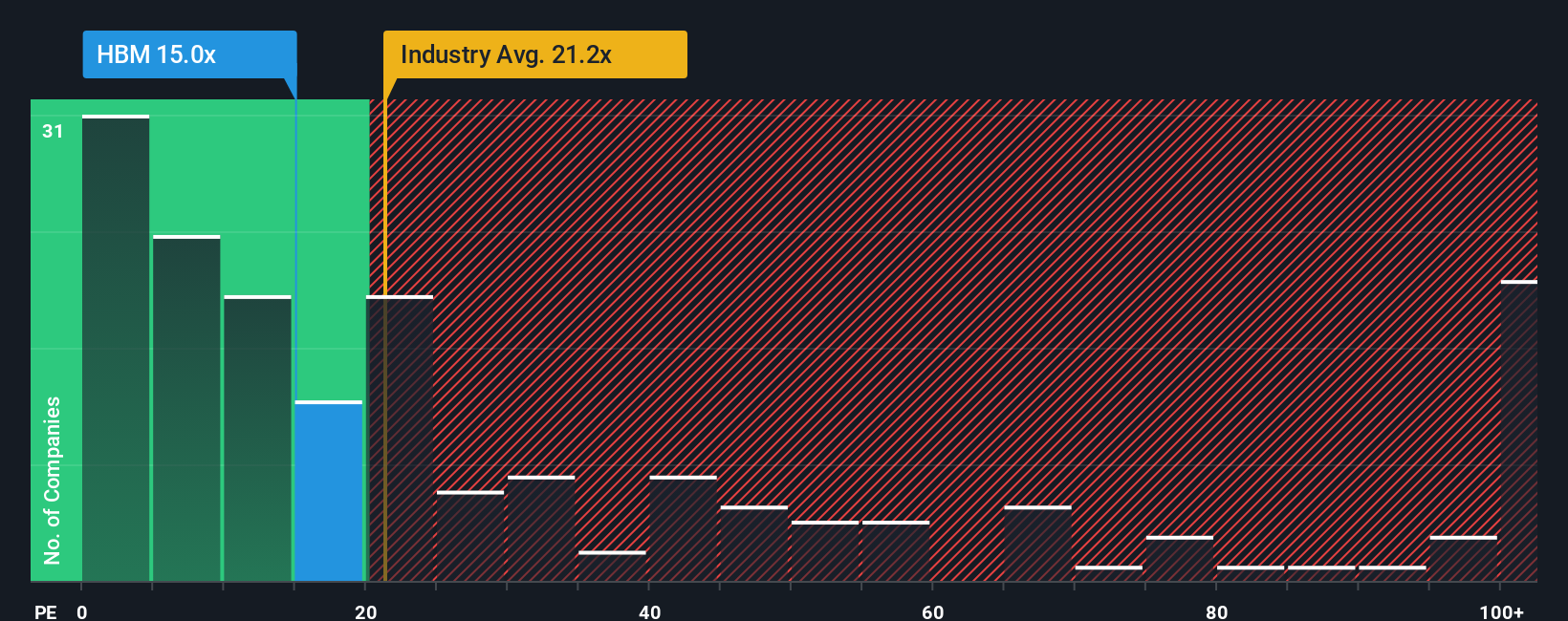

Approach 2: Hudbay Minerals Price vs Earnings (PE Ratio)

The Price-to-Earnings (PE) ratio is a widely used tool for valuing profitable companies like Hudbay Minerals because it directly relates the company’s market price to its actual earnings. When a company is generating steady profits, the PE ratio helps investors assess whether the stock is trading at a reasonable price relative to its earnings power.

It is important to remember that what is considered a “normal” or “fair” PE ratio can depend on factors such as expectations for future growth, as well as the perceived risks involved. Higher expected growth often justifies a higher PE, while higher risk can push that fair level down. For investors, this means it is crucial to interpret the ratio in context rather than in isolation.

Hudbay Minerals currently trades at a PE ratio of 21.2x. This is below both the industry average for metals and mining companies at 23.1x and its peer group average of 52.4x, making it look relatively inexpensive at first glance. Rather than relying solely on these broad comparisons, Simply Wall St uses a proprietary “Fair Ratio.” This fair PE ratio, in Hudbay’s case, is calculated as 21.9x and takes into account factors like its earnings growth prospects, profit margins, risk profile, industry benchmarks, and market capitalization. This dynamic approach provides a fuller picture of what the stock “should” be trading at today.

