Rolls-Royce (LSE:RR.) Valuation in Focus After Strong One-Year Shareholder Return

Rolls-Royce Holdings (LSE:RR.) has caught investor interest recently, with its stock seeing marked gains over the past month. Shares are up 9% as the company continues to navigate industry shifts and evolving post-pandemic demand patterns.

See our latest analysis for Rolls-Royce Holdings.

Looking at the bigger picture, Rolls-Royce Holdings’ strong 30-day share price return adds to a year of remarkable momentum, with the 1-year total shareholder return sitting comfortably above 120%. Recent headlines have further lifted sentiment, making it clear that momentum is building rather than fading.

If the resurgence in aerospace and defense stocks has your attention, now is the perfect moment to explore See the full list for free.

But with shares near recent highs and analysts’ targets close to current prices, investors are left wondering if Rolls-Royce is truly undervalued, or if the market is already factoring in all that future growth.

Most Popular Narrative: 3% Overvalued

With Rolls-Royce Holdings closing at £11.68, the most widely followed valuation narrative estimates fair value at £11.36, leaving little room for upside as expectations remain high. Current market optimism sets an ambitious benchmark for future growth, and the next key catalyst could determine whether shares have more room to run or have topped out.

The growing investor enthusiasm for Rolls-Royce's sustainable technology initiatives (SMRs, UltraFan, hydrogen propulsion, advanced battery storage) is increasingly priced into the stock. However, these projects remain in early commercialization stages and carry material execution, regulatory, and capex risks. If adoption lags or investor timelines prove optimistic, anticipated new revenue streams are likely to be delayed, impacting long-term earnings visibility.

Want to know the financial assumptions powering this lofty valuation? The story hinges on ambitious revenue expansion, bold earnings forecasts, and a multiple that rivals market leaders. Uncover the full narrative for a look at the surprising bullish case and see which aggressive projections are steering the fair value today.

Result: Fair Value of £11.36 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent supply chain disruptions or a faster than expected slowdown in data center and airline demand could quickly challenge the current bullish outlook.

Find out about the key risks to this Rolls-Royce Holdings narrative.

Another View: Peer Valuation Signals Opportunity

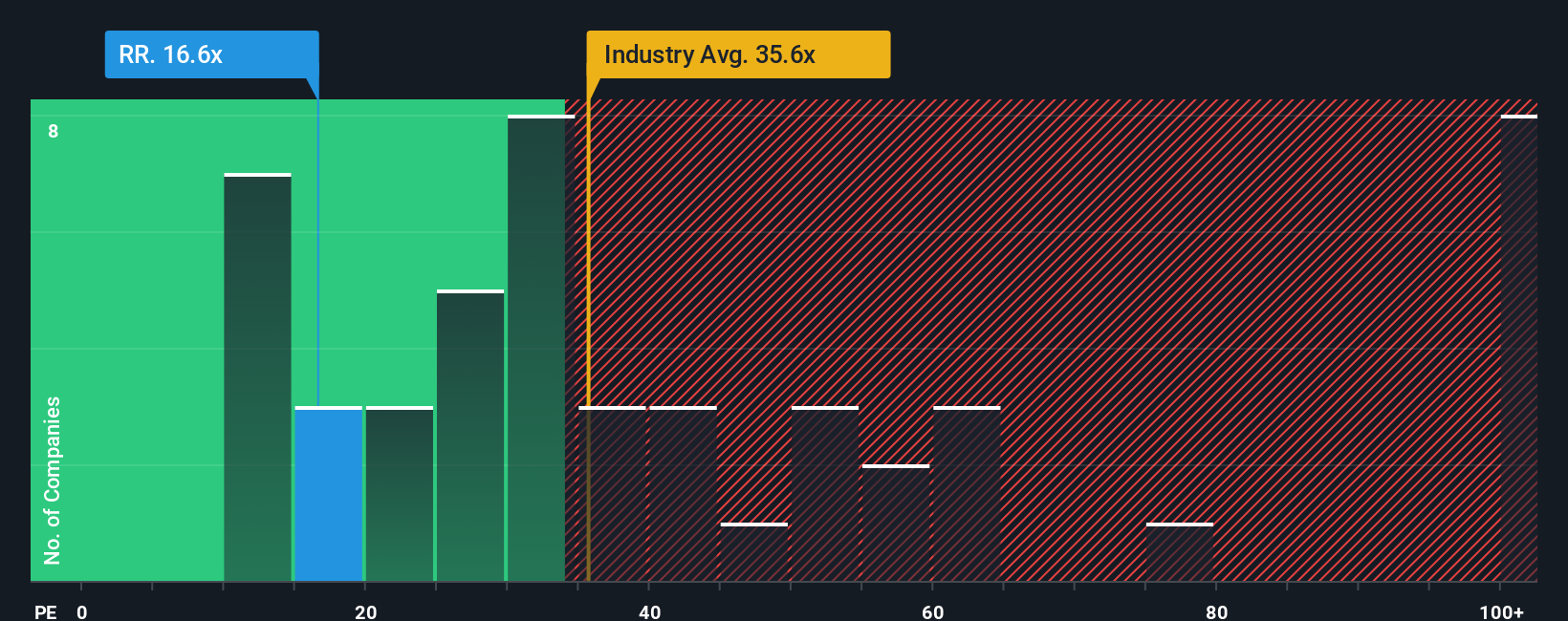

While fair value estimates suggest Rolls-Royce is slightly overvalued, its price-to-earnings ratio stands at 16.9x, which is well below both European industry peers at 34x and the average for similar companies at 28.5x. It is also beneath the fair ratio of 19.6x. This discount narrows valuation risk, but is the market overlooking something, or does it signal a mispriced opportunity?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Rolls-Royce Holdings Narrative

If you have a different perspective or want to dig deeper, you can easily assemble your own Rolls-Royce valuation story from the same data in just a few minutes. Do it your way

A great starting point for your Rolls-Royce Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Why settle for the ordinary when you can spot tomorrow’s winners today? If you want an edge, let these curated stock ideas work for you:

- Catch profit potential by following these 909 undervalued stocks based on cash flows, featuring companies trading below their fair value. This may give your portfolio more room to grow.

- Tap into the future of medicine by targeting breakthroughs through these 31 healthcare AI stocks, where innovation combines with strong financials to support smarter investing.

- Power your search for reliable income by securing these 19 dividend stocks with yields > 3%, which highlights high-yield picks designed for steady income opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com