Is Freeport-McMoRan (FCX) Undervalued? A Fresh Look at Recent Valuation Signals

Freeport-McMoRan (FCX) shares have seen some movement over the past week, with the stock up nearly 10%. However, longer-term returns have trailed the broader market. Investors may be re-evaluating the company's value as commodity prices fluctuate.

See our latest analysis for Freeport-McMoRan.

After a challenging run in recent months, Freeport-McMoRan’s 1-year total shareholder return is down about 21%, though the latest share price bump hints some optimism may be returning as investors react to shifting commodity prices and future demand expectations. While momentum has been subdued for much of the year, the company’s long-term total shareholder returns have still outpaced its short-term share price performance.

If today’s recovery has you thinking about what else could be on the move, consider exploring fast growing stocks with high insider ownership. Discover fast growing stocks with high insider ownership

With shares still trading below analyst price targets and mixed signals from recent results, the key question is whether Freeport-McMoRan is trading at a bargain or if the market has already priced in its future growth prospects.

Most Popular Narrative: 22.3% Undervalued

Freeport-McMoRan’s most widely referenced narrative places its fair value notably above the last close. This significant gap highlights high expectations around the company’s next strategic chapter.

Freeport's new Indonesian smelter, starting up ahead of schedule and expected to reach full capacity by year-end, will make the company a fully integrated global copper producer. This is anticipated to lower operating costs, capture more downstream value, and reduce exposure to export duties. These factors are expected to directly support higher future margins and cash flows.

What’s fueling this ambitious valuation? It is not just new facilities, but an aggressive transformation plan with bold predictions for margin expansion and downstream control. See the assumptions that created this potential value upside in the full narrative.

Result: Fair Value of $50.06 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, reliance on Indonesian operations and uncertainties surrounding future government policies could quickly shift expectations for Freeport-McMoRan’s long-term growth and margins.

Find out about the key risks to this Freeport-McMoRan narrative.

Another View: Market Ratios Tell a Different Story

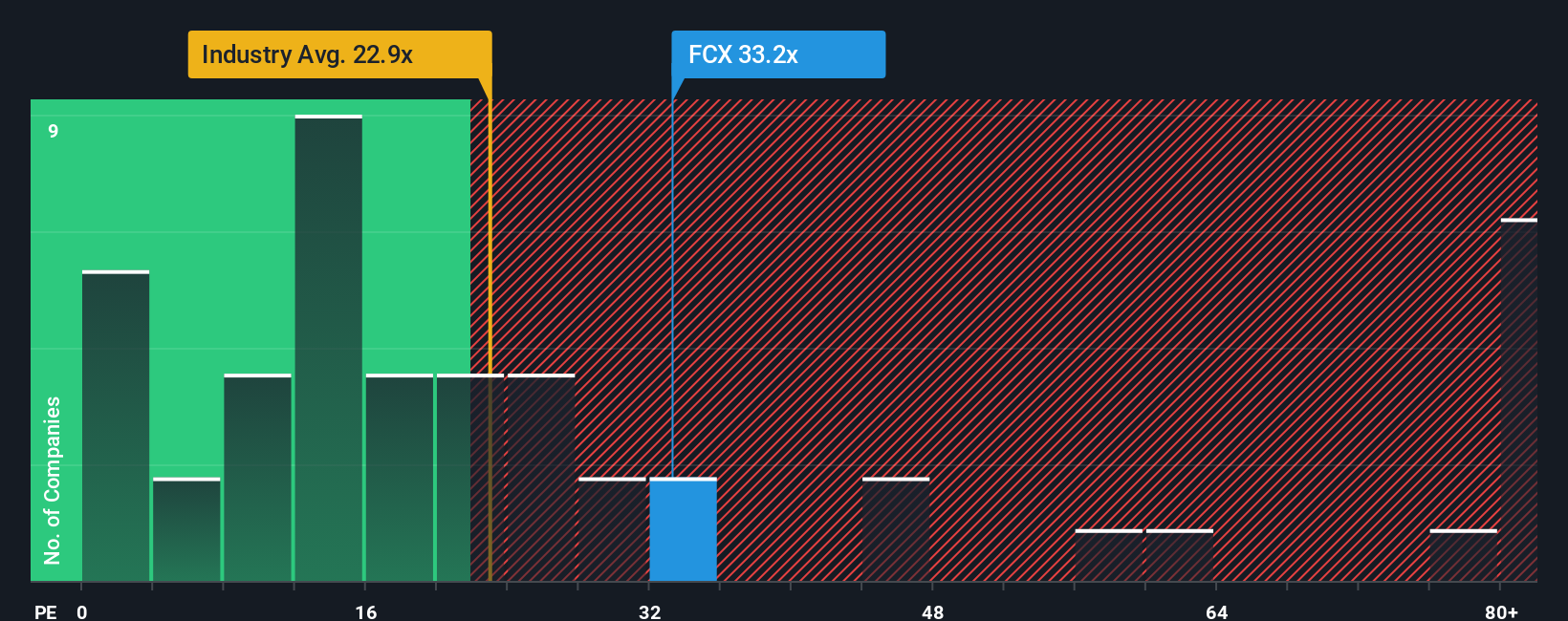

While Freeport-McMoRan appears undervalued by detailed cash flow models, its current price-to-earnings ratio sits at 29.1x. This is noticeably higher than the industry average of 24.7x and the peer group average of 25.4x. Even compared to its fair ratio of 30.3x, there is only a narrow margin for value.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Freeport-McMoRan Narrative

If you see things differently or want to dive into the numbers on your own, crafting your own perspective takes less than three minutes. Do it your way

A great starting point for your Freeport-McMoRan research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Opportunities do not wait around. Give yourself an edge by checking powerful stock lists shaped by rigorous data and fresh market trends on Simply Wall Street.

- Catch high-yield potential and steady passive income by reviewing these 19 dividend stocks with yields > 3% offering yields above 3% right now.

- Tap into tomorrow’s breakthroughs and innovation by searching these 24 AI penny stocks that are transforming the landscape with artificial intelligence.

- Spot companies the market may be overlooking by using these 904 undervalued stocks based on cash flows based strictly on their underlying cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com