Assessing Assurant’s Value After Strong 12.8% Share Price Growth in 2025

If you hold shares in Assurant or are considering jumping in, you are not alone in sizing up its recent performance and prospects. The stock has caught some attention after a solid run, closing at $218.36 and delivering a 1.1% gain in the past week alone. That momentum builds on a longer-term winning streak, with the share price up 12.8% over the past year and an impressive 89.7% over five years. While some of these moves trace back to broader insurance sector developments, it is clear market sentiment on Assurant is shifting, possibly reflecting renewed optimism or a rethinking of the company’s risk profile.

If you are trying to figure out what Assurant is really worth, you will want to go deeper than price charts. That is where valuation checks come into play. According to a systematic approach, the company is currently undervalued in 3 out of 6 standard metrics, giving it a valuation score of 3. What does that mean for you, and which valuation models are actually the most reliable? Let’s walk through the main ways investors measure value, and at the end, I will share an approach that can help you go beyond the usual yardsticks.

Approach 1: Assurant Excess Returns Analysis

The Excess Returns model is a valuation approach that focuses on how much profit a company generates above the cost of its capital. Instead of just looking at earnings or dividends, it focuses on return on invested capital and measures whether the company is delivering sustainable, superior value for shareholders over time.

For Assurant, the data is compelling. The current Book Value stands at $108.81 per share, with a Stable Book Value projected at $128.00 per share based on weighted estimates from six analysts. Meanwhile, Stable EPS is estimated at $20.77 per share, reflecting future profitability, also drawn from consensus analyst expectations. The company's Average Return on Equity sits at 16.23%, comfortably above the Cost of Equity of $8.67 per share. That results in an Excess Return of $12.10 per share, highlighting Assurant’s ability to generate consistent value above its basic funding costs.

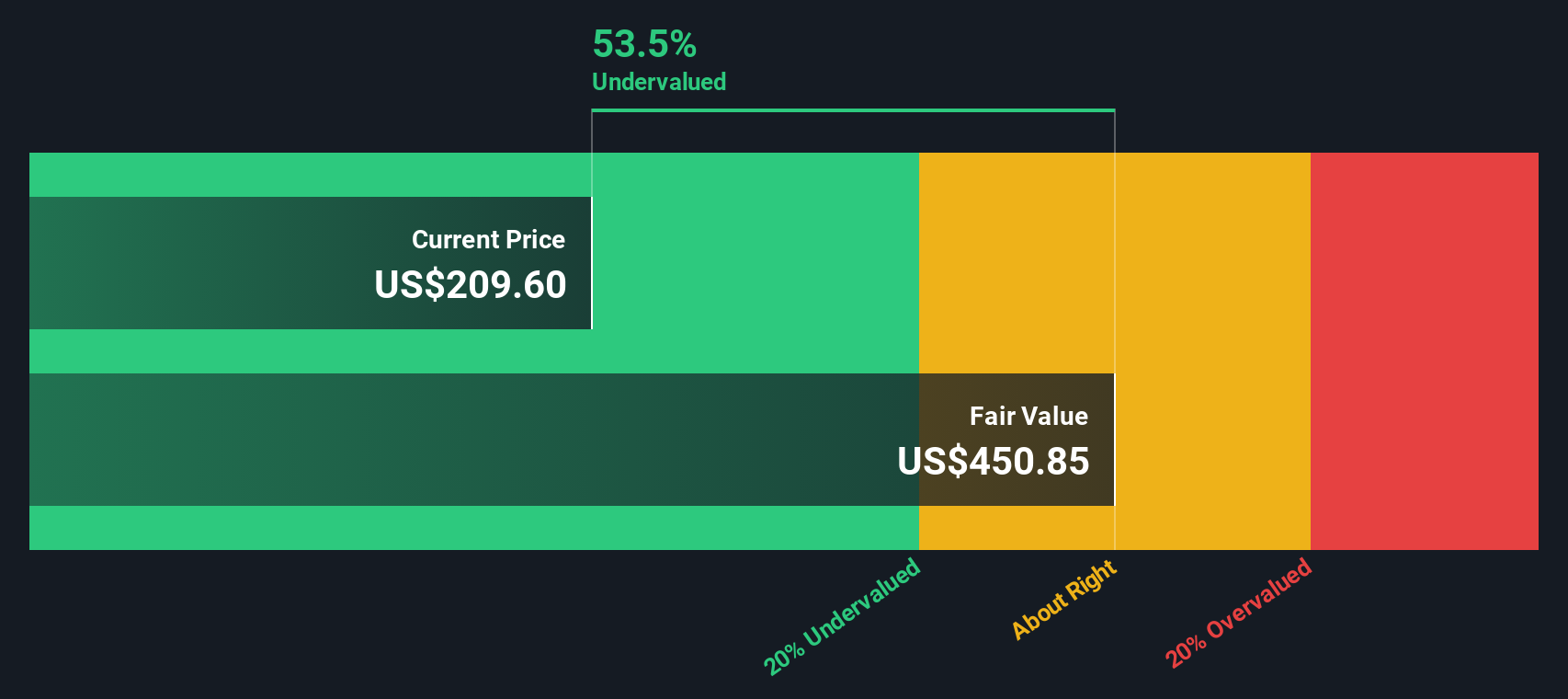

When these metrics are applied within the Excess Returns model, Assurant’s estimated intrinsic value comes out at $455.39 per share. Compared to the current share price of $218.36, this implies the stock is approximately 52.1% undervalued. Such a steep discount suggests investors may be overlooking the company’s ongoing ability to generate robust shareholder returns.