Comparing Hudbay’s actual PE ratio of 21.2x to its Fair Ratio of 21.9x, the stock appears fairly valued by this measure.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hudbay Minerals Narrative

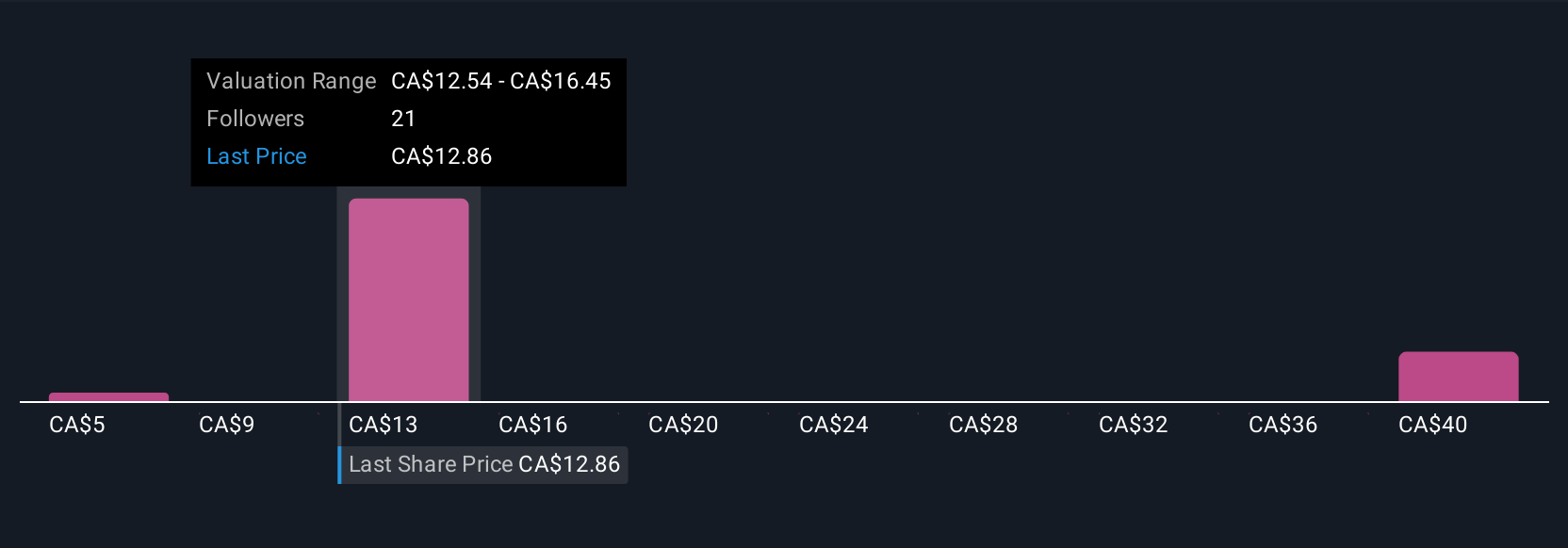

Earlier, we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple, yet powerful way for you to express your own story about a company, linking your expectations for future revenue, earnings, and margins to a fair value, all based on your unique viewpoint.

Narratives help bring the numbers to life by letting you build a picture of Hudbay Minerals’s future performance, then instantly see what those assumptions mean for fair value, right alongside the current price. This tool makes it clear when a stock might be under- or over-valued according to your thesis (not just consensus), and is easy to use on Simply Wall St’s Community page, where millions of investors compare notes and perspectives.

What sets Narratives apart is their flexibility. When new information such as earnings reports or news is released, Narratives are updated dynamically so your thesis and fair value stay relevant. For example, some investors see Hudbay’s production growth, strategic partnerships, and copper market exposure as drivers for a high-end price target of CA$22.89, while others factor in operational risks for a more cautious target like CA$16.06. Narratives let you create your own, grounded in the story and numbers that make sense for you.

Do you think there's more to the story for Hudbay Minerals? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com