Is ASML (ENXTAM:ASML) Undervalued or Overpriced? A Deep Dive Into Its Latest Valuation Narratives

See our latest analysis for ASML Holding.

ASML Holding’s recent price action suggests investors are warming up to its long-term prospects, with momentum coming off a strong year highlighted by a 17% one-year total shareholder return. The steady uptick in revenue and earnings, along with robust demand for its semiconductor equipment, continues to underpin positive sentiment around its share price.

If you’re curious to see what other innovative tech leaders are making waves this year, check out the full list of opportunities with our See the full list for free..

Yet with shares now trading well above their previous averages and analyst targets, the critical question remains: does ASML still offer genuine value at today’s price, or has the market already factored in its future growth potential?

Most Popular Narrative: 12.2% Undervalued

ASML Holding’s most closely tracked narrative currently sees the stock trading at a 12% discount to its fair value. This suggests that recent market caution might be overlooking key strengths. With the narrative’s fair value set at €1,000 per share, a last close at €877.60 places the stock well below this benchmark and invites a closer look at the core assumptions behind this view.

With its technological moat, strong balance sheet, and central role in enabling next-gen chips, ASML remains one of the most critical players in the semiconductor value chain. The current weakness may be a rare opportunity to accumulate shares of a company that is essential to the future of computing.

Want to know what is fueling this optimistic calculation? There is a sharp focus on margin strength, robust recurring revenue, and ambitious long-term growth. The math behind this target rests on bold forecasts for the industry’s next leap and a clear bet on ASML’s dominance. Don’t miss the deep dive on the projections that power this premium.

Result: Fair Value of €1,000 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, potential catalysts such as tighter export controls or a prolonged slowdown in semiconductor demand could quickly challenge this undervalued thesis.

Find out about the key risks to this ASML Holding narrative.

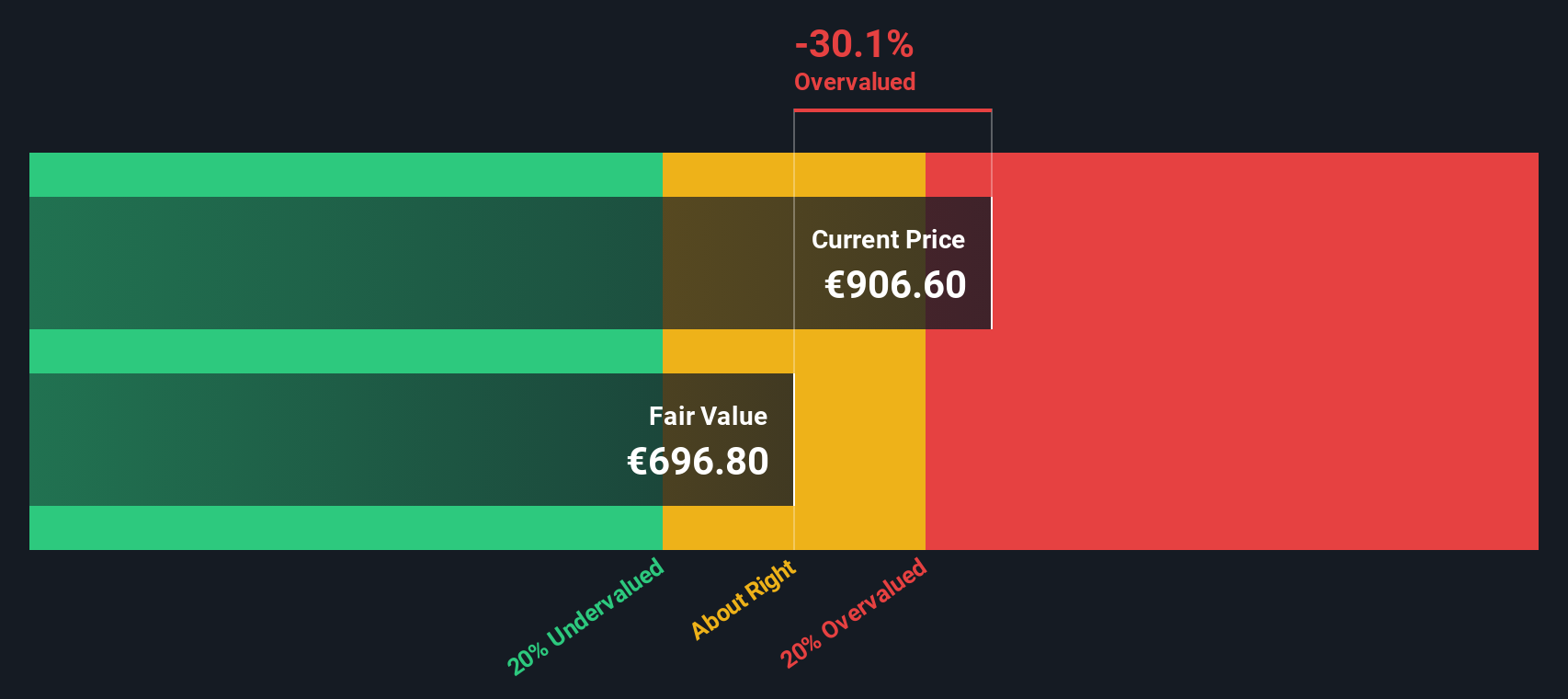

Another View: Discounted Cash Flow Model Signals Overvaluation

While the current narrative points to ASML trading at a healthy discount to fair value, our SWS DCF model presents a different perspective. The DCF approach estimates ASML’s intrinsic worth at €660.74 per share, which is significantly below the market price. This suggests the market may be assigning more value to future growth than historic cash flows justify. Which story will play out?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASML Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ASML Holding Narrative

If you have your own perspective or want to dive deeper into the numbers yourself, you can easily craft a personalized outlook on ASML in just minutes. Do it your way

A great starting point for your ASML Holding research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let your research stop here. Smart investors always have fresh opportunities on their radar. Use these hand-picked ideas to uncover your next potential winner.

- Uncover companies with strong dividends and long-term income potential by checking out these 19 dividend stocks with yields > 3%.

- Jump into the frontier of technology by reviewing these 24 AI penny stocks that are redefining artificial intelligence and automation across industries.

- Capture hidden value by targeting these 910 undervalued stocks based on cash flows and spot stocks that the market might be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com