Result: UNDERVALUED

Our Excess Returns analysis suggests Assurant is undervalued by 52.1%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Assurant Price vs Earnings

For established, profitable companies like Assurant, the Price-to-Earnings (PE) ratio is a straightforward and widely used valuation tool. It tells you how much investors are willing to pay for each dollar of earnings, providing a quick snapshot of market expectations for growth and risk. All else being equal, higher growth prospects and lower risk justify a higher PE, while lower growth or greater uncertainty tend to bring the ratio down.

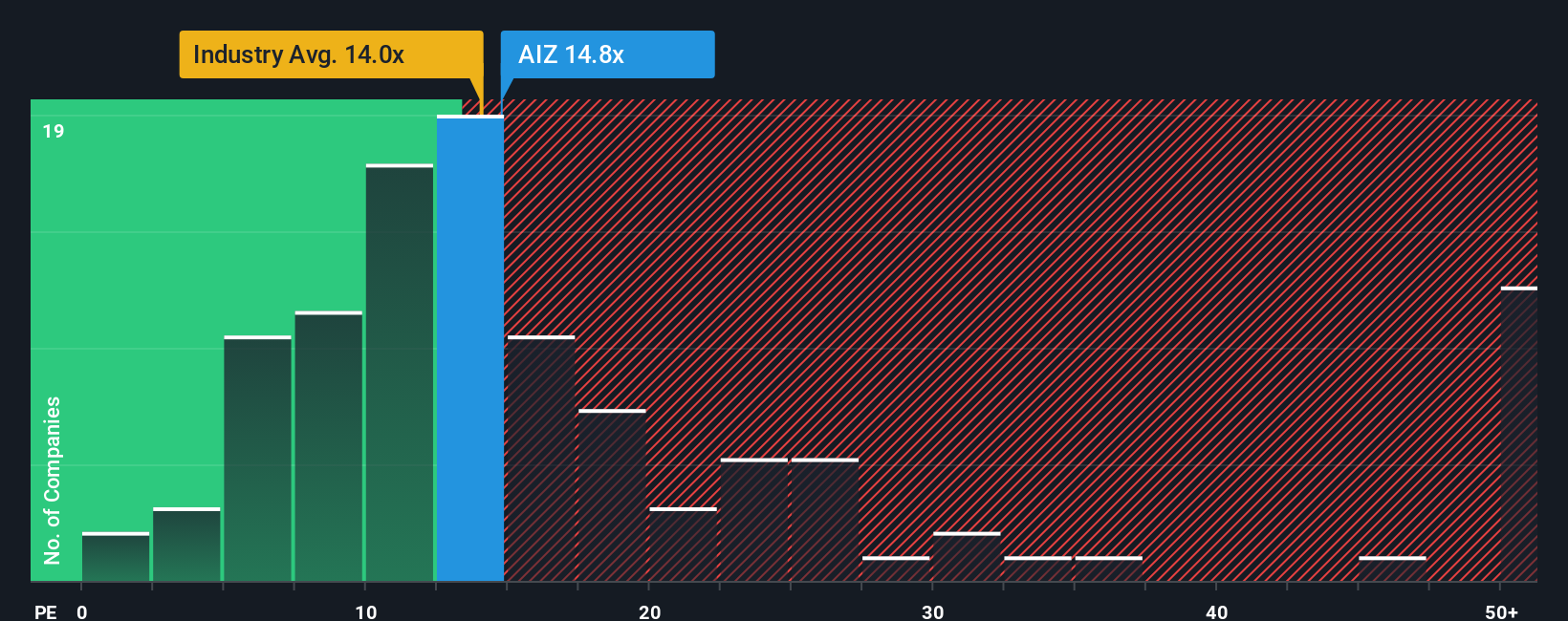

Currently, Assurant trades at a PE ratio of 15.37x. To put this in context, the industry average PE is 13.99x, and the peer group average is 12.62x. This means Assurant’s shares are priced at a slight premium relative to its sector and to similar companies, suggesting that the market recognizes some unique strengths or growth potential within the business.

Simply Wall St's proprietary “Fair Ratio” deepens the analysis by considering more than just earnings. It factors in important elements like expected earnings growth, profit margins, risk profile, market capitalization, and the wider industry landscape to estimate what a suitable PE multiple for Assurant truly is. For Assurant, the Fair Ratio comes out at 16.79x. This tailored benchmark is more informative than a simple industry or peer comparison. It directly reflects the company’s individual circumstances and prospects rather than broad averages.

Comparing these numbers, Assurant’s current PE of 15.37x is below its Fair Ratio of 16.79x. This indicates the stock could be valued at a discount relative to what its business fundamentals would justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Assurant Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your perspective, or story, about a company, grounded in your own assumptions for fair value and estimates of future revenue growth, earnings, and profit margins. By linking the company’s business story and strategic context directly to a financial forecast and a calculated fair value, Narratives help you understand where the numbers come from and why they matter.

Narratives are easy to use and accessible to everyone through the Simply Wall St platform’s Community page, trusted by millions of investors. With a Narrative, you can compare your fair value estimate directly to the current price to decide whether you think the stock is a buy, hold, or sell, and because Narratives update automatically as new news or earnings arrive, your investment thesis stays current. For example, one Assurant Narrative, “AI and Device Protection Will Expand Global Markets,” assumes robust revenue and margin growth and values the company at $241 per share. By contrast, a more cautious Narrative might focus on regulatory and tech risks, pointing to a lower valuation.

Do you think there's more to the story for Assurant? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com