CAVA Group (CAVA): Evaluating Valuation After Recent Share Price Bounce

See our latest analysis for CAVA Group.

While CAVA Group’s 1-year total shareholder return remains in negative territory, this week’s modest share price pick-up hints at stabilizing sentiment after months of declines. Momentum is not yet convincing, but some investors see early signs of a turnaround.

If you’re keen to see what other exciting companies are catching investors’ attention, it is a perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With shares now trading well below recent highs and analysts setting targets significantly above the current price, the key question for investors is whether CAVA is trading at a discount or if the market already reflects its growth prospects.

Most Popular Narrative: 31.4% Undervalued

Based on the most widely followed narrative, CAVA Group’s fair value is set at $92.21, well above the current close of $63.24. This narrative suggests the market may be missing something crucial about the stock’s future prospects.

Rapid geographic expansion into new and underserved markets, supported by strong new unit performance and a robust target of at least 1,000 restaurants by 2032, is likely to accelerate systemwide sales and drive higher topline revenue growth.

Want to know the growth blueprint behind this high valuation? The key element of this narrative is bold expansion goals and a future earnings multiple befitting a fast-growth disruptor. Which future financial milestones set the stage for this aggressive price target? Uncover the details that make this fair value so provocative.

Result: Fair Value of $92.21 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slower sales growth or overstretched expansion plans could limit the brand's momentum and challenge analyst assumptions that support the higher valuation.

Find out about the key risks to this CAVA Group narrative.

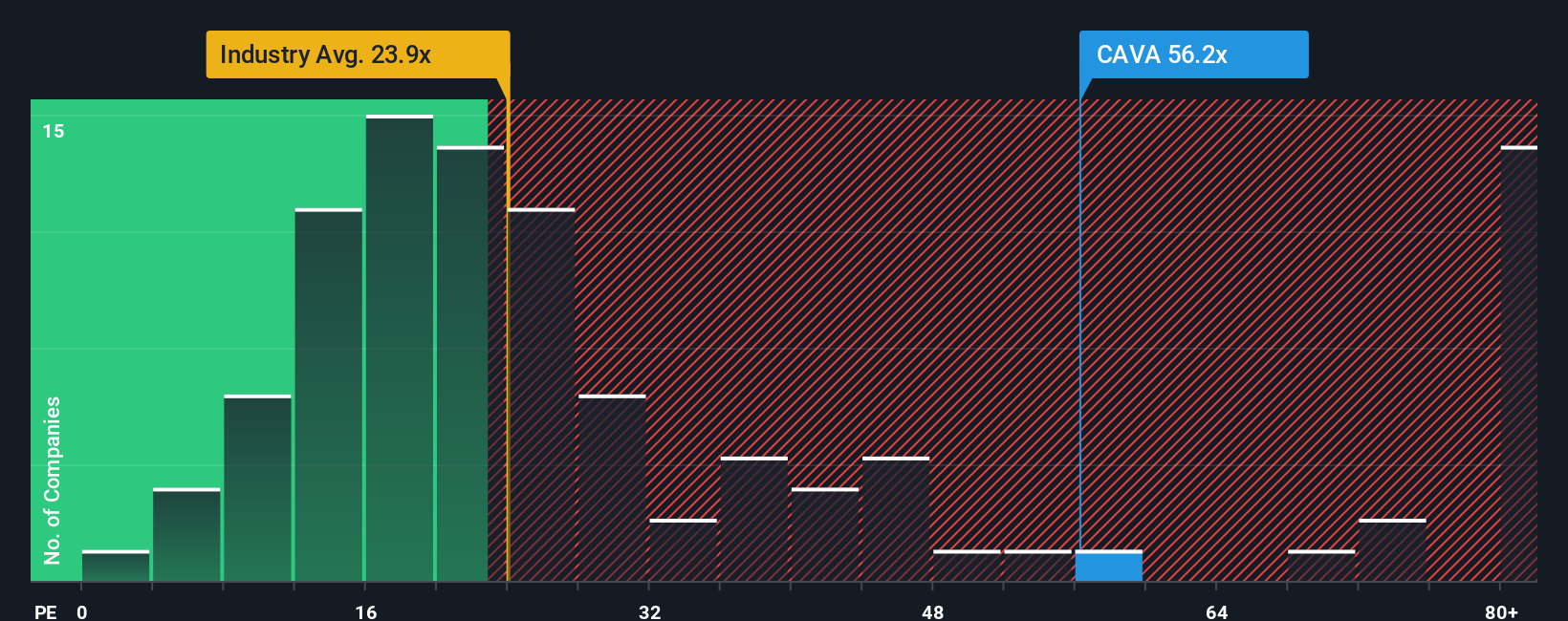

Another View: Multiples Suggest Overvaluation

While the analyst consensus points to CAVA Group being undervalued, our multiples comparison paints a different picture. CAVA’s current price-to-earnings ratio of 52.1x stands well above the US Hospitality industry average of 24.4x, the peer group’s 49.8x, and even the fair ratio of 21.6x. This significant gap highlights valuation risk. Is the market expecting too much growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CAVA Group Narrative

If you want to dig into the numbers and draw your own conclusions, you can craft a fresh take on CAVA Group’s story in just minutes. Do it your way

A great starting point for your CAVA Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

You could miss out on the next big opportunity. Fuel your research and take control by exploring curated investment screens on Simply Wall Street today.

- Maximize your returns with steady income by tapping into these 19 dividend stocks with yields > 3%, which delivers yields over 3% from companies with strong fundamentals.

- Ride the wave of technological disruption and access growth potential in artificial intelligence with these 24 AI penny stocks.

- Get ahead of the curve by searching for hidden value gems in these 909 undervalued stocks based on cash flows based on robust cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com