GDS Holdings (NasdaqGM:GDS): Assessing Valuation After C-REIT IPO and $1.2bn Equity Raise

GDS Holdings (NasdaqGM:GDS) has caught investor attention after successfully completing its C-REIT IPO on the Shanghai Stock Exchange and raising $1.2 billion in new equity. These developments position the company to expand data center capacity and support growth initiatives.

See our latest analysis for GDS Holdings.

With major fundraising and a successful C-REIT IPO providing momentum for growth, GDS Holdings has drawn investor interest this year. The share price now sits at $41.35, reflecting a cautious but steadily improving mood; over the past year, the total shareholder return stands just under 1%, leaving long-term investors looking for stronger follow-through on recent momentum. While recent events point to larger ambitions ahead, the market’s reaction suggests investors are watching for evidence of sustained growth and profitability before re-rating the stock.

If technology’s next wave of growth has you curious, it might be the perfect moment to broaden your search and discover See the full list for free.

With share price gains and major new funding making headlines, the key question emerges: is GDS Holdings undervalued with room to run, or are markets already factoring in the company’s future growth prospects?

Most Popular Narrative: 12.8% Undervalued

GDS Holdings’ widely followed narrative places its fair value at $47.44, outpacing the recent close of $41.35 and elevating debate about whether growth assumptions can close that gap. Investor focus has sharpened as analysts highlight catalysts ranging from new listings to international expansion.

The successful implementation of China's first data center ABS and C-REIT IPOs has pioneered a pathway for GDS to repeatedly recycle capital at cap rates and multiples well above the company's own market valuation, allowing the company to fund new growth while improving leverage and enhancing ROIC, supporting stronger net earnings over time.

Curious what could deliver this robust upside? There is a game-changing assumption driving the bullish narrative. Bold margin targets and future profit multiples are only part of the equation; the outlook is built on aggressive earnings acceleration few might expect. Dive in to see the numbers that could rewrite GDS’s value story.

Result: Fair Value of $47.44 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure and ongoing declines in service revenue could quickly challenge the bullish outlook if these trends continue or if demand slows.

Find out about the key risks to this GDS Holdings narrative.

Another View: Multiples Tell a Different Story

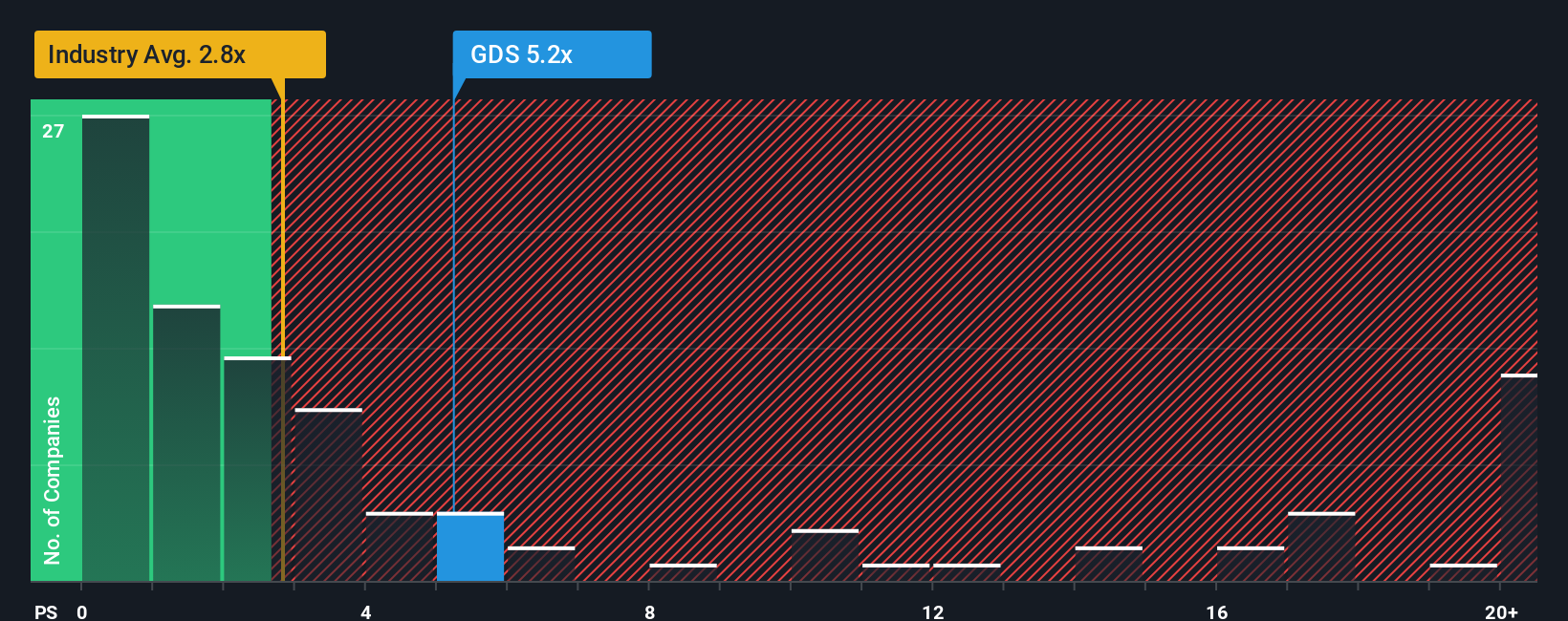

Looking at GDS Holdings through sales-based market multiples, the company’s current ratio stands at 5.4 times sales, notably higher than both the US IT industry average of 2.3x and peer average of 3.6x. The fair ratio, at 3.3x, suggests the stock is priced well above what broader market trends might justify. This premium could signal optimism for sustained growth or raise red flags about valuation risk. Will profits catch up, or is the bar set unreasonably high?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own GDS Holdings Narrative

If you’d rather investigate the numbers firsthand or want an independent take, you have the tools to chart your perspective in just minutes. Do it your way.

A great starting point for your GDS Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Take your strategy further and seize fresh opportunities alongside GDS Holdings. The Simply Wall Street Screener reveals smart investments often overlooked by the crowd. Now is your chance to get ahead and find your edge.

- Unleash growth potential by targeting companies with strong financials using these 3563 penny stocks with strong financials, and spot tomorrow’s winners before the crowd catches on.

- Supercharge your portfolio by tapping into generative AI and automation leaders. See the innovators behind tomorrow’s breakthroughs among these 24 AI penny stocks.

- Secure your future with value opportunities by tracking these 19 dividend stocks with yields > 3% that deliver steady income and robust returns, rain or shine.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com